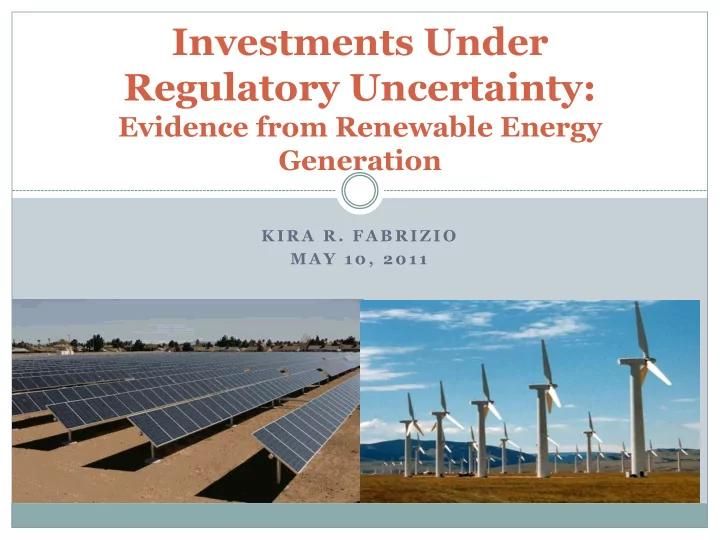

Investments Under Regulatory Uncertainty: Evidence from Renewable - PowerPoint PPT Presentation

Investments Under Regulatory Uncertainty: Evidence from Renewable Energy Generation K I R A R . F A B R I Z I O M A Y 1 0 , 2 0 1 1 Avg. Annual Post-RPS MW Investment ME: 23 NH: 8 830 100 119 NY: 222 MA: 7 CT: 4 165 105 NJ: 3 600

Investments Under Regulatory Uncertainty: Evidence from Renewable Energy Generation K I R A R . F A B R I Z I O M A Y 1 0 , 2 0 1 1

Avg. Annual Post-RPS MW Investment ME: 23 NH: 8 830 100 119 NY: 222 MA: 7 CT: 4 165 105 NJ: 3 600 MD: 34 33 226 16 271 44 27 1585

Two ways to view this paper Policy Impact Theory Similar RPS policies How does uncertainty were passed in similar about future policy states with widely stability affect firms’ different results. Why? response to policies?

This is related to TCE theory and empirical studies on ―political risk‖ International business literature includes studies of the impact of political risk on FDI Governance of transactions takes place within a particular institutional environment determines transaction hazards (Williamson 1991) ―Political risk‖ in a country determines firm’s willingness to invest in long-lived, sunk assets and therefore impacts the governance structures that firms select. Cross-national empirical evidence that greater restraints on regulators / political actors are associated with more infrastructure investment (Levy and Spiller 1994, Henisz and Zelner 2001). The risk of future change to regulatory policy creates the potential for ex post expropriation of return on firms’ investments.

Regulatory instability impedes investment in renewable generation assets RPS policies seek to promote investment in new renewable generation assets. Large, sunk capital investments Location specific (most valuable in-state) and expensive to relocate Much less valuable in ―next - best‖ use, i.e. in the absence of RPS policy Where there is more uncertainty about the stability of the RPS policy, firms will be less willing to invest in long-lived, specific generation assets.

Empirical test Prediction: Firms invest less in renewable generation assets in response to RPS policy in states with more regulatory uncertainty. Diff-in-Diff Model annual state-level MWs of new renewable generation as a function of: RPS policy (or StateGap) RPS policy * Regulatory Uncertainty State-year controls : Electricity price Non-RPS Demand for renewable energy: GSP, population, elec. sales and growth, sierra club membership, % democrats in legislature Existing supply of renewable energy: state and region eligible renewable generation capacity, other policies State (conditional) & Year (unconditional) fixed effects Method: Quasi-Maximum-Likelihood Poisson w/ conditional state FEs (Wooldridge 1999, Simcoe 2007)

Measuring RPS Policy Policy indicator variable (0/1) turns on in policy effective year. Up to 10 years after the RPS policy was enacted. Allows for construction lead time for generation projects. If projects come online early (before the effective year), creates conservative bias in estimates. Measure unmet portion of RPS-created demand. Required % X Target year sales = Required MWhs of renewable energy. Eligible installed MWs X Capacity Factor = Eligible MWh Supply of renewable energy. Required Sales – Eligible Supply = Unmet demand ( StateGap )

How to measure regulatory uncertainty? Want to capture the perceived likelihood of repealing or modifying the RPS policy. Option 1: Use prior repeal of electricity industry deregulation policy as an indicator of policy instability in the state. 24 states passed restructuring legislation between 1996 & 2001 8 later repealed it between 2001 & 2007

Source: Energy Information Administration Website

How to measure regulatory uncertainty? Want to capture the perceived likelihood of repealing or modifying the RPS policy. Option 1: Use prior repeal of electricity industry deregulation policy as an indicator of policy instability in the state. Option 2: Instrument using institutional characteristics that determine likelihood of repeal: Elected PUC commissioners (13 states), formalized consumer advocate (30 states) (Holburn & Vanden Bergh 2006) Party of governor and alignment in executive & legislature (Henisz 2000)

Employ novel state-year level dataset Annual MW investments in renewable generation assets, 1990-2010 Platts (UDI) North American database of electric power producers. Plant level data; on-line year, location, status, plant type, company type RPS policy histories: US Dept. of Energy DSIRE database Effective date, target, annual requirements for each RPS policy Restructuring policy histories: US Energy Information Administration (EIA) Dates restructuring policy passed / repealed State-level institutions: Consumer Advocate (Holburn & Vanden Bergh 2006), Elected commissioners (NARUC) Executive — Legislative party & alignment (Census Bureau) Annual controls from a variety of sources Census Bureau, Bureau of Economic Analysis, EIA, DSIRE, Sierra Club

Summary statistics suggest that investment increased more post-RPS in states w/o repeal States States With Without Repeal of Restructuring Repeal of Restructuring 28.31 44.95 Pre-RPS Annual MW Investment in new Renewable Generation Assets (5.41) (10.84) 203.93 108.40 Post-RPS Annual MW Investment in new Renewable Generation Assets (57.93) (27.75) Pre-to-Post Increase in MW Investment 175.62 63.45 (28.71)** (25.49)* Includes observations only for states that passed RPS policies. N=366 (w/o, pre), 75 (w/o, post), 100 (w/, pre), 26 (w/, post). SE in parentheses, *significant at 5 percent level, **significant at 1 percent level.

Results suggest regulatory uncertainty is an important determinant of investment Dep Var.: MWs of new renewable gen in state-year T6(2) T6(4) RPS 0.812 0.863 (0.288)** (0.440)* Repeal X RPS -1.349 (0.413)** ISO 0.748 0.693 (0.376)* (0.420) Post Interconnect -0.578 -0.614 (0.228)* (0.243)* Restructure 1.190 0.856 (0.466)* (0.535) Restructure X RPS 0.322 (0.451) Observations 1029 1029 Log Likelihood -26435 -26053

Results suggest regulatory uncertainty is an important determinant of investment 9 8.15 8 7.03 7 MWs Renewable Generation 6 5 4 3 2 1 0.4 0 RPS (model 2)* RPS w/ Repeal RPS w/o Repeal* * Predicted effect statistically significant at the 5% level.

Investments to meet ―State Gap‖ are sensitive to uncertainty, those to meet ―Region Gap‖ are not. T7(2) T7(3) StateGap 0.078 0.093 (0.027)** (0.030)** Repeal X StateGap -0.070 -0.082 (0.022)** (0.024)** RegionGap 0.022 (0.011)* Repeal X RegionGap 0.007 (0.015) ISO 1.000 1.106 (0.480)* (0.477)* Post Interconnect -0.537 -0.633 (0.253)* (0.248)* Restructure -0.475 -0.434 (0.518) (0.531) Restructure X RPS -0.635 -0.795 (0.408) (0.436) Observations 1008 1008 Log Likelihood -22980 -22692

Interpretation: Policy instability Results demonstrate that investments increased less post-RPS in states with prior repeal, relative to other states. Is policy instability the culprit? Predict repeal of restructuring as a function of institutional characteristics of the state. Elected PUC commissioners, formalized consumer advocate, Democratic governor. Two-stage Poisson estimates generate results consistent with those reported here (in appendix).

Concerns & Limitations Are there pre-existing trends in investment that differ across RPS and non-RPS states? No. Are states that repealed restructuring systematically different in a way that impacts investments? No. Are RPS policies different in states that repealed restructuring? No. Small number of observations (49 states). Do results from electricity industry generalize?

What do we learn? Uncertainty about future regulatory change impacts firm investments… Especially when investments are specific to the regulatory policy, long- lived, expensive to relocate. Policy makers will struggle to have an impact with initiatives when they can’t credibly commit to policy stability. This generalizes to many other contexts where investments are specific to policy regimes: healthcare, intellectual property, carbon policy. Credible commitments to policy initiatives may be required to get firms to respond. Create mutual dependence: Invest to in assets specific to policy (e.g. transmission) or limit alternatives (e.g. natural gas) Decrease ability to change policy: Create procedural hurdles that reduce risk of policy renegotiations (e.g. Federal & State APA) OR ― vertically integrate ‖ to achieve the policy goals [in this case, the government investing in renewable generation assets themselves]

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.