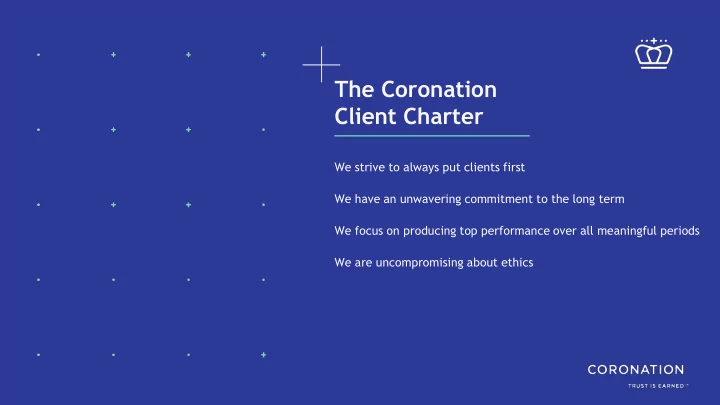

The Coronation Client Charter We strive to always put clients first We have an unwavering commitment to the long term We focus on producing top performance over all meaningful periods We are uncompromising about ethics

Financial planning challenges in 2019 Peter Kempen March 2019 A presentation prepared for the Allan Gray Fund Provider roadshow

FINANCIAL PLANNING CHALLENGES Regulatory environment Disappointing returns Growth-asset dilemma Discretionary savers Retirement crunch Looking forward

How was your year? 5

Regulatory environment in 2019

So, what’s changed in your business? SELECTED REGULATORY INTERVENTIONS, 2001-2019 2001 CGT introduced in SA 2002 CISCA More powers to the FSB to make rules FAIS Fit & proper, compliance, exams , ombud 2003 TER Total expense ratio disclosure introduced 2004 Retirement reform DP Reduce costs, increase access FSC Voluntary empowerment framework agreed 2005 FAIS New rules for compliance & auditor reporting to FSB 2006 FAIS Fit & Proper requirements tightened up 2007 Retirement fund reform NSSF formally on the agenda 2008 GFC Global Financial Crisis leads to step-change in regulatory intent 2009 FAIS PI cover requirements tightened up FAIS Capital adequacy rules expanded 2010 Reg 28 overhauled; requires member-level compliance Retirement fund reform Industry consolidation process starts 2011 Red Book Initiative New regulatory framework proposed Living annuities Disclosure campaign to make DDs more sustainable CISCA First regulations for white-labelled funds 2012 Retirement fund reform NSSF DP published Retirement fund reform Phasing out of provident funds proposed 2013 Retirement fund reform 4x detailed Treasury DPs BBBEE Act adopted: Generic codes now binding DWT Introduction of divdend withholding tax announced 2014 Retail Distribution Review First DP published Retirement fund reform Cap on contr. deduction introduced TCF DP launched introducing outcomes principles 2015 TFSA/TFI New tax-free savings vehicle introduced Retirement fund reform Phasing out of provident funds postponed CISCA Hedge funds declared CIS 2016 Retirement fund reform 2012 NSSF DP issued 2nd time Retirement fund reform Phasing out of provident funds postponed EAC Industry-wide standardised total cost of ownership disclosure 2017 Parliamentary hearings on transformation Retirement fund reform Phasing out of provident funds postponed FAIS New Fit & Proper Rules FSC Revised BEE code adopted 2018 FSR Sets framework for FSCA & PA Retirement fund reform Phasing out of provident funds postponed FAIS New General Code of Conduct 2019 Retirement fund defaults Effective March 2019 COFI Draft bill circulated for comment RDR Awaiting DP on categorisation of advisers, investment issues 7

Retirement fund defaults Still in consultation as at 1 March 2019 – Member guidance • Tell members what their options & trade-offs are before they access their retirement capital • Likely written / web-based communication as the most typical option – Trustee-endorsed opt-in annuity strategy • FSCA Conduct Standard for Living Annuities • Requirements: Suitable, reasonable cost Prescribed, age-related drawdown rates • Member opts out by • • Transferring • Choosing own drawdown or assets Likelihood is that most trustees will implement • conservatively 8

Source of current financial planning anxiety

Annus horribilis 2018 was the worst year on record – even worse than 1920 63 of 70 assets globally ended with negative dollar returns Only 7 assets with positive returns Percentage of assets with a negative return in US dollar terms – T-Bills – China, US, Korea, Japan and Thailand bonds – Wheat (only commodity) Not a single equity market had a positive return Source: Deutsche Bank (end 2018) 10

Negative returns were broad-based Only resources provided any reprieve -16% Naspers Ltd 28% BHP Group PLC -15% Compagnie Financiere Richemont 32% Anglo American Plc 2% Sasol Ltd -4% Standard Bank of SA Ltd 2% Firstrand Limited -31% MTN Group Ltd 3% Mondi -5% Sanlam -40% British American Tobacco Plc -5% Absa Group Ltd 13% Nedbank Group Ltd -15% Remgro Ltd -12% Shoprite Holdings Ltd -10% BID CORP LTD -3% Vodacom Group 42% ANGLOGOLD ASHANTI HOLDINGS -3% Bidvest Group Ltd -9% Growthpoint Properties Ltd 4% Mr Price Group Ltd 4% Capitec Bank Holdings Ltd 4% RMB Holdings Ltd -13% Discovery Holdings Ltd -12% Woolworths Holdings Ltd -7% Investec Plc -1% Redefine Income Fund -50% Aspen Phamacare Holdings Ltd 8% Clicks Group Ltd -6% Sappi Ltd -39% Tiger Brands Ltd 6% Spar Group Ltd -8% PSG Group -7% Gold Fields Limited 9% Netcare Ltd -44% NEPI Rockcastle PLC -12% The Foschini Group Ltd -2% Truworths International Ltd 0% Life Healthcare Group Holdings 0% Exxaro Resources Ltd -2% AVI Limited -35% Fortress REIT Ltd 55% Anglo American Platinum Ltd -19% Reinet Investments Sca -18% RMI Holdings -13% Glencore Xstrata Plc 13% Impala Platinum Holdings Ltd -26% Barloworld Ltd -7% Investec Ltd 0% Pick N Pay Stores / Holdings -60% -40% -20% 0% 20% 40% 60% 80% Top 50 11 Source: Bloomberg (end 2018)

Coming after a miserable few years There’s just no sugar - coating it… 2018 was preceded by several mediocre years – 5-year real returns are now c.0% for both SA equity & property – If the JSE flat-lines to June 2019 - then 5-year nominal equity returns will be zero -5% p.a. (-23% cumulative) in real terms • Life has been really tough for clients – Day-to-day life in SA not easy Ramaphoria evaporated as realities of SA challenges exposed through the year • • Land debate creating anxiety over property rights • Emigration quoted as reason for selling your home rose threefold to 9% (from five years ago) – Unlike previous tough cycles the rand didn’t weaken enough to insulate rand returns Ugly combination of low investment returns & stubborn inflation (negative jaws) • • Resulting in ever-rising draw-down rates for living annuities as markets go nowhere 12

We are on the verge of making history We are 6 months away from testing zero… BEAR MARKET OF THE 70s WEAK MARKET OF EARLY 90s PRE DOMESTIC DEMOCRACY FINANCIAL CRISIS EM CRISIS RECESSION Rolling 5 year SA equity returns 13

Savings industry under stress We can all take a challenging year or two But 5 tough years is historically rare and has put our industry into stress Clients are losing faith in – The growth asset classes (equity & property) – Active management – South African assets – Market-linked living annuities We get it 14

Growth asset dilemma

An inverted risk curve The recent past vs the LT history 14% 14% 14% 12% 12% 12% Balanced Defensive Balanced Plus Capital Plus Coronation Strategic Income Strategic Income 10% 10% 10% Strategic Income 8% 8% 8% Coronation Balanced Defensive Coronation Strategic Income Coronation Strategic Income Balanced Defensive A 6% 6% 6% Strategic Income Coronation Capital Plus Capital Plus 2018 2018 2018 4% 4% 4% 2016 2016 2016 Coronation Balanced Defensive Coronation Balanced Defensive Balanced Plus Coronation Balanced Plus 2% 2% 2% A A 10 Year 10 Year 10 Year Balanced Defensive 0% 0% 0% 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% Coronation Capital Plus Coronation Capital Plus Capital Plus -2% -2% -2% -4% -4% -4% Coronation Balanced Plus Coronation Balanced Plus INDUSTRY SWITCHING DOWN THE RISK CURVE Balanced Plus -6% -6% -6% -8% -8% -8% 16

And flows continue to track ST performance Last 10 year returns vs flows in Balanced Plus 40% R2,000 Millions A sure way to erode 30% wealth over time R1,500 20% R1,000 10% R500 0% R0 -10% -R500 -20% -R1,000 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Total Net Flows (RHS) Balanced Plus rolling 12-month return 17 As at 31 January 2019. Source: Morningstar

Meeting financial planning assumptions Coronation Balanced Plus to 31 December 2018 16% 45% of the time Avg fund: 27% of the time 14% 75% of the time Avg fund: 57% 12% 10% 8% 6% 4% 2% 0% 2014 2013 2012 2011 2010 2009 Actual return Required return to make 10 year assumption Required return to make 20 year assumption Source: Morningstar, Coronation research as at 31 December 2018 18

Coronation Balanced Plus – absolute terms # of # of Subsequent Subsequent Subsequent Subsequent Subsequent Subsequent Start Start End End drawdown drawdown Months Months 1 year 1 year 3 years (p.a) 3 years 5 years (p.a) 5 years Largest Largest May 1998 May 1998 Aug 1998 Aug 1998 4 4 -34,3% -34,3% 29,1% 29,1% 19,1% 68,9% 94,4% 14,2% drawdown drawdown 2 nd largest 2 nd largest Nov 2007 Nov 2007 Feb 2009 Feb 2009 16 16 -16,8% -16,8% 34,7% 34,7% 19,8% 71,8% 154,5% 20,5% drawdown drawdown 3 rd largest 3 rd largest June 2002 June 2002 March 2003 March 2003 10 10 -12,2% -12,2% 35,7% 35,7% 156,5% 36,9% 246,1% 28,2% drawdown drawdown 4 th largest 4 th largest Feb 2000 Feb 2000 May 2000 May 2000 4 4 -8,8% -8,8% 24,9% 24,9% 10,5% 34,8% 132,9% 18,4% drawdown drawdown 5 th largest 5 th largest Sep 2018 Sep 2018 Dec 2018 Dec 2018 4 4 -7,8% -7,8% drawdown drawdown Average Average 11 11 -16,0% -16,0% 24,9% 24,9% 66,4% 21,6% 125,6% 20,3% Source: Morningstar, Coronation Research 19

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries