How ASEAN Economies Coping with Global Slow Growth and the newly US - PDF document

How ASEAN Economies Coping with Global Slow Growth and the newly US Trade Regime (1 st International Conference of Asia Economic Research Institute, Saint Petersburg State University (SPSU), Saint Petersburg, Russia, 30 March 2017) Dr. Anggito

How ASEAN Economies Coping with Global Slow Growth and the newly US Trade Regime (1 st International Conference of Asia Economic Research Institute, Saint Petersburg State University (SPSU), Saint Petersburg, Russia, 30 March 2017) Dr. Anggito Abimanyu Former Chairman Fiscal Policy DG, Ministry of Finance, Indonesia/Professor, Faculty of Economics and Business, Gadjah Mada University, Yogyakarta, Indonesia/Chief Economist, Bank BRI, Jakarta/Special Envoy to Indonesian Ministry of Trade, Jakarta-Indonesia Introduction The global economy remains in a low-growth trap. According to the October 2016 IMF forecast, the global GDP growth is set to be lowered around 3.1% in 2016 and improve modestly to 3.4% in 2017. US and EU are improving, although a slightly lower forecast due to weaker conditions in other major economies. Recent increased in the US FFR has indicated some improvement in the US economy. Weak global trade is remain a particular concern. World trade was growing exceptionally slowly after the financial crisis, and has collapsed in 2015 and 2016. This weak trade growth is both a symptom of and exacerbates the weak global environment. Trade matters for productivity, living standards and inclusive growth. Returning to robust trade growth requires policy action to deepen global integration, but even more importantly to share the benefits. The concern is not just that there has been a gradual rise over the past four years in the number of protectionist measures introduced, but that there is a risk of an anti-trade narrative taking root in the US recently. At the last year Hangzhou Summit, G20 countries were only around half-way to their target of 2% additional G20 GDP by 2018 due to sluggish progress on implementation on trade issues. More worrying with recent US stand point to create uncertainty over global trade that has been a real hurdle for the last hope of a strong recovery from another global financial crisis. The recent failure by the G20 Finance Minister meeting in Germany ended inconclusively after it dropped from its official communiqué language from last year that vowed to resist all form of protectionism. This US policy on trade will change to outlook of the emerging economies. Growth in developing East Asia and Pacific that is expected to remain resilient over the next three 1

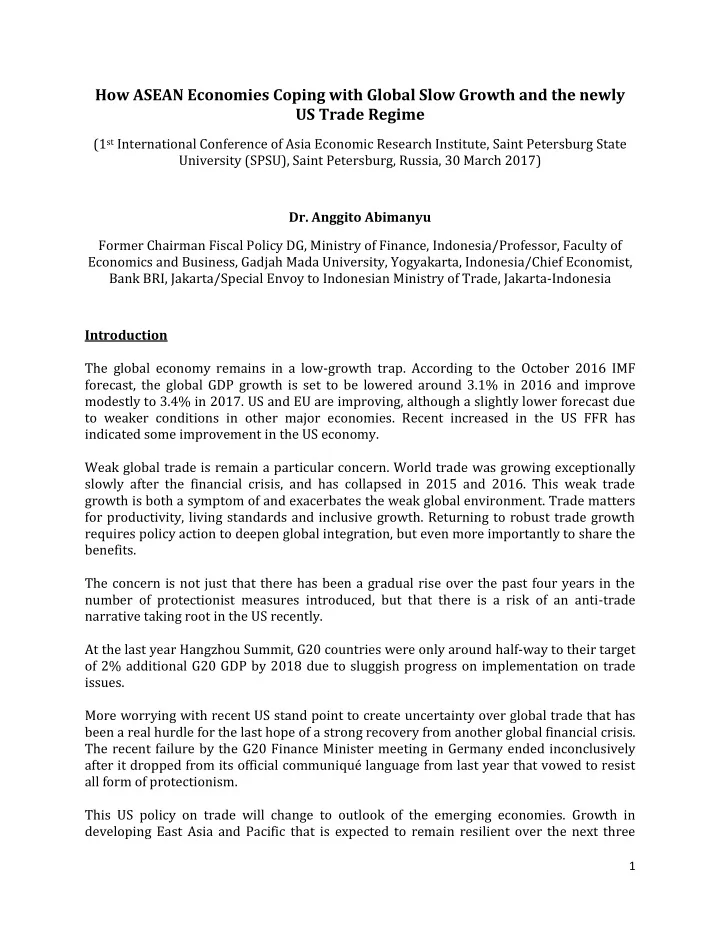

years might be at risk. The only hope will be the domestic demand to be remain robust across much of the region and investment in infrastructure continue to expand. Continued modest commodity prices will benefit commodity exporters and keep low inflation across most of the region will help the emerging economies in Asia. FTA/RTA in APEC and ASEAN FTAs/RTAs that open trade and advance policy cooperation can be helpful when progress at the multilateral level is slow. But narrow country coverage and the discriminatory application of tariff reductions and other market access provisions limit the benefits. While the application of RTA provisions on a non-discriminatory basis is welcome, the many different RTAs can develop diverging rules. For Asia-Pacific countries, the recent US position toward globalization has brought about a complex scenario where opposition to strengthening economic integration has grown. Moreover, uncertainty the US to support further economic integration and continue engagement in the pursuit of new RTA will be a global risk. Initially APEC members are looking for more ambitious trade agreements. The TPP negotiations, the ongoing intensive negotiations of the RCEP and the preparation of a Collective Strategic Study on Issues Related to the Realization of the Free Trade Area of the Asia Pacific are evidence of the interest by APEC economies to strengthen links to effectively promote a free and open trade and investment system. But with decision of President Trump to pulls US out Pacific Trade pact, the TPP status is now uncertain. Attention in the region has begun to turn to RCEP, which covers Australia, Brunei, Cambodia, China, Indonesia, India, Japan, Laos, Malaysia, Myanmar, New Zealand, the Philippines, Singapore, South Korea, Thailand and Vietnam will also being questioned. While some TPP members feel that they could create a parallel agreement without the US, the economic benefits will be significantly reduced without the US participating. Therefore, some TPP member countries may prefer to refocus on the RCEP as an alternative large- scale regional trade liberalisation initiative. This development need to be observed in the near future. ***** The ASEAN Economic Community (AEC) officially started at the end of 2015 earlier than the original plan in 2020. Such a goal would have been difficult for nearly any grouping to reach. For ASEAN, the gaps in economic development has been significant. To bring together nations ranging in GDP per capita now, from Myanmar at just over USD$1.265 to Singapore at more than USD$52,000 would have been challenging under any timeline. But ASEAN leaders made the task more difficult by moving the deadline forward by five years. Instead of 2020, the ASEAN Economic Community would take effect in 2015. Thus member states with an ambitious deadline suddenly faced the conclusion five years sooner than anticipated. Fortunately, ASEAN has had a mechanism for releasing the pressure. Members could reach any goal by using pilot projects. In addition, ASEAN works on the ASEAN Minus X system where somewhere between 10 and 0 members actually move forward with 2

any commitment. No one actually checks for implementation. The ASEAN Secretariat is very small and has no capacity to ensure that members follow through on their various commitments. Services are supposed to be opened as well on the way towards the AEC. By 2014, members had agreed on eight “packages” of market opening. Each package is designed to open up a set of subsectors for other ASEAN firms. For example, each member might decide to open up hotels, clinics or accounting firms. Of the 160 subsectors, ASEAN members have already agreed to open up roughly 65. Not all commitments are likely to be equally meaningful for companies. The AEC also includes free movement of investment. ASEAN members have made limited progress towards meeting this goal. Skill Labor movement and investment are not likely to be significantly opened for the rest of this year. The free movement of goods (other than tariffs), services, investment, skilled labor and freer movement of capital are likely to prove elusive. The US is the number one-two trading partner to ASEAN economies in last two decades. Any trade and investment policy adopted by the US will have a variety impact to ASEAN economies. As for the impact of recent higher US interest rate, ASEAN economies are not homogenous and the impact are unlikely to be uniform. Countries with external financial imbalances or a reliance on external funding would be the most vulnerable to the effects of higher rates. This is why Indonesia for example — have been hit the most since QE reduction started late last year with their currencies weakening as US money flowed back to the US. With an outflow from local currencies into USD, GBP and potentially Yen, downward exchange pressure will come onto local currencies. The result will be either ASEAN governments use their foreign currency holdings to prop up their local currency, or their currencies will depreciate. This stronger dollar increase global commodity prices, such as oil, mining, mineral and agriculture. The modest increase in commodity prices together with weaken local currency since last quarter 2016 help commodity export based ASEAN economies, such as Malaysia, Thailand, the Philippines, Indonesia and Vietnam to improve their balance of trades. On the other hand, consumer expectations of higher US and international interest rates may dampen global consumption spending, hence reducing demand for ASEAN exports. Higher interest rates also raise the borrowing cost of and debt burdens on the government and public sector. ***** In anticipating of slow global growth, individual ASEAN, no other choice but to further launched numerous policy reforms, with some sectors – in particular, trade and investment policy – witnessing a shift towards deregulation and more integration. ASEAN economies such as Indonesia, Myanmar, Brunei, Vietnam have improved positions in the World Bank Doing Business 2016-17 ranking. While others, such as Singapore, Malaysia, the Philippines 3

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.