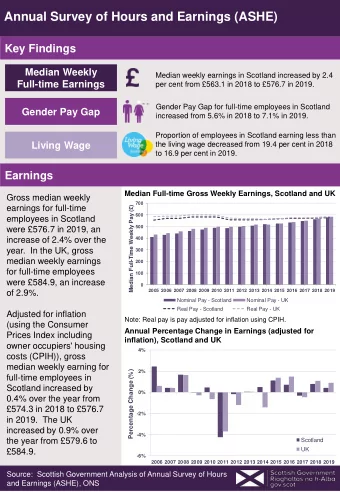

Increased Information Content of Earnings Announcements in the 21st Century An Empirical Investigation William Beaver 1 Maureen McNichols 1 Zach Wang 2 1 Stanford University 2 University of Illinois at Urbana-Champaign March 31, 2017 Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Three-Day Abnormal Return Volatility from 1971 to 2011 (Beaver, McNichols and Wang 2017) Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Empirical Measure of the Information Content of Earnings Announcements ◮ Use one-day announcement windows to maximize power ◮ Adjust for after-hours earnings announcements using timestamps from Bloomberg and IBES (Patell and Wolfson 1982, Berkman and Truong 2009) ◮ Measure the information content using One-Day Abnormal Return Volatility (Beaver 1968) µ 2 i , t USTAT i = Var µ i ◮ The numerator is Announcement Return Squared (Day 0) ◮ The denominator is Non-Announcement Return Volatility (Day-130 to Day-10, Day+10 to Day+130) Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Research Questions ◮ Why does the information content increase after 2001? ◮ Less volatility in non-announcement windows? ◮ Higher unexpected earnings or stronger response to earnings? ◮ More concurrent disclosures other than earnings? (Francis, Schipper and Vincent 2002a) ◮ How does the information content of earnings announcements compare to that of other events? ◮ Prior research suggests the importance of management guidance and analyst forecasts (Ball and Shivakumar 2008, Beyer, Cohen, Lys and Walther 2010) ◮ The information content of stand-alone earnings ◮ Stand-alone guidance and analyst forecasts ◮ By year and across all years ∗ The information content of earnings announcements includes information about earnings and other disclosures issued at the same time. Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Sample Selection Firm-Quarters from 325,386 Compustat Quaterly between 1999 and 2012 With earnings announcement 109,141 time stamps from Bloomberg With time stamps from IBES 131,944 after the match with Bloomberg Remove observations without (84,301) time stamps Firm-Quarters with time stamps 241,085 Remove observations with fewer than 40 trading (564) days in the non-announcement periods Final Sample Size 240,521 Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

11-day Mean Abnormal Return Volatility based on Compustat Days Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

After-hours Earnings Announcements % Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

11-day Mean Abnormal Return Volatility based on Bloomberg and IBES Time Stamps Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

One-Day ( USTAT ) Information Content Twice As Much As Three-Day ( TCU ) Information Content Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Announcement and Non-Announcement Days Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Unexpected Earnings and Earnings Response Coefficient Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Concurrent Disclosure by Firms and Analysts ◮ Management Forecast ◮ More bundling during the Post-Reg FD periods (Anilowski, Feng and Skinner 2007, Rogers and Van Burskirk 2013) ◮ Contain forward-looking information (Waymire 1984) ◮ Analyst Forecast ◮ Selective disclosure to analysts prohibited during the Post-Reg FD periods ◮ Complement the informativeness of earnings (Lang and Lundholm 1996, Francis, Schipper and Vincent 2002b, Frankel, Kothari and Weber 2006) ◮ Financial Statement Line Items ◮ Increasing trend from 1980 to 1999 (Francis, Schipper and Vincent 2002a) ◮ Complement the informativeness of earnings (Hoskins, Hughs, and Ricks 1986, Livnat and Zarowin 1990, Francis, Schipper and Vincent 2002b, Chen, Defond and Park 2002, D‘Souza, Ramesh and Shen 2010) Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

% of Quarterly Earnings Announcements with Concurrent Management Guidance Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Mean USTAT Guidance and No-Guidance Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

% of Quarterly Earnings Announcements with Concurrent Analyst Forecast Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Mean USTAT Forecast and No-Forecast Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Mean % Financial Statement Items in Press Releases Following D‘Souza et al. (2010) Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Mean USTAT by FS Quartiles Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Multivariate Results Regressor USTAT USTAT USTAT USTAT USTAT USTAT T 0.467*** 0.360*** 0.387*** 0.377*** 0.374*** 0.231*** t-stat 9.87 10.18 8.89 8.22 7.72 6.50 GUIDANCE 2.576*** 2.231*** t-stat 9.44 8.67 AF 2.645*** 2.321*** 8.39 8.93 t-stat FS 4.217*** 7.87 t-stat IS 1.642** 1.104* 2.15 1.94 t-stat BS 1.826*** 1.477*** t-stat 4.69 4.23 SCF 1.192*** 1.021*** t-stat 2.58 2.61 Controls? Yes Yes Yes Yes Yes Yes AdjR 2 4.43% 5.02% 5.08% 4.85% 4.86% 5.84% Nobs 148102 148102 148102 148102 148102 148102 Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Earnings Announcement vs. Guidance - Number of Observations Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Earnings Announcement vs. Guidance - USTAT Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Earnings Announcement vs. Analyst Forecast - Number of Observations Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Earnings Announcement vs. Analyst Forecast - USTAT Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Conclusion ◮ Previous results using three-day or longer announcement windows understate the information content of earnings announcements. ◮ One-day announcement windows exhibit roughly twice the price response observed for three-day windows. ◮ Concurrent disclosure positively associated with the information content of earnings announcements ◮ Management guidance, analyst forecasts and disaggregated line items ◮ At best partially explain the time trend ◮ Relative return volatility on stand-alone earnings announcement dates ◮ Surpass that on stand-alone guidance from 2007 to 2012 ◮ More than twice that on stand-alone analyst forecast dates Increased Information Content of Earnings Announcements in the 21st Century (Beaver, McNichols and Wang)

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries