April 26, 2019

Prices coming down from peak levels • Higher vs Q1 2018, lower vs Q4 2018 Sales growth of 15% vs Q1 2018 • Price/mix 5%, volumes 5%, currency 5% EBITDA up 33% vs Q1 2018 + Higher prices and positive currency effects + Higher pulp volumes + Restructuring Wood France (SEK +90m) - Higher prices for wood raw material Increasing pulp volumes from Östrand ramp-up SCA Wood France merged with Groupe ISB • SCA retains 38.5% share in the combined company Acquisition of 10,000 ha forest land in Latvia (post Q1) 3

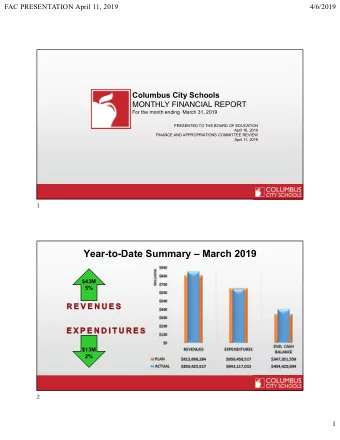

EBITDA (SEKm) Industrial ROCE 1) EBITDA development (SEKm) 1,560 17% 33% 1,560 1,549 1,494 1,175 1,034 33% 31% 30% EBITDA margin Net debt/EBITDA 27% 31% 1.6x 22% Q1 '18 Q2 '18 Q3 '18 Q4 '18 Q1 '19 Note: 1) ROCE for the industrial segments; Wood, Pulp and Paper. ROCE calculated as LTM. 4

Net sales (SEKm) EBITDA (SEKm) EBITDA margin 27% 9% Higher prices 331 23.4% 1,651 304 Increased wood sourcing to meet higher 20.0% 1,298 pulpwood demand Sales up 27% + Increased volumes to the expanded pulp mill + Higher prices Q1 2018 Q1 2019 Q1 2018 Q1 2019 Q1 2018 Q1 2019 EBITDA up 9% Price development – Pulpwood and Sawlogs + Higher prices 130 - Larger import volumes 120 110 100 90 Q1 '17 Q2 '17 Q3 '17 Q4 '17 Q1 '18 Q2 '18 Q3 '18 Q4 '18 Q1 '19 Pulpwood Sawlogs 5

Net sales (SEKm) EBITDA (SEKm) EBITDA margin SCA Wood France merged with Groupe ISB 12% 73% 297 17.7% 1,678 Stable delivery volumes 1,503 11.4% 172 Lower prices vs Q4 Sales up 12% + Increased volumes Q1 2018 Q1 2019 Q1 2018 Q1 2019 Q1 2018 Q1 2019 + Higher prices and positive currency effects Price development – Solid Wood Products EBITDA up 73% + Higher prices and positive currency effects 125 120 + Increased volumes and yield improvement 115 + Restructuring SCA Wood France (SEK +90m) 110 105 - Increased wood raw material costs 100 95 Q1 '17 Q2 '17 Q3 '17 Q4 '17 Q1 '18 Q2 '18 Q3 '18 Q4 '18 Q1 '19 Price index SEK 6

Average daily NBSK production (tonnes) Full capacity Full NBSK capacity of 900kt/year 2,500 12 months 18 months ramp-up ramp-up Ramp-up period of 12-18 months 2,000 Actual • 2020 first full year with full 1,500 capacity Production/deliveries on track 1) 1,000 • Q3 ’18 - 147kt / 105kt • Q4 ‘18 - 160kt / 145kt 500 Q1 ’19 - 172kt / 168kt • 0 Jan/18 Feb/18 Mar/18 Apr/18 May/18 Jun/18 Jul/18 Aug/18 Sep/18 Oct/18 Nov/18 Dec/18 Jan/19 Feb/19 Mar/19 Apr/19 May/19 Jun/19 Jul/19 Aug/19 Sep/19 Oct/19 Nov/19 Dec/19 Note: 1) Including CTMP. April production refers to 2019-04-01 to 2019-04-23. 7

Net sales (SEKm) EBITDA (SEKm) EBITDA margin Lower prices vs Q4 93% 97% 1,134 31.0% Increasing volumes due to the ramp-up of the 30.2% 351 expanded pulp-mill Sales up 93% 589 178 + Increased volumes + Higher prices and positive currency effects Q1 2018 Q1 2019 Q1 2018 Q1 2019 Q1 2018 Q1 2019 EBITDA up 97% + Increased volumes Price development – NBSK Pulp + Higher prices and positive currency effects 155 - Higher raw material costs 145 135 125 115 105 95 Q1 '17 Q2 '17 Q3 '17 Q4 '17 Q1 '18 Q2 '18 Q3 '18 Q4 '18 Q1 '19 Price index SEK 8

Net sales (SEKm) EBITDA (SEKm) EBITDA margin -1% Increased prices for Publication Paper 5% 616 26.0% 2,383 2,366 586 Lower prices for Kraftliner vs Q4 24.6% Sales down 1% - Lower volumes + Higher prices and positive currency effects EBITDA up 5% Q1 2018 Q1 2019 Q1 2018 Q1 2019 Q1 2018 Q1 2019 Price development – Price development – + Higher prices for Publication Paper Kraftliner Publication paper + Positive currency effects 160 160 + Improved product and market mix 140 140 - Higher raw material cost and lower volumes 120 120 100 Project for increased share of white-top kraftliner 100 progressing according to plan 80 80 Q1 Q1 Q1 Q1 Q1 Q1 '17 '18 '19 '17 '18 '19 Price index SEK 9

Initiate new wind projects New target 11 TWh Develop after market offering 2021 Target of 5.0 TWh by 2020 will be exceeded 6.7 TWh • 6.7 TWh secured by 2021 2020 New long-term target of 11.0 TWh 5.0 TWh EBIT target of SEK ~100m (6.7 TWh) Q1 2019 2.7 TWh 10

SCA’s forests bind CO 2 and 2 Replaces Higher growth enables more substitution – 5 replace fossil based products renewable alternatives replace fossil Mt CO 2 based products SCA’s renewable Non-renewable 1 products products Binds net Growing forests bind CO 2 – 4 active forest management Fossil Bioenergy increases growth fuels Mt CO 2 Fertilization Operations Paper Plastic Contorta pine 3 Solid-wood Concrete Investments and products innovation reduce Active carbon emissions silviculture Low Emissions 0.9 Improved SCA’s climate benefits amount to Mt CO 2 seedlings 8 million tonnes of CO 2 per annum, which is more than the total emissions from all the truck traffic and domestic air travel in Sweden* * Source: Swedish Environmental Protection Agency 11

Quarter SEKm Q1 2019 Q1 2018 Change Net sales 5,076 4,400 15% EBITDA 1,560 1,175 33% EBITDA margin 30.7% 26.7% 4.0 p.p. EBIT 1,168 889 31% EBIT margin 23.0% 20.2% 2.8 p.p. Financial items -30 1 Profit before tax 1,138 890 28% Tax -230 -191 Profit for the period 908 699 30% Earnings per share, SEK 1.29 1.00 13

Forest Wood Pulp Paper 2,383 2,426 2,413 2,421 2,366 Net sales (SEKm) 2,220 2,096 2,072 1,846 1,712 1,678 1,651 1,637 1,567 1,558 1,540 1,503 1,455 1,426 1,298 1,287 1,261 1,210 1,162 1,134 1,049 743 672 644 585 589 485 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 '17 '17 '17 '18 '18 '18 '18 '19 '17 '17 '17 '18 '18 '18 '18 '19 '17 '17 '17 '18 '18 '18 '18 '19 '17 '17 '17 '18 '18 '18 '18 '19 EBITDA (SEKm) and EBITDA margin 728 586 618 616 536 439 481 37% 35% 427 31% 30% 371 364 316 358 370 351 331 25% 22% 292 297 291 304 230 276 226 273 32% 30% 30% 25% 28% 28% 154 187 184 172 22% 26% 21% 22% 25% 26% 12% 178 23% 158 149 20% 20% 12% 13% 11% 13% 16% 15% 18% 71 14% -112 9% Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 '17 '17 '17 '18 '18 '18 '18 '19 '17 '17 '17 '18 '18 '18 '18 '19 '17 '17 '17 '18 '18 '18 '18 '19 '17 '17 '17 '18 '18 '18 '18 '19 14

Higher pulp volumes Positive for all segments SEK 5,076m 5% 5% SEK 5% 4,400m Positive EUR and USD + 15% Net sales Price/Mix Volume Currency Net sales Q1 2018 Q1 2019 15

Higher costs for wood raw material EUR and USD positive Higher prices for all segments SEK SEK SEK SEK SEK +46m 1,560m SEK +95m -173m +118m SEK +248m +51m SEK 1,175m Restructuring SCA Wood France Higher pulp Improved energy balance volumes in expanded pulp mill + 33% EBITDA margin EBITDA margin 26.7% 30.7% EBITDA Price/Mix Volume Raw material Energy Currency Other EBITDA Q1 2018 Q1 2019 16

Quarter SEKm Q1 2019 Q1 2018 EBITDA 1,560 1,175 Revaluation of biological assets and other non cash flow items -246 -253 Operating cash surplus 1,314 922 Change in working capital -353 -159 Current capital expenditures -168 -76 Other operating cash flow -167 -96 Operating cash flow 626 591 Strategic capital expenditures -143 -634 17

SEK SEK SEK +1,211m +15m 9,150m SEK +1,229m SEK SEK SEK SEK 7,020m -626m +158m +143m Net debt / EBITDA Net debt / EBITDA 1.3x 1.6x Net debt Operating Strategic capex Acquisitions Dividend Leasing effect Other Net debt Q4 2018 cash flow (IFRS 16) Q1 2019 18

SEKm Mar 31, 2019 Dec 31, 2018 Forest assets according to IAS 41 1) 32,298 32,065 Deferred tax relating to Forest assets -6,653 -6,605 Forest assets, net of deferred tax 25,645 25,460 Working capital 3,955 3,735 Working capital/Net sales 2) 18% 18% Other capital employed 18,174 16,887 Total capital employed 47,774 46,082 Net debt 9,150 7,020 Net debt/EBITDA 3) 1.6x 1.3x Equity 38,624 39,062 Net debt/Equity 24% 18% Note: 1) Gross value before deferred taxes. 2) Average working capital for 13 months as a 19 percentage of 12-month rolling net sales. 3) 12-months EBITDA, up to end of each period.

Prices coming down from peak levels Sales growth of 15% vs Q1 2018 EBITDA up 33% vs Q1 2018 Increasing pulp volumes from Östrand ramp-up SCA Wood France merged with Groupe ISB Acquisition of 10,000 ha forest land in Latvia (post Q1) 20

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries