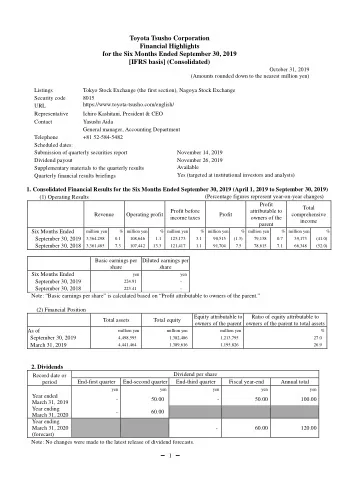

Yap ı Kredi Investor Presentation Yap ı Kredi Investor Presentation Merrill Lynch Turkish Equity 1 1 Conference Merrill Lynch Turkish Equity 1-1 Conference London, 19-20 January 2009

AGENDA � Current macro and sector outlook � Current macro and sector outlook � Summary 9M08 results* and latest developments � 2008YE preliminary highlights & 2009 outlook � 2008YE preliminary highlights & 2009 outlook (*) BRSA Consolidated 2

Starting from end of Sep‘08, Turkish economy negatively impacted by the acceleration of international financial and economic turmoil, albeit at a slower pace albeit at a slower pace Current Macro and Sector Outlook GDP (y/y growth, %) � Production and consumption still in positive territory in 3Q08, albeit p y Q , expected to contract in 4Q08 � Slowdown in GDP growth to 0.5% in 3Q08; contraction of industrial output for the last four months � Expected GDP growth of 0.8% in 2008 and -1.0% in 2009 vs average annual growth of 6.8% between 2002-2007 Industrial Output (y/y growth, %) � Main factors behind expected sluggish economic growth in 2009 : � Weak foreign demand for exports � Volatility in financial markets � High interest and exchange rates � High interest and exchange rates � Increasing unemployment � Weak consumer confidence Note: 2009 Forecasts as 23 January 3

Downward trend in inflation in 2H08 mainly driven by sluggish demand and falling commodity prices; CBT aggressively pursuing easing cycle with limited impact on currency easing cycle with limited impact on currency Current Macro and Sector Outlook CPI inflation (y/y growth, %) � Inflation on an upward trend in 1H08 due to surge in 1H08 due to surge in international food and energy prices while on a downward trend in 2H08 driven by stagnant demand and rapid fall in commodity prices (CPI: 7.8% 2009F vs 10.1% 2008) � Central Bank aggressively Benchmark Bond and Central Bank Policy Rates (%) pursuing easing cycle from Nov’08 onwards with bond rates 27% 25% declining in parallel declining in parallel 23% � Key risk factors for disinflation 21% 19% in 2009: 17% High risk perception and High risk perception and � � 15% capital flight 13% Weak TL and strong Dec-07 Jan-08 Mar-08 Apr-08 May-08 Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov-08 Dec-08 Jan-09 � exchange rate pass-through B Bond rate (annual compound) d t ( l d) CB ON rate (annual compound) CB ON t ( l d) Note: 2009 Forecasts as 23 January 4

Easing trend in current account deficit driven by deceleration in economic activity starting from end of Sep’08; positive contribution of FDI to financing of current account deficit of FDI to financing of current account deficit Current Macro and Sector Outlook Foreign Trade (USD bn) � Slowdown in exports in 4Q08, along with weak global demand along with weak global demand � Larger contraction in imports coupled with stagnant domestic demand and falling commodity demand and falling commodity prices � Expected decline in exports and imports in 2009 by 16% and 23%, p y , respectively, driven by weak Current Account Deficit (as % of GDP) foreign and domestic demand � As a result, current account deficit becoming less of an external financing risk in 2009 � As of Nov’08, net FDI inflows reached USD 13.7 bln, despite global problems ; expected USD 10 bln net FDI in 2009 Note: 2009 Forecasts as 23 January 5

Turkey less affected by the global financial turmoil than most other emerging market peers emerging market peers 5Y Credit Default Swaps (USD, bps) � Turkey has been relatively less Vs 3Q08 affected by the global financial crisis as y g 432 evidenced by comparative CDS Turkey +135 bps spreads with major CEE countries 748 +486 bps Russia � Ongoing talks for and expectation of a 795 795 +360 bps 360 b new IMF stand-by deal providing Kazakhstan further stability in Turkey vs most 833 +503 bps Latvia peers 413 413 +275 bps 2 b � Turkey is less vulnerable in terms of Croatia capital outflows vs other CEE 617 +357 bps Romania countries as a result of lower and 473 further reduced current account further reduced current account Bulgaria +248 bps deficit 245 +171 bps Poland � Agressive rate cuts by the Central 172 Bank (375 bps in 3 months since Bank (375 bps in 3 months since +112 bps +112 bps Slovakia Slovakia November 2008) expected to help 193 +130 bps Czech Rep. economic activity to pick up earlier Current 379 +213 bps than anticipated 4Q08 Hungary g y 3Q08 3Q08 6

Despite a challenging fourth quarter, the banking sector is still solid in terms of liquidity and capitalization q y p Current Macro and Sector Outlook 1Q08 ∆ 2Q08 ∆ 3Q08 ∆ 4Q08 ∆ Banking Sector 2008 Solid loan growth in the first 3 quarters of � Total Loans 11% 8% 6% 2% 30% 2008 followed by contraction in both TL and TL Loans 7% 10% 7% -4% 22% FC loans in all categories (except for credit FC loans in all categories (except for credit FC Loans (in USD) 12% 6% 4% -6% 16% cards) in 4Q due macroeconomic slowdown Consumer Loans 9% 8% 8% -2% 24% and banks’ cautious stance 10% 7% 5% -2% 21% Mortgage Rising trend in NPL ratio as a function of � -2% 1% 1% -10% -9% Auto loan contraction and asset quality 10% 10% 10% 10% 11% 11% -1% 1% 33% 33% General Purpose General Purpose deterioration in SME, credit cards and Credit Cards 5% 11% 4% 6% 29% consumer loans Corporate 13% 7% 6% 2% 32% Banking sector still sound and healthy: � Total Deposits 8% 5% 3% 8% 27% � Implementation of intensive restructuring TL 7% 5% 7% 5% 27% in aftermath of 2001 crisis thoroughly in aftermath of 2001 crisis thoroughly FC (in USD) FC (in USD) 0% 0% 10% 10% -3% 3% -9% 9% -3% 3% addressing weaknesses 3.1% 3.0% 3.0% 3.4% 3.4% NPL Ratio � No imminent liquidity problems and Loans / Deposits 82% 84% 87% 82% 82% limited reliance on wholesale funding ** 16.0% 15.3% 16.1% 15.4%* CAR � Sector well capitalised with CAR well Sector NPL Ratio Sector NPL Ratio above regulatory limits vs peer countries Credit Cards � No toxic assets on banks’ balance sheets 8.0% 6.7% 7.0% � Limited FX risk 6.0% Total Loans Effective measures taken by Central Bank: � 5.0% 3.4% 4 0% 4.0% � Opening of interbank FX deposit market O i f i t b k FX d it k t Commercial Loans 3.0% 3.3% where CBT acts as intermediary 2.0% 2.2% � Reduction of FX reserve requirement 1.0% Consumer Loans from 11% to 9% resulting in an additional 0.0% c-07 n-08 r-08 n-08 l-08 g-08 p-08 t-08 v-08 c-08 b-08 r-08 y-08 foreign currency liquidity of ~ USD 2.5 bln g y y Dec Jan Feb Mar May Jun Aug Sep Nov Dec Ju Oc Ap Source: Weekly BRSA data as of 26 December. 7 * As of October 2008 ** Deposit banks

Profitability of the banking sector impacted by the negative developments in the second half of 2008 but still sound with ROAE at 18% ROAE at 18% Current Macro and Sector Outlook 2007 2008 Banking Sector Jan-Oct Jan-Oct % chg (mln YTL) � Banking sector revenue growth Total Revenues 32,662 36,720 12% of 12% y/y; driven by 21% y/y Net Interest Income 20,515 24,804 21% growth in net interest income Non-Interest Income 12,147 11,917 -2% and 24% y/y growth in fee o/w Fees & Comm. 6,417 7,988 24% income . Non-interest income o/w Other 5,730 3,929 -31% negatively impacted by FX g y p y Operating Costs 14,552 18,011 24% losses as a result of exchange HR costs 6,189 7,657 24% rate volatility in 4Q08 Non-HR costs 8,363 10,354 24% � Operating costs up 24% y/y, Operating Income 18,110 18,709 3% driven by branch network driven by branch network Provisions 2,509 4,540 81% expansions throughout the year Pre-tax Income 15,601 14,169 -9% and inflationary pressure in 1H08 Tax 2,693 2,771 3% � Provisions up 81% on the back of Net Income 12,908 , 11,398 , -12% asset quality deterioration Sector Return on Average Equity (%) accelerating from 2H08 onwards 26% � Net income down by 12% y/y 22% � ROAE at 18.1% as of Oct’08 ROAE t 18 1% f O t’08 18.1% 18% despite downward trend starting from 2H08 14% 10% 10% Dec-07 Feb-08 Apr-08 Jun-08 Aug-08 Oct-08 8

AGENDA � Current macro and sector outlook � Current macro and sector outlook � Summary 9M08 results* and latest developments � 2008YE preliminary highlights & 2009 outlook � 2008YE preliminary highlights & 2009 outlook (*) BRSA Consolidated 9

Key performance indicators Summary 9M08 results (BRSA Consolidated) Consolidated Net Income Consolidated ROE (*) (mln YTL) 1,102 32.0% 28.5% (2) (2) 1,077 2.8 pp 31.3% 49% 725 ( ) (1) 9M07 9M07 9M08 9M08 9M07 9M08 Consolidated ROA (**) Cost / Income 57.2% 2.24% 50.5% (3) 5.8 pp 56.4% (2) 50.6% (2) 2.19% 2.19% 0.10 pp 0 10 pp 2.09% 9M07 9M07 9M08 9M08 9M07 9M07 9M08 9M08 (*) Calculations based on beginning of the year equity. Annualized (**) Calculations based on net income/end of period total assets. Annualized 10 (1) Calculations based on restated equity and net income; ROE as of 9M07 was 28.7% based on reported equity and net income (2) Normalized to exclude the one-off effects of pension fund provisions on costs, general provision release on revenues and tax settlement expense on tax provisions in 1Q08. Also normalized to exclude one-off tax risk provision in 2Q08 (3) Normalized to exclude the gross-up effect of Superonline write-off on revenues and provisions in 2Q07

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries