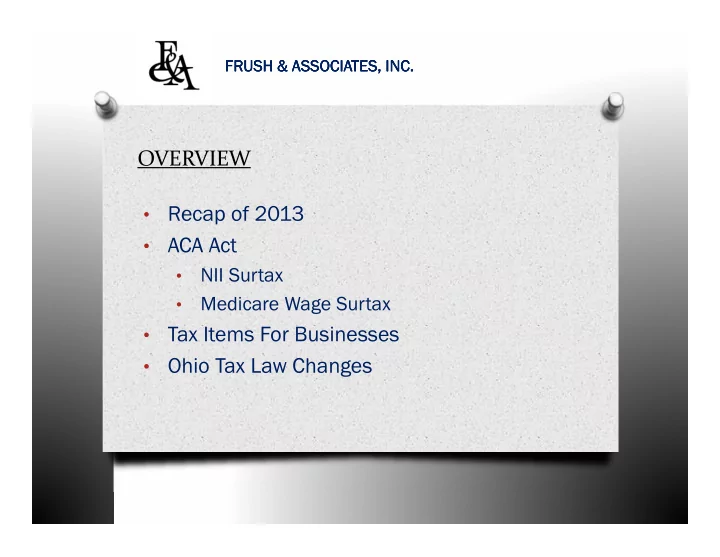

FRUSH & ASSOCIATES, INC. FRUSH & ASSOCIATES, INC. FRUSH & ASSOCIATES, INC. FRUSH & ASSOCIATES, INC. OVERVIEW Recap of 2013 • ACA Act • NII Surtax • Medicare Wage Surtax • Tax Items For Businesses • Ohio Tax Law Changes •

Circular 230 Disclosure Pursuant to the rules of professional conduct set forth in Circular 230, as promulgated by the United States Department of the Treasury, nothing contained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service, and it cannot be used by any taxpayer for such purpose. No one, without our express prior written permission, may use or refer to any tax advice in this communication in promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to any other party. For discussion purposes only. This work is intended to provide general information about the tax and other laws applicable to retirement benefits. The author, his firm or anyone forwarding or reproducing this work shall have neither liability nor responsibility to any person or entity with respect to any loss or damage caused, or alleged to be caused, directly or indirectly by the information contained in this work. This work does not represent tax, accounting, or legal advice. The individual taxpayer is advised to and should rely on their own advisors

Last Time We Met….. O The FISCAL CLIFF – included the potential onset of federal tax increases and spending cuts (scheduled to take effect January 1, 2013) that could have a substantial impact on the economy. O Was estimated up to 90% of Americans would have a tax increase.

Where We Were � Bush-era tax rates of 10%-35% � Dividends (qualified) taxed from 0%-15% � Long-term capital gains taxed from 0%-15% � Estate tax – higher exemption/ lower rate � No marriage penalty � Tax-advantaged depreciation options � Phase-outs and credits

Bush Tax Cuts Extended….With A Kicker 2012 Brackets 2012 Brackets 2012 Brackets 2012 Brackets 2013 Brackets 2013 Brackets 2013 Brackets 2013 Brackets 10% 10% 15% 15% 25% 25% 28% 28% 33% 33% 35% 35% 39.6%*

Dividends 2012 2012 2012 2012 2013 2013 2013 2013 Ordinary: Ordinary: Up to 35% Up to 39.6%* Qualified: Qualified: 0-15% Up to 20%*

Capital Gains 2012 2012 2012 2012 2013 2013 2013 2013 Short-Term: Short-Term: Up to 35% Up to 39.6%* Long-Term: Long-Term: 0-15% 0-20%*

ACA Tax Provisions * The Affordable Care Act of 2010 introduced tax provisions relating to health care, and also snuck in a couple new taxes

Schedule of New Health Care Provisions Year Provision 2013 • Flexible spending arrangement the maximum drops to $2,500 per plan year • New “HI” (hospital insurance tax) on high-income taxpayers • New 3.8% Medicare tax on investment income • Medical care itemized deduction threshold increases to 10% of AGI starting in 2013 (except from 2015–2016) 2014 • States will be required to provide federally approved insurance plans • Premium assistance credit • Excise tax on uninsured individuals Excise tax on applicable large employers (moved to 2015) • • Insurer reporting requirements • Eligible premiums included in cafeteria plans 2017 • Increase in medical deduction threshold for taxpayers age 65 and over 2018 • Excise tax on high-cost employer plans 9

ACA Tax Provisions � Beginning with 2012, employers are required to report the cost of coverage on the employee’s W-2, Box 12 (informational only) � Employer contribution continues to be not taxable to the employee � Net Investment Income Tax � Additional Medicare Tax

ACA Tax Provisions � Small Business Health Care Tax Credit � Helps small businesses and small tax-exempt organizations afford the cost of covering their employees � Specifically targets those with low- and moderate-income workers � Designed to encourage small employers to offer health insurance coverage

ACA Tax Provisions � Small Business Health Care Tax Credit � Small Employer � Fewer than 25 FTE � Average wage less than $50,000/year � Pay at least half of single (not family) employee health insurance premiums

ACA Tax Provisions � Small Business Health Care Tax Credit � For 2010 to 2013 – maximum credit is 35% of premiums paid for small employers � For 2014+ changes to: � Maximum credit is 50% of premiums paid � To be eligible, must pay premiums on behalf of employees enrolled in a qualified health plan offered through a SHOP � Credit available for 2 consecutive taxable years

ACA Tax Provisions � Small Business Health Care Tax Credit � Even if did not owe tax, can carry unused credit back or forward to other years � Can claim expense for premiums in excess of the credit � Can file an amended return if you forgot to claim originally � File Form 8941 to calculate – include as general business credit on return

ACA Tax Provisions � Employer Shared Responsibility Payment � Transition relief provisions moved compliance to 2015; encourage voluntary compliance in 2014 � PCORI - $1 fee per number of lives covered for plan years ending before October 1, 2013 � $2 per covered life 10/1/13-9/30/14 � File on Form 720 – Quarterly Excise Tax Return for 2 nd Quarter following plan year end

Net Investment Income Surtax � Beginning with 2013 tax year, imposes a 3.8% surtax to all taxpayers whose income exceeds a certain “threshhold amount” � Theoretically a taxpayer in the 39.6% tax bracket could have a marginal rate of 43.4%

NII Surtax � The surtax applies to the LESSER LESSER LESSER of: LESSER � Net investment income - or - � Excess of Modified Adjusted Gross Income over applicable threshold amount � Threshold amounts: � Single, HOH - $200,000 � MFJ - $250,000 � Trusts/Estates - $11,650 (top bracket)

NII Surtax � Net Investment Income (NII) includes: � Interest � Dividends � Annuity Distributions � Rents � Royalties � Income from Passive activities � Capital Gains

NII Surtax � Net Investment Income (NII) does not include: � Salaries and Wages � Active business income � IRA Distributions. 401(k) Distributions � Self-Employment income � Gain on sale of active partnership or S Corporation interest � Tax-exempt interest � Social Security and Veterans benefits

NII Surtax � Example: � John is single and has an MAGI of $220,000. He has interest and dividends of $40,000. � John’s “surtax” base is the lesser of: � NII - $40,000 � MAGI over threshold - $220,000-200,000 = $20,000 � John pays a surtax of $760 ($20,000 x 3.8%)

NII Surtax � Interest � Some interest may be excluded if earned in a trade or business � Ordinary course of business � Not trading of financial commodities � Individual not a passive investor � Example – dentist earns income on extra cash in a money market – not excluded because not in the ordinary course of business

NII Surtax � What is a Passive activity? � Regulations under Section 469 automatically assume you don’t really participate in some activities � Puts the burden of proof on you to prove otherwise � Must prove you “materially participate” � Passive income is included in both sides of the NII calculation

NII Surtax � Proving material participation – 7 tests Participate > 500 hours per year 1. Participation constitutes substantially all of 2. the participation by all involved in the activity Participation more than 100 hours, and no 3. one participates more Significant participation over 100 hours in 4. the activity, and total participation in all significant activities over 500 hours

NII Surtax � Proving material participation – 7 tests 5. Materially participated in activity for any 5 of previous 10 tax years Personal service – 3 previous tax years 6. Generic facts and circumstances 7. After proving material participation, need to go back to exclusion test mentioned before to determine if you can exclude income.

NII Surtax � Example: Joe and Dan are 50/50 shareholders in an S Corporation and make widgets. Joe works 2,000 hours per year, Dan sits on the beach doing nothing. The company earns $1,000,000 of ordinary income during the year, allocated evenly to each. The company also earned $100,000 in interest from its money market account. What does each include in their NII?

NII Surtax � Answer � Joe excludes his $500,000 share of income because it meets the exclusion tests. He includes his $50,000 share of the interest income. � Dan includes his $500,000 share of income in the NII base because he does not meet the exclusion tests. He includes his $50,000 share of the interest income also.

NII Surtax � Owners with multiple companies � IRS recognizes you may not be able to meet the 500 hour requirement � Can group together multiple activities to test and prove material participation on a combined basis � Restrictions on types that can be grouped together � Once you elect to group, no turning back � IRS allowing changes to prior groupings if subject to NII only

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries