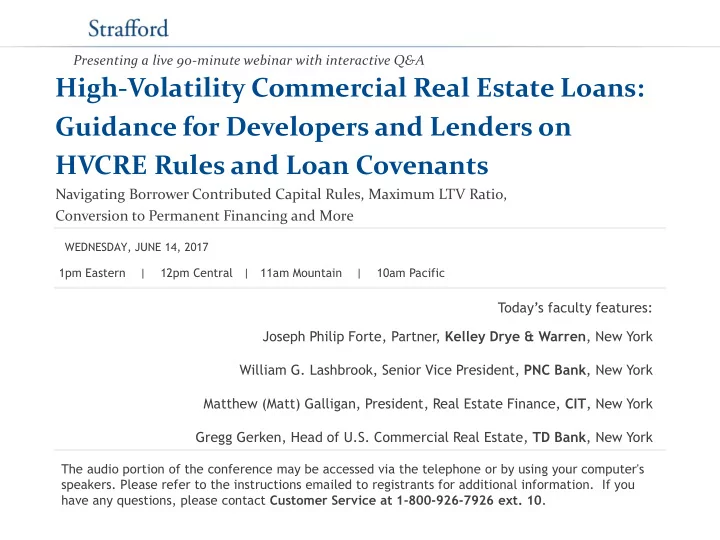

Presenting a live 90-minute webinar with interactive Q&A High-Volatility Commercial Real Estate Loans: Guidance for Developers and Lenders on HVCRE Rules and Loan Covenants Navigating Borrower Contributed Capital Rules, Maximum LTV Ratio, Conversion to Permanent Financing and More WEDNESDAY, JUNE 14, 2017 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific Today’s faculty features: Joseph Philip Forte, Partner, Kelley Drye & Warren , New York William G. Lashbrook, Senior Vice President, PNC Bank , New York Matthew (Matt) Galligan, President, Real Estate Finance, CIT , New York Gregg Gerken, Head of U.S. Commercial Real Estate, TD Bank , New York The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10 .

Tips for Optimal Quality FOR LIVE EVENT ONLY Sound Quality If you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, you may listen via the phone: dial 1-866-873-1442 and enter your PIN when prompted. Otherwise, please send us a chat or e-mail sound@straffordpub.com immediately so we can address the problem. If you dialed in and have any difficulties during the call, press *0 for assistance. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

Continuing Education Credits FOR LIVE EVENT ONLY In order for us to process your continuing education credit, you must confirm your participation in this webinar by completing and submitting the Attendance Affirmation/Evaluation after the webinar. A link to the Attendance Affirmation/Evaluation will be in the thank you email that you will receive immediately following the program. For additional information about continuing education, call us at 1-800-926-7926 ext. 35.

Program Materials FOR LIVE EVENT ONLY If you have not printed the conference materials for this program, please complete the following steps: Click on the ^ symbol next to “Conference Materials” in the middle of the left - • hand column on your screen. • Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program. • Double click on the PDF and a separate page will open. Print the slides by clicking on the printer icon. •

HI HIGH GH-VOLA OLATIL TILITY ITY CO COMMERC ERCIAL IAL REAL AL EST STATE TE LO LOAN ANS: S: G U I D A N C E F O R D E V E L O P E R S A N D L E N D E R S O N H V C R E R U L E S A N D L O A N C O V E N A N T S S T R A F F O R D P U B L I C A T I O N S , I N C . W E B I N A R JUNE 14, 2017 MODERATOR SPEAKER Joseph Philip Forte Matthew (Matt) Galligan Kelley Drye & Warren CIT SPEAKER SPEAKER Gregg Gerken William G. Lashbrook TD Bank PNC Bank

BASEL ACCORD 1) Basel Committee on Banking Supervision (originally Committee on Banking Regulations and Supervisory Practices) formed in the early '70s. 2) G10 Central Bankers response to financial turmoil following US abandoning Gold Standard resulting in the failure of several major banks for foreign currency losses. 3) Principal focus is capital adequacy and its role in global banking system. 4) Since 1988 has issued 3 Capital Accords concerning minimum capital ratio to risk (Basel I), minimum capital reserves, supervisory review of adequacy and risk disclosure (Basel II 2004) and increased required capital, rated quality of capital, changed risk rating of assets and buffers and minimum liquidity (Basel III 2010). 6

US BASEL III 1) Pursuant to Dodd-Frank, Federal Reserve Board, Office of the Comptroller of the Currency and the Federal Deposit Insurance Corporation approved US Basel III for the banks regulated by them in July 2013. 2) Among its comprehensive revisions was the new category of High Volatility Commercial Real Estate Loans deemed to be riskier than other real estate loans. 3) All HVCRE loans are assigned a capital risk weighting of 150% (12% rather than 8%). 4) The HVCRE Rule went into effect on January 1, 2015 for all HVCRE loans 7

DEFINITION OF HVCRE 1) Any loan which is not a “permanent” loan and finances the acquisition, development and construction of real property (ADC) are HVCRE loans regardless of when made. 2) Limited regulatory exemptions from HVCRE. 3) Very vague and broad definition. 4) Loans prior to effective date are not grandfathered. 8

HVCRE EXEMPTIONS The following loans are expressly exempt from the HVCRE Rule: 1) One to four family residential properties. 2) Real estate that qualifies as "Investment in community development" or "qualified investment". 3) Agricultural land. 4) Commercial real estate (CRE) loans which meet regulatory exemption requirements. 9

HVCRE EXEMPT ADC LOAN 1) LTV ratio Is equal or less to bank regulator's supervisory LTV limit. 2) Borrower contributes capital in cash, unencumbered readily marketable assets or out of pocket expenses incurred and paid for by borrower equal to 15% of “as completed” value. 3) Borrower has contributed capital prior to lender's first advance, and 4) Such capital plus all internally generated capital must be contractually required to remain in project for the life of the project. 10

PROBLEM WITH THE RULE 1) The HVCRE rules are creating confusion and disproportionately affecting commercial real estate ADC loans by driving up borrowing costs and reducing credit availability. 2) The rules also appear to be contributing to the apparent slowdown in bank commercial real estate lending. 11

BANKS ATTEMPT TO OBTAIN GUIDANCE 1) Since January 2015, necessary clarification for key elements of the rule have not been provided by regulators despite ongoing requests. 2) Many banks, including small community financial institutions, have been deterred from making this type of loan, which can represent up to 50 percent of a small bank loan portfolio. 12

CONSEQUENCE OF NOT CLARIFYING THE RULE 1) Without modifications, the consequences of the HVCRE rule could have a deleterious economic impact on commercial real estate lending by U.S. banking organizations. 2) Without a response from the regulatory community, the proposed legislation is intended to address the problem. 13

CURRENT OUTSTANDING CRE DEBT 1) Of the $3.8 trillion in commercial real estate debt outstanding, commercial banks constitute our nation’s largest source of commercial real estate financing. 2) Approximately $1 billion a day is maturing though 2018 – including $411 billion in bank debt. 14

JUST A CRE OWNERS AND BANK LENDERS PROBLEM 1) Significant contribution that the commercial and multifamily real estate industry makes to the nation’s GDP. 2) Contributing to America’s gross domestic product, employing millions of people and producing a significant amount of the taxes raised by local governments for essential public services. 3) Without adequate credit capacity for this important sector, jobs and tax revenue will be lost. 15

BANK REGULATORS ATTEMPT TO CLARIFY THE RULE 1) HVCRE Frequently Asked Questions published by the agencies on March 31, 2015 (FAQs). 2) Unfortunately, the FAQs raised more issues than were resolved but answered questions that no one had asked. 3) Lack of clarity in the HVCRE rule has resulted in a wide disparity in how banks classify their ADC portfolios as HVCRE or non-HVCRE. 4) Results negatively impact ADC loan decisions for some banks, leaving some borrowers with fewer and potentially more costly sources of ADC loan capital. 5) A slowdown in ADC lending has the potential for broader economic impact. 16

BORROWER UNCERTAINTIES 1) Contributing additional capital to an existing HVCRE loan. 2) Grandfathering of existing ADC loans. 3) Cash contributed by second mortgage on property. 4) “As stabilized” value. 5) Land contributed to a new development. 6) Soft costs as contributed capital. 7) Subsequent appraisal/valuation resulting in LTV no longer exceeding maximum LTV ration. 8) Contributed capital remaining in the project. 9) Impact of mezzanine debt. 17

TYPICAL HVCRE LOAN COVENANTS 18

PURPOSE OF THE PROPOSED LEGISLATION 1) The proposed legislation addresses several specific deficiencies in the agencies’ regulations governing what is an HVCRE loan. 2) The legislation does not eliminate the agencies’ ability to require banks to hold higher capital for HVCRE loans. 3) The bill provides the clarity which the regulators have yet to provide, including which types of loans should not be classified as HVCRE loans. 19

PROPOSED LEGISLATION CLARIFIES THE RULE 1) Capital charge remains at 150 percent consistent with original risk regulatory agencies wanted to protect against under HVCRE rule 2) ADC loans made prior to January 2015 are grandfathered and do not have to satisfy current HVCRE exemption criteria 3) New exemption added to HVCRE rule covering acquisition/refinancing loans for performing income producing properties 4) Internally generated capital no longer required to remain in the project 20

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries