Agenda 1. FY2018 Audit Results 2. FY2020 Budget Timeline 3. FY2020 Budget Update: Revenue Projections Appendix Engage. Inspire. Prepare. April 23, 2019

Engage. Inspire. Prepare. FY2018 Audit Results Annual Financial Report, Including Independent Auditor’s Reports Performance Audit on SPLOST

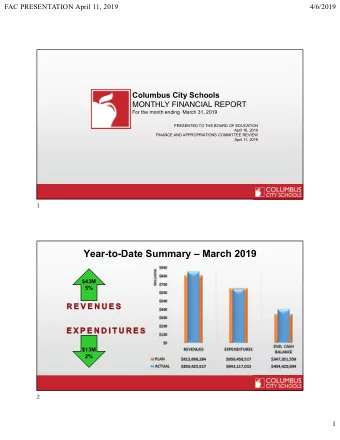

FY2018 Audit Documents 1 | FY2018 Audit Results

“In our opinion, the financial statements… present fairly, in all Purpose 1: material respects, the Express an opinion respective financial as to whether the position of the financial statements Audit governmental are in conformity Results activities…in accordance with generally with accounting accepted accounting principles generally principles (GAAP) accepted in the United States of America.” March 26, 2019 Audit Letter FY2018 Independent Auditor’s Report Independent Auditor’s Report Summary 1 | FY2018 Audit Results

Financial Statements: 1. Unmodified Opinion 2. No Internal Control Material Weakness or Significant Purpose 2: Deficiencies Identified Audit financial 3. No Noncompliance Noted statements (content) 4. No Findings or Questioned Costs and compliance with Audit Federal grant Federal Awards (Compliance): Results 1. Unmodified Opinion requirements, per 2. No Internal Control Material OMB Circular A ‐ 133 Weakness or Significant (Single Audit) Deficiencies Identified 3. Low ‐ Risk Auditee 4. No Findings or Questioned Costs Last Section of the FY2018 Independent Auditor’s Report Independent Auditor’s Report Summary 1 | FY2018 Audit Results

Objectives Results Objective #1: To determine whether the schedule of Results: Expenditures tested were related to activities “Based on the results projects adheres to the approved resolution adopted by approved in the SPLOST resolutions. the Paulding County School District. of our audit, we Objective #2: To determine that the reporting Results: [The] School District has an effective method in conclude that the effectiveness between the School District and the place to communicate with the Board in regard to the Board of Education communicates the status of capital financial and construction status of each project to Paulding County outlay projects to ensure that legislative, regulatory and ensure that legislative, regulatory, and organizational organizational goals and objectives were achieved. goals and objectives are achieved. School District's Objective #3: To determine the reliability of the Results: Adequate processes are in place to monitor monitoring function to verify that actual project expenditures to ensure that actual project expenditures SPLOST Program is expenditures are not exceeding budgeted amounts. do not exceed budgeted amounts. Objective #4: To determine whether there is an Results: [The] Board has an effective program in place effective means of monitoring program performance to monitor program performance and to ensure the operating in within a projected timeline, to evaluate the validity of timely completion of each capital project within the expenditures, and to evaluate the timely completion of projected timeline. compliance with all each capital project. Objective #5: To determine the reliability, validity or Results: There is an adequate process in place to applicable laws and relevance of financial analyses to verify that cash flows monitor cash flows to ensure that financial analyses to conform to forecasted projections by project and verify that cash flows conform to forecasted projections regulations, the priority, and that intended economic results are by project and priority are reliable, valid, and relevant accomplished. and that the intended economic results are referendum approved accomplished. Objective #6: To determine whether effective Results: Effective procedures are in place to verify that by the County's procedures exist to verify that design and construction the design and construction of capital projects adhere of capital projects adhered to applicable quality control to applicable quality control standards. citizens, and industry standards. Objective #7: To determine the effectiveness of Results: Effective financial controls are in place to best practices.“ financial controls in place to ensure that the receipt and ensure that the receipt and expenditure of tax revenue disbursement of tax revenue funds are in compliance funds are in compliance with applicable laws and Mauldin & Jenkins with applicable laws and regulations. regulations. Objective #8: To determine whether the School District Results: [The] School District is following procurement is following Board approved procurement policies and policies and procedures. procedures. SPLOST Performance Audit Summary 1 | FY2018 Audit Results

Today: April 23, 2019 Revenue Projections 1 st Public Hearing on Proposed Budget Budget Approval Timeline 2 | Budget Timeline

Major Budget Influencers (MBI) must also be identified and considered within the framework, especially changes in funding and new or expanding influences on the budget, which may be positive or negative and short ‐ term or long ‐ term . Major Revenue Influencers Major Expenditure Influencers Enrollment Growth Enrollment Growth State Budget (Security Grant and Mental Health) ESEP QBE: State Teacher Scales (Local Enrollment (Weighted) Impact) Local Fair Share Step Increases Teacher Pay Scale TRS Equalization Grant: • Custodial Services Rollback Impact Wealth per Weighted FTE Changes in Local Sources: Property Taxes (MR) TAVT Major Budget Influencers 2 | Budget Timeline

