IMPACT OF FRAUD ON REVENUE COLLECTION

BACKGROUND The legislative background & mandate of the SRA. ➢ SRA established in terms of section 3 of the Swaziland Revenue Act, 2008. ➢ Key Function of SRA: To assess and collect all revenue on behalf of the Government. ➢ Also, SRA is tasked with taking appropriate measures to counteract tax or revenue fraud or other forms of tax or revenue evasion. ➢ All collections to be soon sent to Govt. Account. 2

WHY REVENUE COLLECTION? So that Government can finance her operations such as: ➢ Roads and building infrastructure; ➢ Education, schools, scholarships, etc.; ➢ Salaries for civil/public servants; ➢ Health and pharmaceutical supplies; ➢ Millennium Development Goals ➢ Etc. 3

WHY COLLCETION BY SRA? It’s a world standard to establish such semi-autonomous agencies to collect revenue on behalf of governments. The privatization of revenue collections gives good governance and efficiency benefits. 4

WHY COUNTERACT FRAUD? ❖ Fraud could leak already collected revenue – e.g. fraudulent refund claims ❖ Fraud can either postpone revenue collection or revenue not collected at all. ❖ Revenue targets may not be met. ❖ Fraud could lead to importation of prohibited or harmful goods into the country to the detriment of society. 5

EXAMPLES OF FRAUDS IN REVENUE ▪ Forgery/manufacturing/alteration/deletion of documents, invoices, etc.; ▪ Falsification of financial statements (with intention of not paying required tax or duties); falsification of certificates of origin/import permits/export permits; ▪ Changing of company names and directorship with the sole purpose of fleeing from tax liability; ▪ Etc. 6

ANTI-FRAUD PROGRAMS IN SRA ➢ Documentation & Management of business processes (to achieve consistency, certainty, minimize discretions – process deviations could be red flags for fraud and corruption); ➢ Systems Automation (minimize human error and keep audit trails for operations and benefits of management reports); ➢ Existence of adequate risk management framework (e.g. standardized incident reporting, identification and monitoring of risks, etc.); ➢ Existence of anti-fraud policies and their enforcement; ➢ Internal & External Audits 7

…… ..ANTI-FRAUD PROGRAMS IN SRA ➢ Hotlines for tips ➢ Fraud & Corruption sensitizations initiatives ➢ Surprise audits ➢ Dedicated ant-fraud / corruption units ➢ Proactive data monitoring & analysis ➢ Employee background checks Notable challenges to these control measures: ✓ Stakeholder collaboration needs enhancement ✓ Rewarding of whistle-blowers for tips still an issue 8

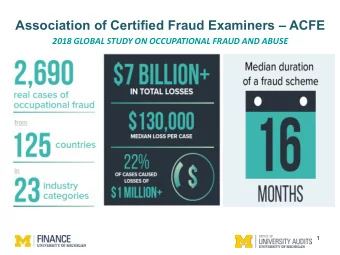

LESSONS FROM FRAUD FIGHTING ▪ The longer the fraud remains undetected, the greater the harm inflicted onto an organization; ▪ In 95% cases, perpetrators of fraud take efforts to conceal the frauds through creation or altering of documents; ▪ The most common detection methods are tips through hotlines; ▪ The “2016 Report to the Nations” by ACFE reveals that much as hotline tips work, but frauds uncovered through active detection methods (i.e. surveillance, monitoring or account reconciliation), the loss on duration of the fraud is lower; 9

EXPECTED BENEFITS FROM AFCE The localization of AFCE is expected to have the following benefits: ▪ Increase up-skilling of personnel through training and education in the country ▪ Widening of the anti-fraud community in the country ▪ Reduction of fraud in business and governmental organizations 10

Thank you… 11

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries