SLIDE 1

0 8 0 5

Month Day Total No. of Stockholders Domestic Foreign LCU Cashier File Number Document ID

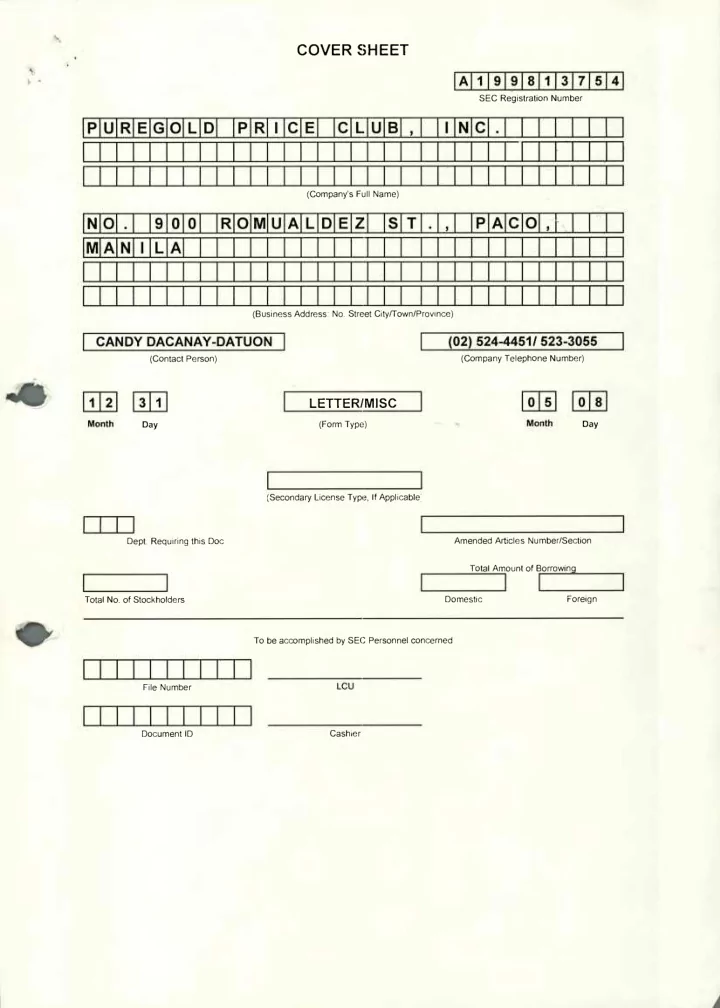

CANDY DACANAY-DATUON

(Contact Person)

(02) 524-4451/ 523-3055

(Company Telephone Number)

2 3

1

Month Day

- Dept. Requiring this Doc

LETTER/MISC

(Form Type) (Secondary License Type, If Applicablej Amended Articles Number/Section Total Amount of Borrowing To be accomplished by SEC Personnel concernedCOVER SHEET

A 1 9 9 8 1 3 7 5 4

SEC Registration Number

P U R E G O L D P R

C i E C L. U B

N C

(Company's Full Name)N O 9 0 0 R O M U A L D E S T P A C O

M

A N

L

A

(Business Address: No. Street City/Town/Province)