Norwegian Air Shuttle ASA Q3 2013 Presentation Europe’s best low-cost airline

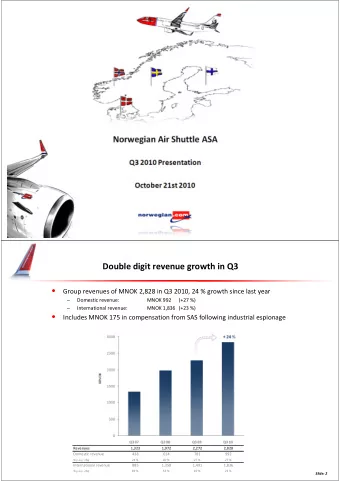

Europe’s best Double digit revenue growth in Q3 low-cost airline • Group revenues of MNOK 4,878 in Q3 2013 + 15 % 5 000 4 500 4 000 3 500 3 000 Domestic Revenue (MNOK) International Revenue (MNOK) 2 500 Total Revenues (MNOK) 2 000 1 500 1 000 MNOK 500 0 Q3 10 Q3 11 Q3 12 Q3 13 Revenues 2 828 3 376 4 224 4 878 Domestic revenue 992 958 1 071 1 072 % y.o.y. chg 27 % -3 % 12 % 0 % International revenue 1 836 2 419 3 153 3 806 % y.o.y. chg 23 % 32 % 30 % 21 % 2

Europe’s best Pre-tax profit of MNOK 604 in Q3 low-cost airline Q3 13 Q3 12 EBITDAR MNOK 1 169 1 098 EBITDA MNOK 778 822 EBIT MNOK 638 708 Pre-tax profit (EBT) MNOK 604 873 Net profit MNOK 436 628 EBITDAR development Q3 EBT development Q3 1 300 900 1 200 873 1 206 800 1 169 1 100 1 098 733 1 000 700 686 900 600 800 604 840 MNOK MNOK 500 700 600 400 500 300 400 300 200 200 100 100 0 0 Q3 10 Q3 11 Q3 12 Q3 13 Q3 10 Q3 11 Q3 12 Q3 13 EBITDAR margin 30 % 36 % 26 % 24 % EBT margin 26 % 20 % 21 % 12 % 3

Europe’s best Underlying EBT result MNOK 932 low-cost airline • Estimated long-haul wet-lease, fuel & irregularity effects MNOK 101 – Planned wet-lease MNOK 64 – Increased fuel consumption A340 vs B788 MNOK 19 – IRR cost MNOK 18 • Start-up costs Long-Haul, LGW & ALC unadjusted for (business as usual) 4

Europe’s best Extraordinary summer weather affected late bookings low-cost airline Fw d. Bookings (%) 2012 leisure routes from the Nordics (avg. for 2013 Share of available seats sold on typical departure during the month of July) Pre-sale period Departure 25 2013 23 average for departures in July Avg. daily max temperature ( °C ) preceding week (Oslo) - 21 2012 19 17 15 7 2012 6 average for departures in July Avg. daily precipitation (mm) 5 preceding week (Oslo) - 4 2013 3 2 Väderöarna, Bohuslän in Western 1 Sweden, August 23 rd 2013 5

Europe’s best Ancillary revenue remains a significant contributor low-cost airline • Ancillary revenue comprises 11 % of Q3 revenues (target 15%) • NOK 90 per scheduled passenger (an increase of 5 % from last year) 6

Europe’s best Cash position of NOK 2.3 billion (+568 million) low-cost airline Cash flows from operations in Q3 13 MNOK 67 (MNOK 460) Cash flows from investing activities in Q3 13 MNOK -618 (MNOK -565) Cash flows from financing activities in Q3 13 MNOK -68 (MNOK 267) Cash and cash equivalents at period-end MNOK 2 303 (MNOK 1735) CONDENSED CONSOLIDATED STATEMENT OF CASH FLOW Unaudited Q3 Q3 YTD YTD Full Year (Amounts in NOK million ) 2013 2012 2013 2012 2012 Net cash flows from operating activities 67.4 459.7 2 113.4 1 575.1 2 021.6 Net cash flows from investing activities -617.9 -564.9 -1 161.4 -1 220.1 -2 765.5 Net cash flows from financial activities -67.9 267.4 -378.2 276.1 1 369.4 Foreign exchange effect on cash -1.7 -1.8 -1.9 -1.3 0.3 Net change in cash and cash equivalents -620.1 160.4 571.9 629.8 625.8 Cash and cash equivalents in beginning of period 2 922.9 1 574.4 1 730.9 1 104.9 1 104.9 Cash and cash equivalents in end of period 2 302.9 1 734.8 2 302.9 1 734.8 1 730.9 7

Europe’s best Equity improved by MNOK 561 compared to last year low-cost airline • Total balance of NOK 14.4 billion • Net interest bearing debt NOK 3.4 billion (2.7) • Equity of NOK 2.9 billion at the end of the third quarter • Group equity ratio of 20 % (22 %) 14 000 Long term 12 000 liabilities 5 386 Non-current 10 000 assets 10 011 4 454 Other 8 000 current 7 611 liabilities 3 505 6 000 2 312 Pre-sold tickets 4 000 2 530 Receivables 1 763 2 047 1 562 2 000 Equity MNOK Cash 2 940 2 379 1 735 2 303 0 Q3 12 Q3 13 Q3 13 Q3 12 8

Europe’s best High load factor maintained on 31 % capacity growth low-cost airline • Average flying distance up 11 % 11 000 1 ASK Load Factor + 31 % 10 000 86.4 % 86.1 % 84.7 % 84.4 % 82.6 % 82.2 % 81.8 % 81.4 % 80.5 % 9 000 0.8 8 000 68.5 % 7 000 0.6 6 000 5 000 0.4 4 000 Available Seat KM (ASK) 3 000 0.2 2 000 Load Factor 1 000 0 0 Q3 04 Q3 05 Q3 06 Q3 07 Q3 08 Q3 09 Q3 10 Q3 11 Q3 12 Q3 13 ASK 683 1 033 1 694 2 333 3 590 3 979 5 331 6 480 7 780 10 223 Load Factor 68.5 % 86.4 % 84.7 % 86.1 % 81.8 % 82.2 % 80.5 % 84.4 % 82.6 % 81.4 % 9

Europe’s best Passenger record in Q3 low-cost airline • 6.0 million passengers • An increase of 800,000 passengers +16 % 6.00 5.00 4.00 3.00 2.00 Passengers (million) 1.00 0.00 Q3 04 Q3 05 Q3 06 Q3 07 Q3 08 Q3 09 Q3 10 Q3 11 Q3 12 Q3 13 Pax (mill) 0.5 0.9 1.5 2.0 2.6 3.1 3.8 4.6 5.2 6.0 10

Europe’s best Highest growth at London Gatwick low-cost airline • Increasing market share in all Nordic markets • Norwegian accounted for 90 % of growth at London Gatwick + 231,000 pax 40 % 35 % 30 % + 212,000 pax 25 % + 131,000 pax Gatwick total market: +271,000 20 % Norwegian at Gatwick: +243,000 + 119,000 pax 15 % + 149,000 pax + 243,000 pax 10 % 5 % 0 % Marketshare Marketshare Marketshare Marketshare Marketshare Int'l Marketshare Int'l Oslo Airport Stockholm Airport Copenhagen Airport Helsinki Airport Gatwick Airport Spanish bases (OSL) (ARN) (CPH) (HEL) (LGW) (AGP, LPA, ALC) Q3 08 29 % 10 % 2 % 0 % 0 % 2 % Q3 09 35 % 12 % 8 % 0 % 2 % 3 % Q3 10 39 % 14 % 10 % 2 % 3 % 3 % Q3 11 38 % 19 % 11 % 8 % 4 % 4 % Q3 12 37 % 21 % 15 % 10 % 4 % 5 % Q3 13 39 % 23 % 17 % 12 % 6 % 6 % 11

Europe’s best Unit cost excluding fuel down 3 % low-cost airline • Underlying unit cost down 7 % – Excl. fuel hedge, EUR & USD effect MNOK 65 – Excl. Long-Haul wet lease, fuel & IRR costs MNOK 101 -3% Fuel share of CASK 0.40 CASK excl fuel Operating cost EBITDA level per ASK (CASK) 0.11 0.35 0.15 0.14 0.13 0.30 -3% 0.29 0.28 0.27 0.27 0.25 Q3 10 Q3 11 Q3 12 Q3 13 Cost per ASK (CASK) (NOK) 0.41 0.41 0.41 0.40 CASK ex. fuel 0.29 0.27 0.28 0.27 Other losses / (gains) is not included in the CASK concept as it primarily contains hedge gains/losses offset under financial items* as well as other non-operational income and/or cost items such as gains on the sale of spare part inventory amd unrealized foreign currency effects on receivables/payables and (hedges of operational expenses). *Norwegian hedges USD/NOK to counter foreign currency risk exposure on USD denominated borrowings translated to the prevailing currency rate at each balance sheet date. Hedge gains and losses are according to IFRS recognized under operating expenses 12 (other losses/ (gains) while foreign currency gains and losses from translation of USD denominated borrowings are recognized under financial items.

Europe’s best Aiming for FY CASK NOK 0.25 excluding fuel low-cost airline Scale economies New more efficient aircraft Growth adapted to int’l markets • • • Uniform fleet of Boeing 737-800s Flying cost of 737-800 lower than 737-300 Cost level adapted to local markets • • • Overheads 737-800 has 38 “free” seats Outsourcing/ Off-shoring • • 3 new 737-800 delivered in Q3 (13 y.o.y.) Unchanged unit fuel consumption in Q3 due to A340-300 wet lease Crew and aircraft utilization Optimized average stage length Automation • • Self check-in/ bag drop • Rostering and aircraft slings optimized Fixed costs divided by more ASKs • • Automated charter & group bookings • Q3 utilization of 12.2 BLH pr a/c (+0.3 BLH) Frequency based costs divided by more ASKs • • Streamlined operative systems & processes Q3 sector length up by 11 % 13

London: Europe’s best low-cost airline Growth on short-haul & adding long-haul In operation Capacity increase New S14 TOS TRD AES HEL OSL BGO ARN TRF SVG d GOT AAL CPH LONDON (Gatwick) BUD NCE SPU DBV BCN FCO CFU JFK PMI IBZ ALC FAO AGP CTA LCA JTR LAX ACE TFS FUE LPA FLL 14

Europe’s best New crew bases in New York and Florida low-cost airline • JFK with most departures in Norwegian’s long-haul network • 15 weekly roundtrips from NYC to Europe from summer 14 ARN OSL Stockholm Oslo CPH JFK Copenhagen OAK New York San Francisco LGW London MCO Orlando LAX BKK Los Angeles FLL Bangkok Ft. Lauderdale 15

Europe’s best Competitors are national airlines flying internationally low-cost airline «Other European companies are capable of coping without creating this kind of creative corporate structures» Petter Førde, Chairman, Norwegian Pilots Association Majority of members fly for SAS and other competitors (Mr. Førde flies for Widerøe) “Other European Companies” have a very different business model 16

Europe’s best Improved product in all Scandinavian domestic markets low-cost airline LYR KKN LKL KRN ALF 3W 1 TOS ANX BDU EVE LLA S S 1 6 2 +1 +1 BOO +1 6 1 5 UME +1 5 4 TRD 2 MOL AES ARN 4 15 Route with more departures S14 vs S13 +1 5 +2 Route with no change S14 vs S13 +1 +1 6 S 15 New daily number of departures GOT BGO +2 4 15 VBY +2 Change from S13 to S14 2 OSL 5 3 3W Weekly number of departures 13 +2 HAU 3 TRF SVG S Seasonal MMX KRS 17

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries