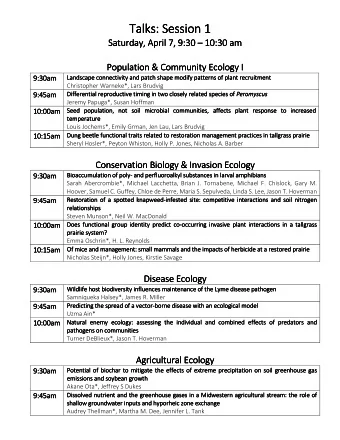

SESSION B SUPPLIES TO MULTIPLE LOCATION ENTITIES ALLOCATION METHODS - PowerPoint PPT Presentation

SESSION B SUPPLIES TO MULTIPLE LOCATION ENTITIES ALLOCATION METHODS A BUSINESS PERSPECTIVE CHIU MING MAN, BARCLAYS 17-18 April 2014 Tokyo, Japan Definition of MLE Branches A legal entity that has establishments (fixed place of

SESSION B SUPPLIES TO MULTIPLE LOCATION ENTITIES ALLOCATION METHODS A BUSINESS PERSPECTIVE CHIU MING MAN, BARCLAYS 17-18 April 2014 Tokyo, Japan

Definition of MLE • – Branches – A legal entity that has establishments (fixed place of business with a sufficient level of infrastructure in terms of people, systems and assets to be able to receive and/or make supplies) in more than one jurisdiction – Each establishment is legally inseparable from the other – Not subsidiaries or ‘related’ parties which only have a single fixed places of business in one location but may be registered for VAT in multiple locations (these should be treated as SLEs) • Use of MLEs – Regulatory passporting – Free flow of intra-group capital and liquidity resulting in lower costs of doing business – Integrated organisation and risk management – Increased ability to withstand idiosyncratic adverse shocks – Economies of scale 2

• MLE Business models (for procurement of services) – Administrative centres • MLE HQ facilitates the procurement of services from S but each MLE branch uses and pays for its share directly (global framework agreements) • MLE HQ facilitates the procurement and payment of services from S and recharges the cost to each MLE branch that uses the service (global contracts) – Service provider (e.g. IT development, centralised support functions) • MLE HQ acquires services from S and consumes this as cost component of a separate supply between MLE HQ and each MLE branch (sub contracting) – Alternative billing models (cost+ vs rate card) 3

• Practical implications – Direct use Can be effective where MLE HQ simply acts as an administrative centre only and services are used and are paid for directly by each MLE branch Supplier would need to ‘second guess’ which MLE is using the service For customer, often impossible to determine location of use at the point of invoice/payment where there is direct use but not direct payment (particularly in MLEs that operate centralised accounts payable functions which are segregated from the procurement functions) rendering it impossible to apply reverse charge correctly 4

• Practical implications – Direct delivery Simple to apply in practice as VAT jurisdiction follows business agreement Consistent with main rule for SLE where MLE HQ operates a service provider model (but note, MLE HQ may not always be the service provider and buyer of services from S) Inconsistent with destination principle when applied to ‘multiple - use’ scenarios (global contracts utilised by more than one establishment of a MLE), or contracts where the customer of S is not MLE HQ 5

• Practical implications – Recharge Method Effective where services are acquired and paid for centrally to realise economies of scale ( cf. Direct use method) Builds on existing data/processes (e.g. accounting, TP recharge data), simplifying compliance and audit burden [note: requires acceptance of “fair and reasonable” allocations or apportionment methodologies] Difficulties in linking price of initial supply and the amount of recharge, particularly in circumstances where costs are recharged on a ‘pooled’ basis or where MLE HQ is a service provider Lack of clarity regarding internally generated services which may include elements of externally acquired services (either in unaltered or altered form) Challenges in applying time of supply rules in a consistent and coherent manner 6

• Business imperatives – Need for consistency/clarity of treatment – hybrid approach represents the worst case scenario for business to administer • Compliance certainty • Systems alignment for compliance • Documentation/data requirements to support tax audits – Fundamental question of actual supply vs. deeming provisions taking into account current inconsistency of treatment of branch-branch supplies – Lack of clarity regarding some aspects of the approaches, in particular the Recharge Method (possibly as future OECD work?) – Notwithstanding this, tax authorities are encouraged to provide clear guidance of the various approaches 7

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.