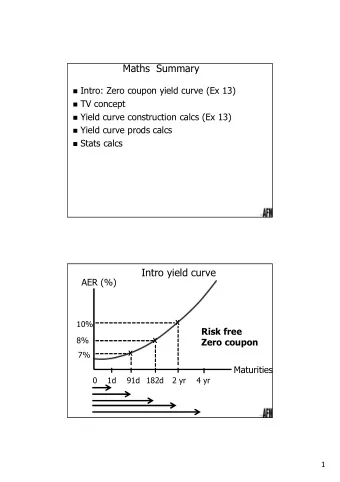

MARCH, 2014

Market Leader in High-Yield Pre-Owned CV Financing Shriram Transport Finance Company Limited (STFC) is one of the q Operating Revenue Break Up largest asset financing NBFC with approximately 25% market share in pre-owned and approximately 5-6% market share in new truck FY14 – Rs. 7.88 bn FY13 – Rs. 6.56 bn financing Strategically present in high yield - pre-owned CV financing with q expertise in loan origination, valuation and collection Expanded product portfolio to include financing of tractors, small q commercial vehicles, 3-wheelers, passenger commercial vehicles and construction equipment Large customer base in excess of 1.1 mn as of March 31, 2014 q Employee strength of approximately 18,122 including 11,209 product/ q credit executives as of March 31, 2014 Listed on the National Stock Exchange and Bombay Stock q Exchange with a market capitalisation of over Rs. 160 bn Foreign institutional investor holds more than 53 percent of the q company equity. Large Assets Under Management ( as on Marcg 31, 2014) Extensive Distribution Network Total Assets Under Management (AUM) Pan-India presence through a network of q q ● Pre-Owned CV: Approximately Rs. 465.54 bn ● 654 branch offices ● New CV: Approximately Rs. 62.50 bn ● 629 rural centres ● Others: Approximately Rs. 2.98 bn Partnership with over 500 Private Financiers q 4

Corporate History q Securitised Rs. 87.57 bn during FY 2010. 2010 q Successfully raised Rs. 5.84 bn through QIP with AUM: Rs 531.02 bn domestic & international investors. As of March 31, 2014 q Successfully placed Rs. 10 bn of NCD with domestic investors q Purchased hypothecation loan outstandings of commercial 2009 vehicles and construction equipments of GE Capital Services India and GE Capital Financial Services (GE) aggregating to approximately Rs. 11 bn q Merger of Shriram Investment Ltd. and Shriram Overseas Finance Ltd. 2005-06 With STFC ; PAT crosses Rs. 1,000 mn (2006) q Investment from ChrysCapital (2005) and TPG (2006) q Preferential Allotment to Citicorp Finance (India) in 2002 2002-04 q Preferential Allotment to Axis Bank and Reliance Capital in 2004 q Tied up with Citicorp for CV financing under Portfolio Management Services (PMS) 1999 AUM: Rs. 2.44 bn q The 1 st securitization transaction by STFC 1990 q Investment from Telco & Ashok Leylond 1984 q Initial Public Offering 1979 q STFC was established 5

Unique Business Model CV Financing Business Model Pre Owned (5-12 Years & 2-5 Years Old CVs) New Lending yields 18-24% (5-12 years) Lending yields 14-16% Lending yields 15-16% (2-5 years) q Small truck owners (less than 2-3 trucks) with Target Segment q Existing customer base upgrading to new trucks underdeveloped banking habits Market Share q Leadership position with a market share of 25-27% q 5-6% q AUM of approximately Rs. 465.54 bn at the end of q AUM of approximately Rs. 62.50 bn at the end of Performance FY14 FY14 FY09 FY10 FY11 FY12 FY13 FY14 LCV 200,699 287,777 361,846 460,831 524,887 432,111 Vehicles sold during FY08-14 MHCV 183,495 244,944 323,059 348,701 268,263 200,627 Total 384,194 532,721 684,905 809,532 7,93,150 632,738 6

With a Strong Financial Track Record Total Income Net Interest Income (Rs mn) 84,000 (Rs mn) 78,882.6 77,000 65,635.9 36,478.9 39,000 70,000 34,536.1 58,938.8 36,000 32,261.4 54,010.5 63,000 29,078.5 33,000 56,000 30,000 44,955.4 49,000 22,175.5 27,000 24,000 42,000 21,000 35,000 18,000 28,000 15,000 21,000 12,000 14,000 9,000 7,000 6,000 3,000 0 0 2010 2011 2012 2013 2014 2010 2011 2012 2013 2014 Net Profit EPS (Rs mn) (Rs) 66 59.98 55.72 55.59 15,000 13,606.2 60 54.49 14,000 12,298.8 12,642.1 12,574.6 54 13,000 12,000 48 41.09 11,000 8,731.1 42 10,000 9,000 36 8,000 30 7,000 6,000 24 5,000 18 4,000 3,000 12 2,000 6 1,000 0 0 2010 2011 2012 2013 2014 2010 2011 2012 2013 2014 7

Driven by Fast Growth in AUM with Low NPAs AUM (Rs bn) 550& 490& 430& 182.3& 166.3& 370& 182.3& 310& 163.2& 250& 111.8& 190& 364.7& 314.4& 130& 219.9& 198.7& 179.8& 70& 10& NPA Levels +50& 2010& 2011& 2012& 2013& 2014& 4.5% Off+Books& On+Books& 4.0% 3.9% 3.5% 3.2% 3.1% 2.8% 2.6% 3.0% 2.5% 2.0% 1.5% 1.0% 0.7% 0.8% 0.4% 0.4% 0.5% 0.8% 0.0% FY'10 FY'11 FY'12 FY'13 FY'14 Net NPA Gross NPA 8

Strengths 1 Widespread Geographical Reach 2 Valuation Skills & Recovery/Collection Operation 3 Strong Balance Sheet 4 Strong Management Team 5 Organizational Structure: Credit Risk Focus 6 Strengthening Presence and Expanding Reach 10

Geographical Reach & Proximity to the Customer Branch Locations Across India Pan-India Presence 654 Branch Offices & 629 Rural Centres Tie up with Appx. 500 Private Financiers 18,122 Employees including 11,209 Field Officers Regional Split of Branches States with STFC Presence As on March 31, 2014 11

2 Valuation Skills & Recovery/Collection Operation: Leveraging on Relationships Valuation Skills: q Knowledge driven valuation model Considerable expertise in valuation ● of pre-owned trucks 60%-70% Loan-to-Value Valuation skills is critical to ● Ratio – Old CVs Vehicle Assessment succeed in this space given that 75%-85% Loan to Value Ratio – New CVs the amount of loan, EMI and a truck operator ’ s ability to repay rests on the value of the truck Recovery/Collection Operation: In-house Administered Loan Recovery q ● Due to underdeveloped banking habits of small truck operators, a large part of monthly collections is Field Officers Vast Customer Base in the form of cash ● Compulsory monthly visits to borrowers by field officers help in managing large cash collections ● Continuous monitoring of Knowledge & Relationship based Recovery Procedure disbursed loans Experience in credit appraisal & recovery/collection operations has lead STFC to become one of the leading organized players in the sector 12

3 Healthy Asset Quality Prudent Credit Norms NPA Levels Substituted formal credit evaluation tools, such as IT q 4.5% returns and bank statements, with personal understanding 3.86% 4.0% of the customers ’ proposed business model Client and truck-wise exposure limits 3.5% q 3.20% 3.06% 2.83% 3.0% 2.64% Reasons for Low Delinquency 2.5% Asset backed lending with adequate cover q 2.0% Assets are easy to repossess with immediate liquidity q 1.5% Target segment generally operates on state highways and q short distances, ferrying essential commodities 0.71% 0.83% 0.77% 1.0% 0.44% 0.38% Incentive Schemes 0.5% Well-defined incentive plan for field officers to ensure low q 0.0% FY10 FY11 FY12 FY13 FY14 default rates Field officers are responsible for recovery of loans they q Net NPA Gross NPA originate Over 79% coverage between Gross/Net NPA as on March, 2014 13

3 Has Attracted Strong Interest from Quality Investors Current Shareholding Consistent track record and q Key Shareholders* % age (Mn Shares) high growth potential has attracted reputed institutional Shriram Capital 59.10 26.05 and private equity investors to infuse growth capital Piramal Enterprises 22.60 9.96 Last fund raising : Allotted q Genesis Indian Investment Company 13.65 6.02 11.658 mn equity shares at Rs. Ontario Teachers 11.32 4.99 500.80 per share to Qualified Institutional Buyers (QIB) for an Sanlam Life Insurance 11.27 4.97 aggregate sum of Rs. 5.84 bn Centaura Investments 7.53 3.32 resulting in a dilution of around 5.20% to 45 marquee global as Stiching Pensioenfonds ABP 3.55 1.57 well as domestic funds and Smallcap World Fund 2.30 1.01 insurers, which included 22 existing investors and the rest, Public & Others 95.56 42.11 new investors on January 28, 2010 Total 226.88 100.00 Capital Adequacy ratio as of q March 31, 2014 : 23.39% * As on March 31, 2014 Large Investments by major Institutional and Private Equity Investors 14

3 Optimized Balance Sheet : Access to Low Cost Funds Borrowings Funding Mix as % of Overall Liabilities Strategic mix of retail deposits and institutional funding q 100% Average cost of funds declined over the years with q increase in Bank/ Institutions liabilities 80% Access to fixed rate long term loans of 3 - 5 years due to q strong relationships with public, private sector, foreign banks and institutions 78% 79% 60% 80% 82% 82% 40% Securitization Securitization of loan book at regular intervals to fund new q 20% originations and maintain growth momentum. 22% 21% 20% Securitized assets portfolio stands at Rs. 166.28 bn at the 18% q 18% end of FY14 0% FY'10 FY'11 FY'12 FY'13 FY'14 Conservative recognition of income on account of q Retail Banks/Institutions amortization of securitization income over the tenor of the agreements Credit Ratings Long term rating: AA+ from CARE & AA from CRISIL Highest short term rating: F1+ from Fitch & P1+ from CRISIL 15

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries

![TDR Assumptions for Pulsed Neutron Yield [/keV] Neutron Yield [/keV] 2500 2000 2000 2500](https://c.sambuz.com/892356/tdr-assumptions-for-pulsed-s.webp)