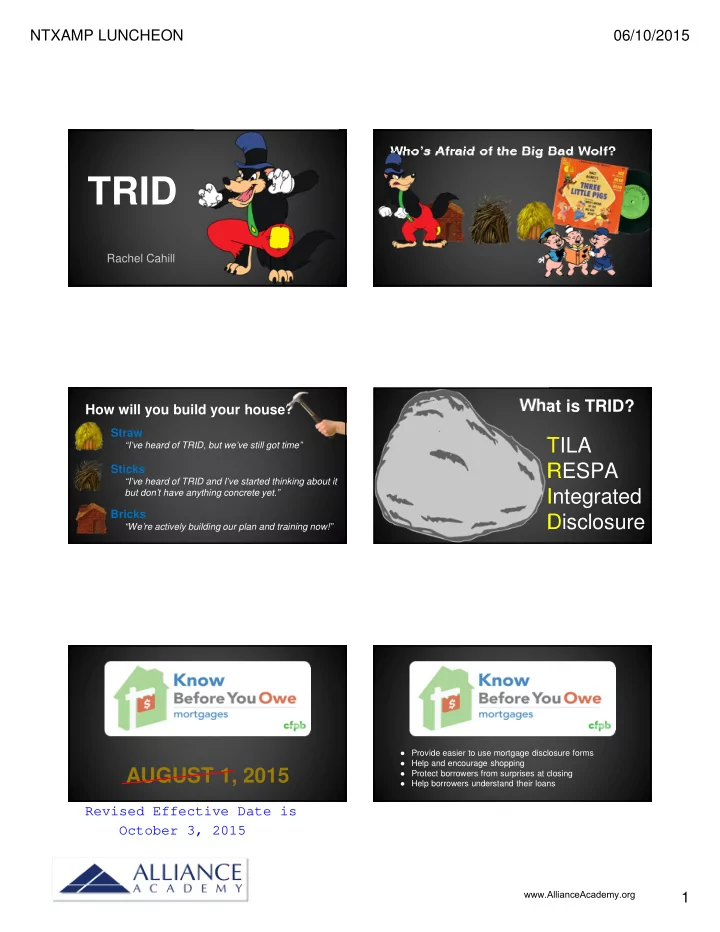

NTXAMP LUNCHEON 06/10/2015 Who’s Afraid of the Big Bad Wolf? TRID Rachel Cahill What is TRID? How will you build your house? Straw TILA “I’ve heard of TRID, but we’ve still got time” RESPA Sticks “I’ve heard of TRID and I’ve started thinking about it Integrated but don’t have anything concrete yet.” Bricks Disclosure “We’re actively building our plan and training now!” ● Provide easier to use mortgage disclosure forms ● Help and encourage shopping AUGUST 1, 2015 ● Protect borrowers from surprises at closing ● Help borrowers understand their loans Revised Effective Date is October 3, 2015 www.AllianceAcademy.org 1

NTXAMP LUNCHEON 06/10/2015 Will TRID impact MY business? Will TRID impact MY business? EVERYONE (Lenders, Real Estate, & Title) ORIGINATORS ● New loan app def = no required docs before LE ● Managing different forms for applications before & after Oct 3 ● No collection of payments or methods until Intent to effective Date of Aug 1 ● Effect of LE & CD delivery dates on contract deadlines Proceed ● Need more accurate data for estimates of taxes, ins, etc. ● HUD Line numbers removed ● Charge rate lock extension fees? Maybe…. ● Contact information needed for CD ● New booklet “Your Home Loan Toolkit” ● Multiple copies of disclosures to borrower ● Creditor prepares CD instead of Title JUNE 3: CFPB FINALLY AGREES TO SOFTER Coverage ENFORCEMENT IF WORKING IN “GOOD FAITH” TO COMPLY WITH THE TRID RULE Does NOT Apply To: Loan Types Affected: ● Reverse mortgages Closed-end consumer mortgages secured by real property, ● HELOCs including: ● Chattel-dwelling loans ● 1-4 Family residential ● Creditors that make 5 or fewer ● 25-Acre loans mortgage loans per year ● Vacant land loans ● Jr liens for housing assistance Keep in mind... this is a very soft “understanding” from Cordray loans to low/moderate income and is NOT a “hold harmless” period. consumers, or energy efficient Recommended Reading What is changing? ● Definition “Loan App” Full Final Rule plus Staff interpretations ● New Forms Only 1,888 pgs of “light reading” in legal terminology ● Timing & Processes CFPB “Small Entity Compliance Guide” ● Variances (fka tolerance) CFPB “Guide to Forms” CFPB “Readiness Guide” http://goo.gl/vooCde www.AllianceAcademy.org 2

NTXAMP LUNCHEON 06/10/2015 New strict definition of “Loan App” A ddress of subject property 1. New Definition of Loan L oan Amount requested 2. I ncome of the consumer 3. Application E stimated value of the property 4. N ame of the consumer 5. S ocial Security number to obtain credit report 6. 7. Any other info needed to qualify Tighter RESPA Triggers for 3 Day Disclosures “Pre-TRID” 3 Day Disclosures New Forms Early TIL Initial GFE “Pre-TRID” Disclosures for Closing New “Loan Estimate” LE Replaces GFE & early TIL Final TIL Includes new terminology required under Dodd-Frank Covers key features, costs, cash to close and risks HUD-1 Clearer breakdown of costs than lump-sum GFE blocks www.AllianceAcademy.org 3

NTXAMP LUNCHEON 06/10/2015 CD New “Closing Disclosure” How do I know which form to use? Replaces HUD-1 & Final TIL Oct 2 Applications taken on or BEFORE July 31, 2015 3 Days to Review ● Use the GFE, TIL and HUD-1 all the way through. (Do not switch or combine!) Easier for consumers to locate key information Oct 3 Applications taken on or AFTER August 1, 2015 ● Closely lines up with LE ● Use the LE and CD all the way through ● Interest rate & pmts ● Closing Costs broken down ● Loan affordability & cost of loan over time Timing Changes New Timing TILA-RESPA merge means TWO definitions of “business day” for timing requirements Requirements General: Days when the creditor’s offices are open to the public doing most normal business functions (Company Calendar) Specific: All calendar days except Sundays & legal public holidays (when the mail runs) Loan Estimate Timing Mailbox Rule & Received Dates Mailbox rule didn’t go away Initial LE: Considered “received” on 3rd ● Provided or placed in mail no later than 3 general specific day after mailing business days from app date Email considered “mail” so apply ● Provided or placed in the mail no less than 7 specific mailbox rule, unless there is proof of business days prior to closing (same 7 day waiting period) receipt www.AllianceAcademy.org 4

NTXAMP LUNCHEON 06/10/2015 Loan Estimate Intent to Proceed Loan Estimate Timing MUST receive “Intent to Proceed” from Revised LEs: at least one borrower before collecting ● Must be sent within 3 general days of Rate Lock or COC any fees other than a credit report fee. ● Signature on Loan Estimate is not I2P ● STILL must have valid Change of Circumstance ● Silence from borrower is not I2P ● Last version RECEIVED by the consumer no less than 4 ● Cannot collect even payment method specific business days prior to closing (mailbox rule) before I2P (ex credit card for appraisal) ● Cannot be sent out after Closing Disclosure is issued Closing Disclosure Timing Closing Disclosure Timing Revised CDs : ● May be delivered at or before closing Pre-Close CD: ● If certain changes are made, 3-day wait might start again ● Must be RECEIVED by the consumer no less than 3 (mailbox rule applies) specific business days prior to closing (mailbox rule applies) ● Limits on Closing Cost Increases (nearly identical to current Closing CD : RESPA tolerances) ● Delivered and signed at closing Closing Disclosure Changes New Processes Changes trigger another 3 business-day wait • APR increase or decrease more than 0.125% (or 0.25% for loans with irregular payments or periods) • Loan Product change • Prepayment penalty added • Less-significant changes disclosed on updated CD without additional 3-day waiting period www.AllianceAcademy.org 5

NTXAMP LUNCHEON 06/10/2015 Ready to leave a “TIP”? Preparing the CD “Total Interest Percentage” ● “Represents the total amount of interest that you will pay over the loan term as a percentage of your loan amount” ● Most creditors are going to prepare and provide the CD ● Loan Amount $100,000 with total amt of interest paid over the loan ● Creditor is accountable for the on-time delivery of an accurate term of $50,000, then the TIP would be 50% ($50,000÷$100,000) CD to consumer ● Industry Feedback ○ “TIP information is completely unnecessary and will prove very confusing for ● Creditor and Settlement Agent need to collaborate to complete consumers” ○ “Consumers will simply not understand that this rate is unrelated to the interest and deliver the CD rate and APR” ○ “Alarm consumers when they see how high these are, especially if they believe there is some connection to the other rates listed” ● Settlement Agent is responsible for delivering a CD to seller ZERO Tolerance → “Variations” Variances These fees may NOT increase: ● Fees paid to the creditor or mortgage brokers ● Affiliates of creditor or broker (previously in the 10% category) ● Unaffiliated 3 rd party if creditor did not allow consumer to shop for service provider (previously in the 10% category) 10% Tolerance → “Variations” ZERO Tolerance → “Variations” Some fees may exceed disclosed by aggregate of 10%: These fees may NOT increase: (continued) ● Unaffiliated 3 rd party if creditor permits consumer to shop and ● Transfer taxes consumer selects a provider from the Written Service Provider ● Lender credits may not DECREASE List disclosure or does not choose a provider at all ● Recording fees www.AllianceAcademy.org 6

NTXAMP LUNCHEON 06/10/2015 No Variation Test IMPACT Charges can exceed initial amounts disclosed on LE (if they were consistent with best & most reasonable info available at the time of disclosure): ● Prepaid interest ● Property insurance premiums ● Amounts placed into escrow account ● Charges paid to 3 rd party providers not included on creditor’s provided list or not required by creditor Who will prepare the CD? Will TRID impact MY business? • Which loan forms to use before & after Aug 1? Preparation of CD • New loan app def = no required docs before LE • No fees or payment methods before LE issued Delivery of CD to borrower • Need more accurate estimates of taxes, ins, etc. • New booklet “Your Home Loan Toolkit” Delivery of CD to seller • Impact of LE & CD delivery on contract deadlines • Contact information needed for CD Why? Lender is held responsible for accuracy • Multiple copies of disclosures to borrower of costs and delivery to borrower • Creditor prepares CD instead of Title What can I do NOW to prepare? ● Start using new 6 data point app definition ● Communicate with partners about how to make the transition easier (collaborate!) ● BE HONEST and UPFRONT about delays!!!!! ● Parties work together as a TEAM!!!! ● Read the guides ● TRAINING TRAINING TRAINING TRAINING www.AllianceAcademy.org 7

NTXAMP LUNCHEON 06/10/2015 How will you build your house? www.AllianceAcademy.org 8

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries