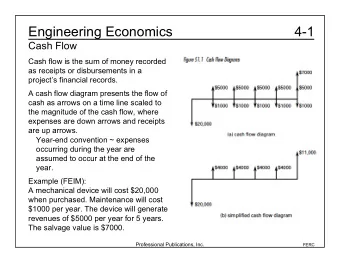

10/18/19 1 Cash Flow, Inventory, and Your Financial Health Ollin Sykes, CPA, CTIP, CMA Scott Sykes, CPA Sykes & Company, P.A. 2 1

10/18/19 Disclosures There are no relevant financial relationships with ACCME- defined commercial interests for anyone who was in control of the content of the activity. 3 Pharmacist and Pharmacy Technician Learning Objectives • List nine best practices for managing community pharmacy operations • Discuss strategies for managing inventory effectively • Describe key financial indicators and benchmarks for your own business 4 2

10/18/19 Current Industry Trends • Tighter reimbursements • Lower margins in some cases • Increased DIR/GER/BER fees • Tighter cash flow • USP <800> • Track and Trace • Third-Party reconciliation • Inventory management 5 #1 – Fundamentals: Introduction • Foundation of all businesses • Pharmacy industry inherently requires strong fundamentals • Poor foundation limits analysis and understanding • Lack of controls make fraud easier to perpetrate 6 3

10/18/19 #1 – Fundamentals: Introduction (continued) • Does not allow for proactive management • Poor fundamentals cost owner time and money • Utilize technology • Back office should be streamlined and efficient • Allows for pharmacy owner to focus on growth and patient care 7 #1 – Fundamentals: Daily Processes • Fundamentals include: • Daily/Weekly processes • Point of Sale • Reconciliations • Payroll • Accounts Payable 8 4

10/18/19 #1 – Fundamentals: Balance Sheet • Balance Sheet is a snapshot in time • Assets = Liabilities + Equity • Assets: • Cash, 3 rd Party Receivables, Inventory, Fixed Assets, etc. • Liabilities: • Accounts Payable, Notes Payable, Sales Tax Payable, etc. • Equity: • Retained Earnings, Distributions/Draws 9 #1 – Fundamentals: Profit & Loss • Displays profit or loss for a period Revenues - Cost of Goods Sold Gross Margin - Expenses Net Income 10 5

10/18/19 #2 – Know Your 3 rd Party Receivables • Adjudicate a script - money is owed to the pharmacy from PBM payors • Money owed to the pharmacy is an asset • This asset increases your revenues and provides an accurate picture of gross revenues 11 #2 – Know Your 3 rd Party Receivables • The biggest unreconciled bank account in a pharmacy • Fill and hope is not a fundamental business strategy • Utilize technology and manage • Quickly identify errors and issues with payors • It’s your money! 12 6

10/18/19 #2 – Know Your 3 rd Party Receivables • Provides additional data you can analyze to maximize your cash flow and margin • DIR/GER/BER fee reporting • Average AR days outstanding – 19 – 22 days • Do you know what is owed to you at any given moment? • Do you know if you are getting reimbursed for what you adjudicate? 13 #2 – Know Your 3 rd Party Receivables • Necessary to understand the financial picture of your pharmacy • Allows pharmacy owner to understand payer trends • Catches errors with reimbursements • Captures DIR fees and other adjudication costs 14 7

10/18/19 #2 – Know Your 3 rd Party Receivables • Best Practices for Reconciliation o Manual reconciliation is time consuming and increases payroll costs o Manual reconciliation is not necessary and inefficient o Utilize technology resources in the marketplace 15 #2 – Know Your 3 rd Party Receivables • Best Practices for Reconciliation – continued o Technology captures the information in real time o Does require uploads of 835 files or EOB’s for some payers o Management of the system is required to ensure integrity 16 8

10/18/19 #2 – Know Your 3 rd Party Receivables Aged Receivables Snapshot – Healthy (Page 1) 17 #2 – Know Your 3 rd Party Receivables Aged Receivables Snapshot – Healthy (Page 2) 18 9

10/18/19 #2 – Know Your 3 rd Party Receivables Aged Receivables Snapshot – Unhealthy (Page 1) 19 #2 – Know Your 3 rd Party Receivables Aged Receivables Snapshot – Unhealthy (Page 2) 20 10

10/18/19 #2 – Know Your 3 rd Party Receivables Adjustment Payment Level Detail Report 21 #2 – Know Your 3 rd Party Receivables Aetna DIR Report (Page 1) 22 11

10/18/19 #2 – Know Your 3 rd Party Receivables Aetna DIR Report (Page 2) 23 #2 – Know Your 3 rd Party Receivables Daily Dash 24 12

10/18/19 #3 – Inventory Management • Vital component of financial statements • Guessing is not a business strategy • $100 bills on the shelf • Inaccuracies will impact your financial statements, analysis and advisory • Poor management will crush cash flow 25 #3 – Inventory Management • Poor management may increase tax liabilities • Synchronization! • High performing pharmacies take inventory seriously • Technology continues to improve • Emphasis on inventory management is, and will continue to be, a trend in the coming years 26 13

10/18/19 #3 – Inventory Management • Inventory Turn = Cost of Goods Sold / Average Inventory • Demand shifts daily/constantly • Next day ordering, let wholesaler carry cost/risk • Inventory management is a process • Explore automation 27 #3 – Inventory Management – Track & Trace • Drug Supply Chain Security Act • Enacted to further secure drug supply • Trace drug unit through supply chain • Must confirm the entities you do business with are licensed and registered • Must implement protocols and processes for identifying suspect and illegitimate products 28 14

10/18/19 #3 – Inventory Management – Track & Trace • Receive, store, and provide product tracing documentation including transaction information, history and statement • Intercompany transfers or transfers with other pharmacies must be considered • Begin inquiring trading partners on how these compliance issues will impact their pharmacy • Ultimate impact on pharmacies and inventory management 29 #3 – Inventory Management – Physical Counts • Annual physical counts in the 3rd or early 4th quarter • Two physical counts if more data points are needed • Use to adjust books and records to actual • Utilize for proactive tax planning • Companies in the market that specialize in pharmacy inventory 30 15

10/18/19 #3 – Inventory Management – Perpetual • Pharmacies today must utilize, change required • Nearly impossible to maximize net profit without • Scheduled periodic cycle counts • Technology to analyze your Rx data • Carefully craft reorder points to maximize cash flow 31 #3 – Inventory Management – Perpetual • Package size analysis and economies of scale • Synchronization!! • Scheduled returns • Monthly accounting adjustments, real-time margin, and enhanced financial advisory • Accurate cost downloads are necessary (EDI) 32 16

10/18/19 #4 – Cost of Goods Sold/Margin • Biggest expense in a pharmacy • Accurate inventory adjustments are vital • Any inaccuracies will impact margin and net income • Average retail 2019 gross margin approximately 23% 33 #4 – Cost of Goods Sold/Margin • Revenue diversification and specialization to enhance margin • DIR fee impacts to gross margin and profit and loss statement • Are you maximizing behind the bench adjudication 34 17

10/18/19 #5 – Payroll • Payroll inherently complex • Look to technology and outsourcing • Second biggest expense for a pharmacy • Average is 10.5% of total revenue • Under 10% of total revenues ideal 35 #5 – Payroll • Simple analysis of your operating hours may provide opportunity to cut costs dramatically • Should owners adjust their salaries for tax purposes? • How do owner salaries impact retirement planning? 36 18

10/18/19 #6 – DIR/GER/BER/ER Fees • DIR fees continue to trend higher • Know what your fees are as a % of revenue • Know your star ratings • Average 1.8% - 4%+ • Understand your accounting • Utilize technology to capture 37 #7 – Key Performance Indicators • Current Ratio • Current Ratio = Current Assets / Current Liabilities 2.5 / 1 – Average • • < 2.0 / 1 – Red Flag • > 2.5 / 1 – Good, higher the better 38 19

10/18/19 #7 – Key Performance Indicators • Equity to Assets • Equity Ratio = Total Equity / Total Assets • 10-20% for newer pharmacies • 50% + for mature pharmacies • Great indicator of balance sheet strength 39 #7 – Key Performance Indicators • Inventory Turnover • Inv. Turnover = COGS / Avg. Inventory • Typical industry average is 12 turns a year • Higher the better. Explains how well you manage inventory 40 20

10/18/19 #7 – Key Performance Indicators • Others • Gross Margin – 23% • AR Days – 19 • Payroll % of Rev. – 10.5% • Overhead % – 6-8% • Net Income – 4-7% 41 #8 – Accrual and Cash Accounting • Generally, pharmacies were required to report on the accrual basis of accounting for tax purposes • TCJA expanded the use of the cash method of accounting for tax reporting • Many pharmacies incorrectly reported cash basis for tax and therefore not eligible to take advantage 42 21

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries