2020 CARES Act: SBA EIDL and PPP Loans Webinar FRIDAY, APRIL 3, 2020

HOUSEKEEPING ITEMS All attendees have been muted. You will only hear George and Angie speaking. CHAT FEATURE: Use only to send a technical message directly to Angie if you are having issues with the webinar. Q&A FEATURE: If you have a question about the information being presented, type in your question in the Q&A. Your questions will be hidden from other attendees, but we will repeat and answer the question aloud during the broadcast. 3

T ODAY ’ S P RESENTER : G EORGE S. D AUGHARTY , CPA Principle – Daugharty & Company, P.C. • • Earned a Master in Professional Accounting degree from the University of Texas-Austin Over 25 years as a CPA, including experience on • the corporate side as well as in public accounting with a “Big Four” firm • Lived A number of years in Atlanta, GA prior to settling with his family in the beautiful Shenandoah Valley in 2006 4

CARES Act • On March 27, 2020 the House of Representatives passed the Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”), commonly known as “Phase Three” of coronavirus economic relief. President Trump signed the bill into law the same day. • The CARES Act provides much needed stimulus to individuals, businesses, and hospitals in response to the economic distress caused by the coronavirus (COVID-19) pandemic. 5

Small Business Administration (SBA) Loans PAYCHECK PROTECTION PROGRAM (PPP) ECONOMIC INJURY DISASTER LOAN (EIDL) 6

PAYCHECK PROTECTION PLAN (PPP) Covers the period February 15, 2020 through June 30, 2020. Allows business suffering due to the coronavirus outbreak to borrow money for a variety of qualified costs related to employee compensation and benefits including Employee Interest on Continuation compensation Mortgage debt incurred Payroll costs of health care (of those interest Rent Utilities before the benefits making less obligations covered period than $100K) 7

PAYCHECK PROTECTION PLAN (CONTINUED) • Eligible companies employ no more than 500 employees • Maximum amount is 250% of the average monthly amount spent on gross payroll, payments to independent contractors, and payments to owners • Repayment of the loan may be deferred 6 months at an interest rate of 1.0 – 4.0 %, due in 2 years • All or a portion of the of the loan may be forgivable: • The borrower is eligible for loan forgiveness equal to the amount spent by the borrower on payroll and certain other business expenses during an 8-week period after the origination date • Of the amount forgiven, up to 25% can be for amounts spent on rent, or mortgage interest, and utilities so long as the remaining 75% is spent on payroll The amount forgiven may not exceed the principal of the loan • • The forgiveness provisions are to effectively pay employers to retain employees and to rehire any employees who have already been laid off due to the COVID-19 crisis No collateral is needed, and the loan will be an unsecured loan • 8

PAYCHECK PROTECTION PLAN (CONTINUED) • PPP loans and EIDL advance loans • Call your bank or lending cannot be used for the same purpose institution to apply. The following local and regional banks are some • Starting April 3, 2020, small business of the SBA approved lenders: and sole proprietorships can apply • Starting April 10, 2020, independent • Blue Ridge Bank contractors and self ‐ employed • Farmers & Merchants Bank individuals can apply • First Bank & Trust Company • Other regulated lenders will be available to make these loans as soon • Park View Federal Credit Union as they are approved and enrolled in the program • Pendleton Community Bank • United Bank 9

PAYCHECK PROTECTION PLAN (CONTINUED) The application is two pages The list of required items is as follows (F&M Bank): • Copies of payroll tax reports filed with the IRS (including Forms 941, 940, state income and unemployment tax filing reports) for the entire year of 2019 and the first quarter of 2020. • Copies of payroll summary reports for each pay period for the preceding 12 months and year-to-date to include gross wages including PTO. • Documentation reflecting health insurance previous paid by the company under a group health plan including owners of the company for the 12 months immediately preceding the date of the SBA loan origination. • Documentation of all retirement plan funding by the employer for the immediately preceding 12 months. • Signed SBA Paycheck Protection Program Loan Application (SBA Form 2483). • Complete Certificate of Incumbency and Beneficial Ownership Information • 2019 Balance Sheet (to include specific breakdowns as to Fixed Assets; Other Assets; Inventory; Recs; Cash; Accts Payable; Current Liabilities; and Current LTD) • 2019 Income Statement (to include specific breakdowns as to Depreciation; Owner Salaries; Income Taxes; Net Income After Taxes; COGS; Recs; etc.). • Copy of current and unexpired State issued drivers license or US Passport. • SBA Loan excel Worksheet showing maximum loan amount. 10

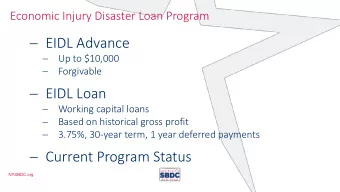

ECONOMIC INJURY DISASTER LOAN (EIDL) Covers the period January 31, 2020 through December 31, 2020. Business with no more than 500 employees that have been directly affected by the disaster are eligible to apply. SOME INELIGIBLE BUSINESSES Agricultural Religious Charitable Gambling Casinos & Enterprises Organizations Organizations Concerns Racetracks 11

ECONOMIC INJURY DISASTER LOAN (CONTINUED) APPLICAN APPLICANTS MA TS MAY REQUES Y REQUEST AN T AN AD ADVANCE OF E OF UP UP TO How w can I us can I use e the e loan funds? loan funds? $10,0 $1 0,000 WITH WITHIN THREE D IN THREE DAYS AFTER THE AFTER THE • Fixed debts (rent, etc.) APPLICA APPL ICATIO ION IS RECEIV N IS RECEIVED AND IS NO AND IS NOT SUBJE T SUBJECT T TO • Accounts payable REP REPAYMENT ENT, EVEN EVEN IF THE L IF THE LOAN REQUES AN REQUEST IS IS • Payroll ULTIM UL TIMATELY DENIED. DENIED. • Some bills that could have been paid had the What are What are the collat the collateral req ral requirements? irements? disaster not occurred • No collateral required for EIDLs under $25,000 Ho How much can w much can I borr I borrow? • Up to $2 million • SBA takes real estate as collateral when it is available • Interest rates • Small Businesses 3.75% • SBA will not decline a loan for lack of collateral, • Most Private, Non-Profits 2.75% but requires borrowers to pledge what is available • Terms up to 30 years • Eligibility based on the size, type of business, and EIDLs may EIDLs ma y be be appr approved solely on the ed solely on the basis of basis of an an applicant applicant’s s credit score or b credit score or by use of an alt use of an alternativ rnative e financial resources me method t thod to gauge the gauge the applicant applicant’s ability s ability to repa repay. 12

ECONOMIC INJURY DISASTER LOAN (CONTINUED) • PPP loans and EIDL advance loans cannot be used for the same purpose • Apply directly on the SBA website at https://covid19relief.sba.gov/#/ • Ineligible Uses of Loan: • Dividends and bonuses • Disbursement to owners except when directly related to performance of services • Repayment of stockholder/principal loans, except when loans are because of the disaster and repayment would cause hardship • Expansion of facilities or acquisition of fixed assets • Repair or replacement of physical damages • Refinancing long term debt • Paying down or paying off loans provided, or owned by another Federal agency or a Small business investment company • Payment of any part of a direct Federal debt, except IRS obligations • Relocation 13

ECONOMIC INJURY DISASTER LOAN (CONTINUED) Basic Filing Requirements The SBA has established a streamlined process for those applying for the COVID-19 Economic Injury Disaster Loan. This streamlined process requires applicants to self certify they are eligible for the loans. The streamlined application is completed online and does not require any supporting documentation. We do not know, at this time, what additional items will be requested after the streamlined application has been submitted. 14

Comparison of the SBA EIDL and PPP Loan Programs EIDL PPP 15

Comparison of the SBA EIDL and PPP Loan Programs EIDL PPP 16

A DVICE ICE BASED ASED ON ON WHA WHAT WE WE KNO KNOW NO NOW FOR OR APPLICANTS APPLICANTS 1. 1. ACT SO SOON: ON: The CARE Act budgeted a set amount for these programs. We feel there are more potential applicants than the amount designated to fund these programs, so apply now. 2. 2. CHOOS CHOOSE AN SBA AFFILIA E AN SBA AFFILIATED BANK: ED BANK: Some banks have stated they are not going to participate in the PPP program, are complaining that they are not making enough money off the program, or are saying they are not getting enough guidance. So, we strongly recommend you find a bank that is an SBA lender and that is publicly and clearly stating they are participating with the PPP. 3. 3. INCL CLUDE AL UDE ALL YOUR UR “P “PAYROLL LL” AL ” ALLOWABL BLE: E: Make sure you correctly include the following amounts when preparing the excel spreadsheet used for your PPP application: Group Health Insurance Payroll Tax Self-Employed Income (and subcontractors.) 17

E XAMPLE XAMPLE : H : H OW OW YOUR PPP PPP LOAN AN AMOUNT AMOUNT IS IS CAL CALCULA ULATED ED 18

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries