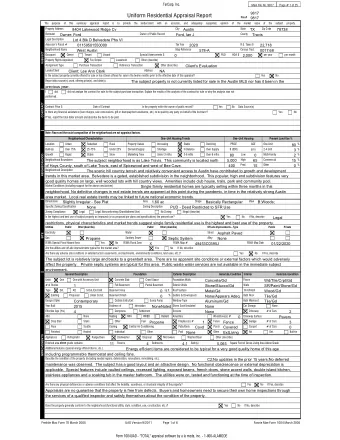

BMO Capital Markets Global Metals and Mining Conference CASH POSITIVE DESPITE THE LOWER GOLD PRICE Nick Holland 29 February 2016

Forward looking statements Certain statements in this document constitute “ forward looking statements ” within the meaning of Section 27A of the US Securities Act of 1933 and Section 21E of the US Securities Exchange Act of 1934. In particular, the forward looking statements in this document include among others those relating to the Damang Exploration Target Statement; the Far Southeast Exploration Target Statement; commodity prices; demand for gold and other metals and minerals; interest rate expectations; exploration and production costs; levels of expected production; Gold Fields ’ growth pipeline; levels and expected benefits of current and planned capital expenditures; future reserve, resource and other mineralisation levels; and the extent of cost efficiencies and savings to be achieved. Such forward looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of the company to be materially different from the future results, performance or achievements expressed or implied by such forward looking statements. Such risks, uncertainties and other important factors include among others: economic, business and political conditions in South Africa, Ghana, Australia, Peru and elsewhere; the ability to achieve anticipated efficiencies and other cost savings in connection with past and future acquisitions, exploration and development activities; decreases in the market price of gold and/or copper; hazards associated with underground and surface gold mining; labour disruptions; availability terms and deployment of capital or credit; changes in government regulations, particularly taxation and environmental regulations; and new legislation affecting mining and mineral rights; changes in exchange rates; currency devaluations; the availability and cost of raw and finished materials; the cost of energy and water; inflation and other macro-economic factors, industrial action, temporary stoppages of mines for safety and unplanned maintenance reasons; and the impact of the AIDS and other occupational health risks experienced by Gold Fields ’ employees. These forward looking statements speak only as of the date of this document. Gold Fields undertakes no obligation to update publicly or release any revisions to these forward looking statements to reflect events or circumstances after the date of this document or to reflect the occurrence of unanticipated events. BMO Global Metals and Mining Conference, Nick Holland, 29 February 2016 2

Q4 and FY 2015 Results Salient features Net cash flow from operating activities of US$47m (FY15: US$123m) Attributable gold equivalent production up 2% QoQ to 566koz (FY15: 2,159koz) All-in costs down 2% QoQ to US$942/oz (FY15: US$1,026/oz) Normalised earnings of US$15m (FY15: US$45m) Final dividend of 21 SA cents declared (FY15: 25 SA cents) Net debt decreased US$47m QoQ to US$1,380m, net debt to EBITDA at 1.38x South Deep – production up 24% QoQ to 68koz (FY15: 198koz) Impairments of US$300m – none of the significant operating assets affected FY16 guidance – production of 2.05-2.10Moz at AIC of US$1,035-1,045/oz Cash positive despite the lower gold price BMO Capital Markets Global Metals and Mining Conference, Nick Holland, 29 February 2016 3

Steady decrease in all-in costs Q4 2015: production up 2%, all-in costs down 2%, gold price flat 2013 2014 2015 700,000 1800 Production: 2,022koz Production: 2,219koz Production: 2,159koz AIC: US$1,312/oz AIC: US$1,087/oz AIC: US$1,026/oz 598,000 1600 600,000 566,000 559,000 557,000 556,000 557,000 548,000 535,000 1400 496,000 501,000 500,000 477000 451,000 1200 400,000 1000 Ounces US$/oz 800 300,000 600 200,000 400 100,000 200 0 0 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Attr Gold Produced Gold Price AIC Steady decrease in AIC through 2015 BMO Global Metals and Mining Conference, Nick Holland, 29 February 2016 4

Strong focus on cash generation Net cash flow 2013 2014 2015 250 2,000 Gold: US$1,249/oz Gold: US$1,140/oz Gold: US$1,386/oz Net cash: US$236m Net cash: US$123m Net cash: (US$232m) 1,625 1,500 1,372 1,315 1,283 1,275 1,265 150 1,265 1,198 1,179 1,174 1,103 1,092 1,000 75 65 63 54 54 47 38 50 30 500 4 US$ million US$/oz -29 -50 0 -45 -500 -150 -1,000 -229 -250 -1,500 -350 -2,000 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Net cash flow Gold price Net cash flow from operating activities after taking account of net capital expenditure, environmental payments, debt service costs and non-recurring items. US$123m net cash flow from operating activities generated in FY15 BMO Global Metals and Mining Conference, Nick Holland, 29 February 2016 5

Comfortable balance sheet, with flexibility Balance sheet ● Net debt of US$1,380m at 31 December 2015 Net debt (US$m) and Net debt/EBITDA 2,000 1.8 ● Net debt to EBITDA of 1.38x at end-Q4 2015 1.6 1,500 ● Unutilised facilities of US$844m and R2.5bn 1.4 US$m 1,000 1.2 ● First debt maturity in November 2017 500 1.0 0 0.8 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2013 2014 2014 2014 2014 2015 2015 2015 2015 Net debt Net debt/EBITDA Debt facilities Net debt/EBITDA and gold price 3,500 1.8 1,300 1.6 1,250 3,000 1.4 1,200 2,500 1.2 1,150 1.0 US$m 2,000 US$/oz 0.8 1,100 1,500 0.6 1,050 0.4 1,000 1,000 0.2 500 0.0 950 0 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 US$ facilities Rand facilities Total facilities 2013 2014 2014 2014 2014 2015 2015 2015 2015 Utilised Unutilised Net debt/EBITDA Gold price Continue to lower net debt BMO Global Metals and Mining Conference, Nick Holland, 29 February 2016 6

South Deep Business performance Q4 Q3 Production (koz) and AIC (US$/oz) 2015 2014 2015 2015 80 2,500 68 70 Production 68.1 54.9 198.0 200.5 koz 2,000 55 60 AISC 1,095 1,404 1,490 1,548 49 US$/oz 50 1,500 39 36 40 AIC 1,156 1,431 1,559 1,732 US$/oz 1,000 30 20 Required leadership in place • 500 10 • Bedding down a performance driven culture 0 0 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Skills development strategy developed • Production AIC • Significant improvement in safety performance Positive production trends emerging • Net Cash Flow (R million) and Gold Price (R/kg) 0 600,000 • Simplified destress mining being implemented -50 500,000 Targeting cash breakeven by end-2016 • -100 -57 -150 400,000 2016 Guidance -200 300,000 • Production: 257koz -250 -266 -300 200,000 • AISC: R550,000/kg -350 -330 100,000 • -361 AIC: R575,000/kg -400 -398 • -450 0 Capex: R999m Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 • Exchange rate: R14.14 = US$1.00 Net cash flow Gold Price Target is to reach breakeven by end-2016 BMO Global Metals and Mining Conference, Nick Holland, 29 February 2016 7

̵ ̵ ̵ ̵ ̵ ̵ ̵ ̵ ̵ ̵ South Deep Key factors underpinning performance improvements ● 98% of critical skills appointed Key Pillars 1. People ● Business improvement implementation 2. Safety and health capacity established 3. Mechanised Fleet 4. Infrastructure ● Fleet renewal 5. Mining ● Infrastructure upgrade and maintenance 6. Mine design and planning ● Improvement in underground working 7. Systems conditions ● Employee motivation through improved TRACKLESS FLEET BUSINESS IMPROVEMENT BUSINESS IMPROVEMENT TRACKLESS FLEET working conditions, safety performance, ● Fleet Renewal ● BI Team reward programs and engagement 24 new units commissioned Program Manager 3 old units decommissioned Project managers Fleet size increased from 74 Execution teams to 95 ● 68 Projects ● Planned Maintenance Project management 93L Workshop framework commissioned Progress monitoring and OEM Maintenance contracts commenced in Q4 reporting in early stages Operating platform improving BMO Global Metals and Mining Conference, Nick Holland, 29 February 2016 8

South Deep Positive trends Destress Face Availability Long Hole Stoping Production & Contribution 90 160 80 140 Number of Ends 70 120 60 Tonnes (‘000)/Q 100 50 80 40 60 30 40 20 24% 36% 37% 34% 40% 22% 20 10 0 0 Q1 2015 Q2 2015 Q3 2015 Q4 2015 2014 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2015 2014 2015 Backfill Production (kt) Development Current Mine 80 1600 New Mine 70 1400 Tonnes (‘000)/Q 60 1200 50 1000 m/Q 40 800 30 600 20 400 10 200 0 0 Q1 2015 Q2 2015 Q3 2015 Q4 2015 2014 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2015 2014 2015 Underground operations gaining momentum BMO Global Metals and Mining Conference, Nick Holland, 29 February 2016 9

South Deep People / Skills / Organisational culture Employee Satisfaction Barometer (Q4 2015) 12% 6% Strongly Satisfied Experienced leadership team in place 30% Satisfied 143 of 146 core positions filled Quality Strongly Dissatisfied Business Improvement team established Dissatisfied 52% 47 x Artisans in training Skills OEM Maintenance contracts (Q4 2015) (26% of mining contribution) Disciplined culture Performance oriented Culture Personal engagement Empowering the team BMO Global Metals and Mining Conference, Nick Holland, 29 February 2016 10

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries