SLIDE 1

Wiener Institut für Internationale Wirtschaftsvergleiche The Vienna Institute for International Economic Studies

www.wiiw.ac.at

Mario Holzner New wiiw forecast for Central, East and Southeast Europe, 2014-2016 Investment to the Rescue

Press Conference, 13 March 2014

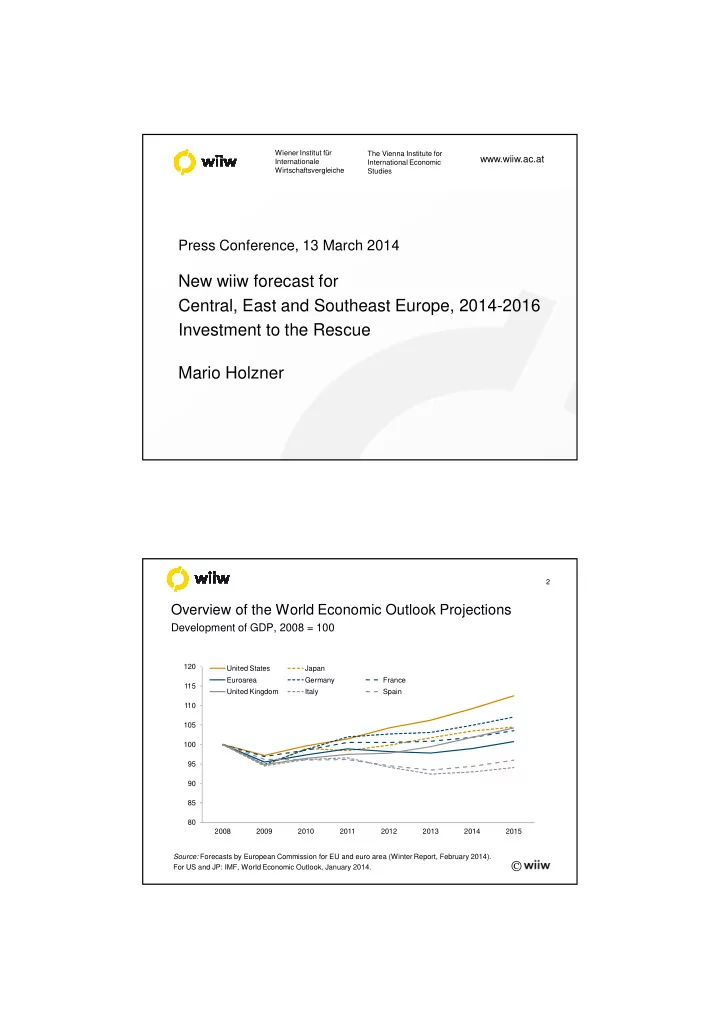

2 Source: Forecasts by European Commission for EU and euro area (Winter Report, February 2014). For US and JP: IMF, World Economic Outlook, January 2014.

Overview of the World Economic Outlook Projections

Development of GDP, 2008 = 100

80 85 90 95 100 105 110 115 120 2008 2009 2010 2011 2012 2013 2014 2015 United States Japan Euroarea Germany France United Kingdom Italy Spain