Price control in vertical relations Patrick Rey Toulouse School of Economics and IDEI based on joint work with Thibaud Vergé (CREST-LEI, Paris) Pros and Cons of Vertical Restraints Stockholm, November 7 2008

Introduction Policy perspective: vertical restraints Hot debates in practice and in the IO literature Large divergence law/economics for price restrictions Research agenda: vertical /horizontal interaction Vertical coordination Rivalry between vertical structures Consumer goods: interlocking relationships 1

Resale Price Maintenance Various forms Imposed price Maximum price (price ceiling) Minimum price (price floor) Recommended, advertised prices Specific product markets Drugs Books, newspapers 2

Competition Law Price restrictions are “bad” RPM (price floors) is illegal per se in the EU (out of a blacklist of two) Non-price restrictions are more tolerated (rule of reason) Caveats US policy over time 1911: price floors are per se illegal (Dr Miles) 1968 : price ceilings are per se illegal (Albrecht) 1997: rule of reason for price ceilings (State Oil) 2007: rule or reason for price floors as well (Leegin) France “Loi Lang” : RPM mandatory for books and press “Loi Galland” : RPM de facto for supermarkets 3

Economics Academic literature: not so clear-cut (OECD report on Franchising, EC Green paper, Rey-Vergé 2008) Intrabrand coordination Price and non-price restraints can have similar effects Interbrand competition Not necessarily favourable to non-price restrictions 4

Economics Intrabrand competition Free-riding on retail services (Telser JLE 1960), quality certification (Marvel-McCafferty Rand 1984) → welfare effect ambiguous/positive (Comanor-Frech AER 1985, Caillaud-Rey 1987) similar for price and non-price restrictions Producer’s opportunism (Hart-Tirole Brookings 1990) O’Brien -Shaffer Rand 1992 Rey-Vergé Rand 2004 → welfare effect negative similar for price and non-price restrictions 5

Economics Interbrand competition Competition-dampening: strategic delegation, not RPM Rey-Stiglitz EER 1988, Rand 1995 (Bonanno-Vickers JIE 1988) Gal-Or EER 1991 Caillaud-Rey EER 1995 Foreclosure: tying/exclusive dealing, not RPM Tacit Collusion (Jullien-Rey 2000) Here: interlocking relationships (joint with Thibaud Vergé) RPM eliminates both intrabrand and interbrand competition Territorial restrictions would not achieve the same outcome 6

Interlocking relationships Market structure 2 (differentiated) manufacturers A and B , constant marginal cost c 2 (differentiated) retailers 1 and 2 , constant marginal cost (=0) demand pattern for 4 “products” (monopoly prices p M , profit Π M ) Manufacturer A Manufacturer B B-1 A-2 A-1 B-2 Retailer 1 Retailer 2 7 Consumers

Interlocking relationships Competition game Upstream competition manufacturers offer two-part tariffs, with or w/o RPM retailers (observe all tariffs) and accept / reject Downstream competition: retailers set retail prices Note: Dobson and Waterson (2007) on linear tariffs Retail market power No retail bottleneck Potential competition at each retail location: selection process (BW 1985) Bypass: manufacturers set-up own their own outlets or sell directly Retail bottlenecks: a single retailer at each retail location (confer rents) 8

No retail bottleneck (and no RPM) Interbrand competition, then intrabrand competition → retail prices are (somewhat) competitive ( p c < p M ) Intuition Manufacturers recover retail margins through fixed fees Internalize impact of (retail) prices on the entire margin on sales of own brand the retail margin on sales of rival brand → for A: max Σ j=1,2 (p Aj - c)D Aj (p) + (p Bj - w Bj )D Bj (p) – F Bj 9

No retail bottleneck Manufacturer A Manufacturer B Retailer 1 Retailer 2 Consumers 10

No retail bottleneck Intuition (cont’d) Retail prices are driven by wholesale (marginal) prices Maintaining high retail prices requires high wholesale prices Positive upstream margins Free-riding on rival manufacturer’s upstream margin 11

Resale Price Maintenance Retail prices are directly set by manufacturers Recover as before retail margins through franchise fees → internalize as before the impact of (retail) prices on the entire margin on sales of own brand the retail margin on sales of rival brand No need anymore to use wholesale prices to maintain retail prices squeezing upstream margins yields monopoly outcome w ij = c → each manufacturer residual claimant on all margins → set retail prices at the monopoly level ( p = p M ) 12

Resale Price Maintenance Continuum of equilibria For any given wholesale prices, there exists an equilibrium given p , A and 1 can share profits through either w A1 or F A1 → A and 1 are thus indifferent about w A1 but w A1 affects A ’s dealing with 2 , and 1 ’s dealing with B Eq. wholesale and retail prices are negatively correlated w ↗ → p ↘ free-riding on rival ’ s upstream margin Only one equilibrium robust to (even small) retail effort retailers as residual claimant wholesale prices at cost, retail prices at monopoly level 13

Retail bottlenecks Retailers earn positive rents (p A1 - w A1 )D A1 – F A1 + (p B1 - w B1 )D B1 – F B1 ≥ (p B1 - w B1 ) Ď B1 – F B1 → (p A1 - w A1 )D A1 – F A1 ≥ (p B1 – w B1 )[ Ď B1 – D B1 ] > 0 → max Σ j=1,2 (p Aj - c)D Aj + (p Bj - w Bj )[D Bj – Ď Bj ] Retailers indifferent wrt dealing with both or only one → manufacturers can easily deviate to exclusive dealing Questions is “ double common” agency still an equilibrium? best equilibrium? (industry profits / manufacturers’ profits) 14

Retail bottlenecks Standard linear demand D ij = 1 - p ij + α p hj + β p ik + αβ p hk ( α + β + αβ < 1) Two-part tariffs Double agency may cease to be an equilibrium This happens for “low degrees” of substitutability (low β ) 15

Retail bottlenecks RPM For ranges of parameters continuum of double agency equilibria including monopoly pricing ( p = p M for some w < c ) As w ↗ , p and retailers’ profits ↘ , manufacturers ’ profits ↗ manufacturers prefer lowest retail prices retailers prefer highest retail prices (even above p M ) 16

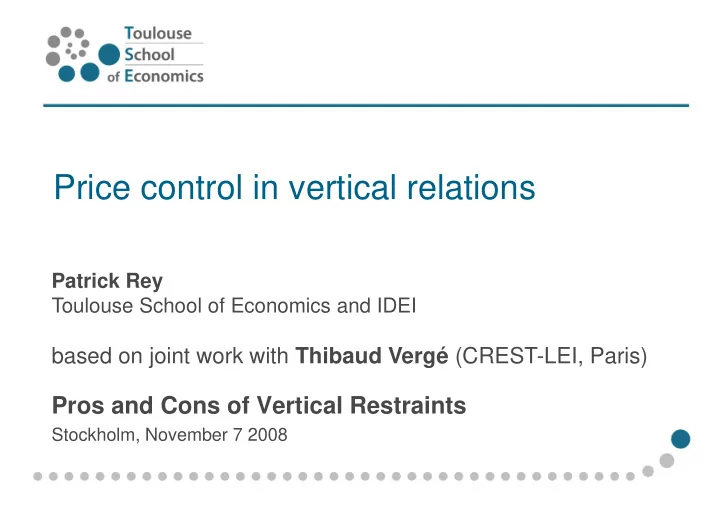

Retail bottlenecks 1 No Double Common Agency Equilibrium with Two-Part Tariffs Equilibrium with RPM and 0 . 8 Monopoly Prices 0 . 6 0 . 4 0 . 2 0 . 2 0 . 4 0 . 6 0 . 8 1 17

Illustration: France Current debate 1996 Laws (Galland, Raffarin) Merger wave (5 large retailers) Carrefour, Auchan, Casino; Leclerc, Intermarché Price evolution (Germany/France) Proposed reform Canivet commission Dutreil and Chatel laws 18

Illustration: France Empirical evidence France – Germany: branded products in supermarkets Biscourp, Boutin and Vergé: market concentration and prices Bonnet-Dubois-Simioni 2004 French market for bottled water Structural econometric model – Berry-Levinson-Pakes Eca 1995 – Berto Villas-Boas 2004 Linear prices / two-part tariffs / RPM → best fit: two-part tariff + RPM, monopoly prices 19

Research agenda Inexistence of (double) common agency eq. Source of the problem one side (the manufacturers) has “all” the bargaining power by construction, in equilibrium the other side (retailers) is indifferent between accepting all / rejecting some offers generates many different types of deviation, difficult to rule all of them out Possible solutions More balanced bargaining power – “Nash - bargaining” / cooperative game theory approaches – Non-cooperative approaches: Stole-Zwiebel ( RES 1996), … Secret / public offer and acceptance decisions Reacting to rejections – Small vs. drastic changes / dynamics – renegotiation / contingent offers 20

Research agenda Illustrations De Fontenay – Gans ( Rand forth, 2005) secret contracts / observable acceptance-rejection decisions contingent offers or renegotiation in case of rejection → no exclusion, no complete coordination Rey – Vergé – Thal (work in progress) public contracts, offers contingent on market structure → integrated monopoly outcome Questions Minimal flexibility needed for monopoly outcome / no exclusion ? Role of contingent offers? → go back to “simpler” market structures 21

Interbrand competition (common agency) 2 manufacturers, 1 retailer → monopoly prices A B (Bernheim-Whinston 1986) Intuition Each manufacturer sells “at cost” → retailer becomes residual claimant R → sets retail prices at appropriate monopoly level Manufacturers retrieve (part of) the profits e.g. through franchise fees Remarks Consumers Does not depend on bargaining power no need for contract observability 22

Intrabrand competition 1 manufacturer, 2 retailers If bargaining power is upstream: monopoly M outcome Wholesale prices above marginal cost (maintain high retail prices despite intrabrand competition) 1 2 Fixed fees to recover retail profits Remark: Observability of wholesale contracts Hart-Tirole Brookings 1990, O’Brien -Shaffer Rand 1992, Consumers McAfee-Schwartz AER 1994, Rey-Vergé Rand 2004 23

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries

![Annual House Price Changes (New & Resale) 2014 Price Growth (Actual), 2015 Forecasts [New]](https://c.sambuz.com/440329/annual-house-price-changes-new-resale-2014-price-growth-s.webp)