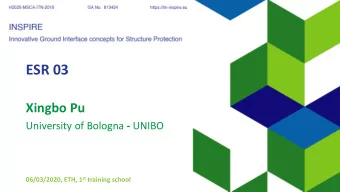

Agenda MEASUREMENT METHODS I. Overview of the ACA o Individual - PDF document

Steps to Compliance: Understanding Measurement Methods under ESR ACA COMPLIANCE Understanding The Measurement Methods Under Employer Shared Responsibility Susan L. Grassli, J.D. April 2016 Agenda MEASUREMENT METHODS I. Overview of the ACA o

Steps to Compliance: Understanding Measurement Methods under ESR ACA COMPLIANCE Understanding The Measurement Methods Under Employer Shared Responsibility Susan L. Grassli, J.D. April 2016 Agenda MEASUREMENT METHODS I. Overview of the ACA o Individual Mandate o The Exchange / Health Insurance Marketplace o Employer Shared Responsibility / Employer Mandate o Market Reforms II. Employer Shared Responsibility o Introduction, Overview and Review of Steps 1, 2 and 3 o The Measurement Methods • Monthly Measurement Method • Look ‐ Back Measurement Method o How to Use the Look ‐ Back Measurement Method • Standard Look ‐ Back & Stability Period Method • Initial Look ‐ Back & Stability Period Method o Next Steps • Overview of 4 Steps to compliance with Employer Shared Responsibility Measurement Methods Under ESR 2 GBS Benefits, Inc. GBS Benefits, Inc

Steps to Compliance: Understanding Measurement Methods under ESR The Basic Parts of the ACA OVERVIEW Individual Shared Responsibility Employer Market ACA Shared Reforms Responsibility Exchanges (Marketplaces) & Subsidies Measurement Methods Under ESR 3 GBS Benefits, Inc. EMPLOYER SHARED RESPONSIBILITY: Introduction, Overview and Review of Steps 1,2 and 3 GBS Benefits, Inc

Steps to Compliance: Understanding Measurement Methods under ESR Steps to Compliance ESR: INTRODUCTION STEP 4 Determine Which Employees will be Offered Coverage and When STEP 3 Determine What will be Offered STEP 2 Determine Compliance Date STEP 1 Determine Employer Size Measurement Methods Under ESR 5 GBS Benefits, Inc. Step 1: EMPLOYER SHARED Determine Employer Size RESPONSIBILTY STEP 4 Determine Which Employees will be Offered Coverage and When STEP 3 Determine What will be Offered STEP 2 Determine Compliance Date STEP 1 Determine Employer Size Measurement Methods Under ESR 6 GBS Benefits, Inc. GBS Benefits, Inc

Steps to Compliance: Understanding Measurement Methods under ESR Step 1: EMPLOYER SHARED Determine Employer Size RESPONSIBILTY o An employer must know it’s official size as determined under Employer Shared Responsibility rules o Factors when determining size: • Control groups and affiliated services groups — Include in count all employees from all entities that are part of the same controlled group or affiliated services group — For more information, see our summary entitled: Controlled Groups and Affiliated Service Groups under Health Care Reform • Contingent employees — These are employees associated with temporary or leasing agencies or PEOs — Must make determination under the rules regarding which contingent employees to count — For more information, see our summary entitled: Contingent Workers: Is the Staffing Agency or the Client Employer Liable under the Employer Mandate? • Full ‐ time employee equivalents and seasonal employees — There are specific rules on how to calculate full ‐ time employee equivalents — There is a specific definition and rule about seasonal employees and whether to count them in the calculation Steps to Compliance: ESR & Information Reporting 7 GBS Benefits, Inc. Step 2: EMPLOYER SHARED Determine Compliance Date RESPONSIBILTY STEP 4 Determine Which Employees will be Offered Coverage and When STEP 3 Determine What will be Offered STEP 2 Determine Compliance Date STEP 1 Determine Employer Size Measurement Methods Under ESR 8 GBS Benefits, Inc. GBS Benefits, Inc

Steps to Compliance: Understanding Measurement Methods under ESR Step 2: EMPLOYER SHARED Determine Compliance Date RESPONSIBILTY o Compliance date varies for Employer Shared Responsibility depending on several factors • There used to be one compliance date – January 1, 2014 • Now, there are now several possible effective dates based on employer size, calendar year v. non ‐ calendar year plans, past v. current plan changes, and qualification for transition rules o Summary of Effective Dates • Large employer (100 or more) — January 1, 2015 — Possible 2015 non ‐ calendar year plan compliance date if qualify for transition rule • Medium employer (50 to 99) — January 1, 2015 — Possible 2016 compliance date if qualify for transition rule • Small Employer (under 50) — No compliance date for Employer Shared Responsibility Measurement Methods Under ESR 9 GBS Benefits, Inc. Step 3: EMPLOYER SHARED Determine What will be Offered RESPONSIBILTY STEP 4 Determine Which Employees will be Offered Coverage and When STEP 3 Determine What will be Offered STEP 2 Determine Compliance Date STEP 1 Determine Employer Size Measurement Methods Under ESR 10 GBS Benefits, Inc. GBS Benefits, Inc

Steps to Compliance: Understanding Measurement Methods under ESR Step 3: EMPLOYER SHARED Determine What will be Offered RESPONSIBILTY o There are two possible penalties if employer doesn’t offer an ACA compliant plan o What needs to be offered to avoid exposure to first penalty • To avoid the 4980H(a) penalty, large employers must offer Minimum Essential Coverage (MEC) to substantially all full ‐ time employees, and their dependents – A plan offered by an employer is generally MEC – “Substantially All” is defined as 95% of full ‐ time employees o What needs to be offered to avoid exposure to second penalty • To avoid the 4980H(b) penalty, large employers must also offer to full ‐ time employees and their dependents a plan that meets: – Affordability – Minimum Value Steps to Compliance: ESR & Information Reporting 11 GBS Benefits, Inc. Step 3: EMPLOYER SHARED Determine What will be Offered RESPONSIBILTY o To avoid both penalties: • Offer health coverage to at least 95% of full ‐ time employees • Check Minimum Value — Employer must pay at least 60% of the total allowed covered costs under the plan. (This does not relate to the monthly premium but instead most all other costs). • Check Affordability — Monthly premium for single coverage must not exceed 9.66 % of any full ‐ time employee’s household income. To do this, select one of 3 safe harbors: » W ‐ 2 method » Rate of Pay method » Federal Poverty Level method Measurement Methods Under ESR 12 GBS Benefits, Inc. GBS Benefits, Inc

Steps to Compliance: Understanding Measurement Methods under ESR Step 4: EMPLOYER SHARED Determine Which Employees will be Offered Coverage & When RESPONSIBILTY STEP 4 Determine Which Employees will be Offered Coverage and When STEP 3 Determine What will be Offered STEP 2 Determine Compliance Date STEP 1 Determine Employer Size Measurement Methods Under ESR 13 GBS Benefits, Inc. Step 4: EMPLOYER SHARED Determine Which Employees will be Offered Coverage & When RESPONSIBILTY o Employees who work full ‐ time, and their dependents, should be offered coverage • Full ‐ time employee = 30 hours per week or 130 average hours per month • Dependents = employee’s children up through age 26, does not include the spouse o Identifying full ‐ time employees is based simply on tracking and counting hours • It doesn’t matter how an employer classifies employees for other purposes. — For example, outside the ACA an employee may be classified as part ‐ time, temporary, or seasonal, but under the ACA, if an employee works the requisite hours, she will be full ‐ time and will need to be offered coverage to avoid exposure to possible penalties. o Tracking hours includes hours actually worked plus other hours for which an employee is paid. Together, these hours are called “Hours of Service” Steps to Compliance: ESR & Information Reporting 14 GBS Benefits, Inc. GBS Benefits, Inc

Steps to Compliance: Understanding Measurement Methods under ESR Step 4: EMPLOYER SHARED Determine Which Employees will be Offered Coverage & When RESPONSIBILTY o All “Hours of Service” should be counted when tracking • Count all hours worked — Hours actually worked — Overtime hours • Count credited hours — Hours for which an employee is paid or entitled to payment even when no work is performed » Examples: vacation, holiday, illness, incapacity/disability, layoff, jury duty, military duty o If not paid hourly: • Switch to tracking actual hours of service, OR • Use Equivalency hours method: Days Worked method or Weeks Worked method — Days worked method: 8 hours for each full or partial workday — Weeks worked method: 40 hours for each full or partial work week Steps to Compliance: ESR & Information Reporting 15 GBS Benefits, Inc. Step 4: EMPLOYER SHARED Determine Which Employees will be Offered Coverage & When RESPONSIBILTY o Counting hours can be done in many ways and some may not create accurate results if employees work anything other than consistently full ‐ time or part ‐ time hours — To help resolve the issue, regulators came up with a Safe Harbor to help process of identifying full ‐ time employees — The safe harbor includes: » the Monthly Measurement method » the Look Back Measurement method Steps to Compliance: ESR & Information Reporting 16 GBS Benefits, Inc. GBS Benefits, Inc

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.