Engage. Inspire. Prepare. Organization ‐ wide Factors Influencing Decisions: Funding Factors (Preliminary)

FY2018 Statewide Revenue Sources FY2018 PCSD Revenue Sources Local Revenue State Revenue Federal Revenue Local Revenue State Revenue Federal Revenue 4% 6% 30% 41% 53% 5% 67% 24% Dependency on State Sources. With approximately 67% of revenue 71% coming from State sources (compared to a statewide average of 53%) FY2014 the District is highly susceptible to changes in State funding, including austerity reductions, Equalization Grant funding and changes in the Quality Basic Education (QBE) methodology. Source: GaDOE School System Revenue/Expenditures Report as of FY2018 Dependency on State Sources 3 | Budget Update

FY2018 1 Low Wealth. Despite favorable employment, income and free ‐ 2 3 and ‐ reduced lunch statistics, PCSD is considered low wealth due 4 to a limited commercial and industrial tax base and the large 5 6 number of school ‐ age children per household. 7 8 State Revenue 9 10 13 th Largest District as of FY2018 11 • 12 13 Students 31 st in Local Revenue per Student (128 vs 180) • 14 Collect $1,235 less than Average per Student or $36 million * 15 16 17 8 th in State Revenue per Student (85 vs 180) • 18 19 Collect $775 more than Average per Student 20 3 rd Largest Recipient of Equalization ($27 million) 21 22 Equalization is declining, influenced by wealth per weighted FTE * 23 24 and local revenue (millage rate) 25 26 29 th in Total Revenue per Student (154 vs 180) • 27 28 Collect $710 or 7% less than Average per Student or $21 million 29 Total Revenue 30 31 Local Revenue *See Appendix form more information 32 33 34 Source: GaDOE School System Revenue/Expenditures Report as of FY2018 35 Average per Student: 35 Large Georgia School Districts with >10,000 FTE (180 total) Ranking Low Wealth: Total per Pupil Funding 3 | Budget Update

Projected General Fund Highlights 3 | Budget Update

FY2019 FY2020 Change % Salaries (FTE/T&E) $ 145.14 $ 157.0 $ 11.9 8.2% Operations $ 12.8 $ 13.1 $ 0.2 1.8% LFS $ (18.9) $ (20.9) $ (2.0) 10.7% Transportation $ 1.4 $ 1.5 $ 0.1 5.6% Nursing $ 0.6 $ 0.6 $ 0.0 3.3% Health Insurance $ 19.1 $ 19.5 $ 0.4 2.1% Total $ 160.2 $ 170.8 $ 10.6 6.6% $1.5 , 1% $0.6 , 0% • $10.6m Increase $17.3 , 10% • 6.6% Growth $11.6 , 7% • $(20.9m) Local Fair Share • $8.6m for $3,000 CE Increase • $633k for T&E • $1.3m for Enrollment Growth $139.7 , 82% and Categorical (Excluding Equalization) Salaries Operations Health Insurance Transportation Nursing (millions) (1) Projected QBE Funding Highlights 3 | Budget Update

Historical Equalization Grant (millions) $40.0 $8.9 $35.0 $(2.3) $1.7 $(0.3) $(2.6) $30.0 $(2.1) $(0.6) $5.0 $25.0 $1.1 $3.9 $5.2 $20.0 $1.0 $(5.6) $2.0 $0.2 $15.0 $3.0 $2.1 $10.0 $5.0 $ ‐ FY20 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 (P) EG $8.2 $10.3 $13.4 $13.5 $15.5 $20.7 $21.9 $16.3 $17.3 $21.2 $26.1 $35.0 $32.7 $30.0 $27.9 $27.4 $29.0 $28.8 EG Impact from FY2018 Rollback: $(3.0m) EG Impact from FY2018 0.125 Reduction: $(0.5m) Cumulative EG Impact from FY2016 Rollback: $(11.2m) (2) Projected Equalization Grant Highlights 3 | Budget Update

FY2019 FY2020 Change % Ad Valorem $ 75.8 $ 82.2 $ 6.4 8.5% Title Ad Valorem $ 6.8 $ 9.4 $ 2.7 39.4% Other Sales Taxes $ 2.7 $ 2.5 $ (0.1) ‐ 5.6% Other Taxes $ 0.0 $ ‐ $ (0.0) 0.0% Total $ 85.2 $ 94.2 $ 8.9 10.5% • $8.9m Increase $2.5 , 3% $9.4 , 10% • 10.5% Growth • 87% Ad Valorem • 6.4m Ad Valorem Increase (18.879) ~$800k at Rollback ( ‐ $5.6m) o ~$5.9m at 18.750 ( ‐ $0.5m) o ~$4.8m at 18.500 ( ‐ $1.6m) o • $1.8m TAVT Increase from $82.2 , 87% HB329 Formula Change ($2.7m Total) Ad Valorem Title Ad Valorem Other (millions) (3) Projected Local Taxes Highlights 3 | Budget Update

Projected Changes in Revenue 3 | Budget Update

Projected Changes in Revenue 3 | Budget Update

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries