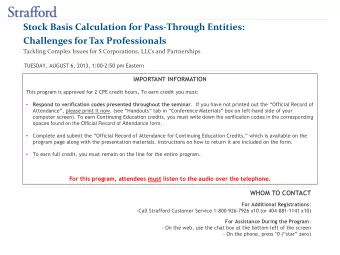

Basis Calculations for Pass-Through Entities: Challenges for Tax Preparers Tackling Complex Calculation Issues for S Corporations, Partnerships and LLCs TUESDAY, JANUARY 8, 2013, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 registered tax return preparer (RTRP) credit hours (other federal tax law/federal tax related ). Based on the IRS rules, to earn credit you must: Participate in the program on your own computer connection or phone line (no sharing) – if you need to register additional • people, please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford accepts American Express, Visa, MasterCard, Discover . • Respond to verification codes presented throughout the seminar . If you have not printed out the “Official Record of Attendance”, please print it now . (see “Handouts” tab in “Conference Materials” box on left -hand side of your computer screen). To earn Continuing Education credits, you must write down the verification codes in the corresponding spaces found on the Official Record of Attendance form . • Complete and submit the “Official Record of Attendance for Continuing Education Credits” included with the presentation materials. That record must include your PTIN ID # . Instructions on how to return it are included on the form. • To earn full credit, you must remain on the line for the entire program. WHOM TO CONTACT For Additional Registrations : -Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10) For Assistance During the Program : - On the web, use the chat box at the bottom left of the screen - On the phone, press *0 (“star” zero) If you get disconnected during the program, you can simply call or log in using your original instructions and PIN.

Sound Quality For best sound quality, we recommend you listen via the telephone by dialing 1-866- 873 - 1442 and entering your PIN when prompted, and viewing the presentation slides online. However, attendees also can opt to listen online if you choose. If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail sound@straffordpub.com so we can address the problem. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

If you have not printed or downloaded the conference materials for this program, please complete the following steps: • Click on the + sign next to “Conference Materials” in the middle of the left -hand column on your screen. • Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides and the Official Record of Attendance for today's program. • Double-click on the PDF and a separate page will open. Print the slides by clicking on the printer icon . •

Stock Basis Calculations for Pass-Through Entities Frank Gariepy, CPA, Partner Meredith Menden, CPA, MBT, Senior Manager www.eidebailly.com www.eidebailly.com 4

IRS CIRCULAR 230 NOTICE Any tax advice expressed in this communication is not intended to be used, and cannot be used, for the purpose of avoiding penalties imposed on the taxpayer by any governmental taxing authority or agency. In addition, if any such tax advice is made available to any person or party other than the party to whom the advice was originally directed, then such advice, under IRS Circular 230, is to be considered as being delivered to support the promotion or marketing (by a person other than Eide Bailly LLP) of the transaction or matter discussed or referenced. Thus, each taxpayer should seek specific tax advice based on the taxpayer’s particular circumstances from an independent tax advisor. www.eidebailly.com www.eidebailly.com 5

S Corporations www.eidebailly.com www.eidebailly.com 6

Background • S Corporation basis is “simple” • Increases • Amounts earned • Amounts contributed • Decreases • Amounts deducted • Amounts distributed • Cannot go negative www.eidebailly.com www.eidebailly.com 7

From the beginning… • Initial Stock Basis • Cash paid for shares • Net Value of Property Contributed to the Corporation (FMV or NTV depending on transaction) • Taxable value of shares received for services provided • Carried over from shares received as gift • Stepped-up for shares inherited • Any combination of the above www.eidebailly.com www.eidebailly.com 8

Increases to Stock Basis • Capital Contributions (property or cash) • Ordinary Income • Investment Income • Gains • Excess of deductions for depletion www.eidebailly.com www.eidebailly.com 9

Decreases to Stock Basis • Distributions (property or cash) • Business Deductions • Non-deductible Expenses • Contributions • 179 Deduction • Losses www.eidebailly.com www.eidebailly.com 10

Who Cares? • Why and when does basis matter • the company had losses • the company made distributions • there was an ownership change in the company. • Basis is a piggy bank • Excess distributions are taxable www.eidebailly.com www.eidebailly.com 11

Order of Basis Adjustments IRC Sec. 1367(a) • Order is very important • First : stock basis is increased for income items • Second : it is decreased for distributions • Third : it is decreased for nondeductible, noncapital expenses • Fourth : it is decreased for items of loss and deduction • Note: If Basis is Positive Before Distributions but would be zeroed out by deduction items, the excess loss is suspended rather than the excess distributions taxable • Election to Reduce Basis by Loss or Deduction Items before Nondeductible Expenses [Reg. 1.1367- 1(g)] www.eidebailly.com www.eidebailly.com 12

Example – [Reg. 1.1367-1(g)] • Sophia owns all of the shares of Princess, Inc., an S corporation that incorporated and elected S status on January 1, 2012. The corporation uses a September 30 year-end. Sophia's stock basis on January 1 is $500,000 • The corporation passes through a non- separately stated loss from business activities of $550,000 and $10,000 of nondeductible meals & entertainment www.eidebailly.com www.eidebailly.com 13

Example 1 – [Reg. 1.1367-1(g)] • Under the ordering rules, the $10,000 nondeductible amount reduces basis before it is reduced by items of loss and deduction Beginning Basis $500,000 Less: Nondeductible M&E ($10,000) Basis before loss $490,000 Less: Loss (limited) ($490,000) Ending Basis $0 Loss Carried Forward ($60,000) Loss Utilized on 1040 ($490,000) www.eidebailly.com www.eidebailly.com 14

Example 2 – [Reg. 1.1367-1(g)] • If election made to reverse the ordering rules, the $10,000 nondeductible amount reduces basis AFTER it is reduced by items of loss and deduction Beginning Basis $500,000 Less: Loss (limited) ($500,000) Basis before n/d items $0 Carryforward Nondeductible M&E ($10,000) Loss Carried Forward ($50,000) Loss Utilized on 1040 ($500,000) www.eidebailly.com www.eidebailly.com 15

[Reg. 1.1367-1(g)] • The election to reduce basis by loss or deduction items before nondeductible expenses results in a higher deductible loss • The nondeductible item however carries over to future years and will reduce basis when there is sufficient basis to absorb it • If the election is not made, the nondeductible items do not carry over, even if basis is reduced to zero in the current year www.eidebailly.com www.eidebailly.com 16

When to Calculate Basis? • Normally calculated at the end of the corporation’s taxable year. [Reg. 1.1367 -1(d)] • Exceptions – • Disposal of entire shareholder interest • Disposal of substantial interest www.eidebailly.com www.eidebailly.com 17

Example Timing Rules • Sophia owns all of the shares of Princess, Inc., an S corporation that incorporated and elected S status on January 1, 2012. The corporation uses a September 30 year-end. Sophia's stock basis on January 1 is $500,000 • The corporation passes through a nonseparately stated loss from business activities of $550,000. The corporation made no distributions to Sophia during the year. At September 30th Sophia's basis is adjusted to $0 with a $50,000 loss carry over www.eidebailly.com www.eidebailly.com 18

Example Timing Rules • Sophia contributes an additional $50,000 to the company on October 1, 2012. Can she take the full $550,000 loss on her personal 2012 income tax return • No - Those increases in basis are considered in determining basis at the end of the corporation's next fiscal year, the corporate year-end not the shareholder year-end governs www.eidebailly.com www.eidebailly.com 19

Per-Share, Per-Day • Pass-through items are generally allocated per- share, per-day [IRC Sec. 1377(a)(1)] • Each item is divided by the number of days in the tax year, then that amount is allocated equally among the shareholders who held shares on each day – [IRC Sec. 1377(a)(1)] • Simplified method: the percentage of stock owned is multiplied by the percentage of the year that it is owned – [1120S Instructions] www.eidebailly.com www.eidebailly.com 20

Slide Intentionally Left Blank

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries