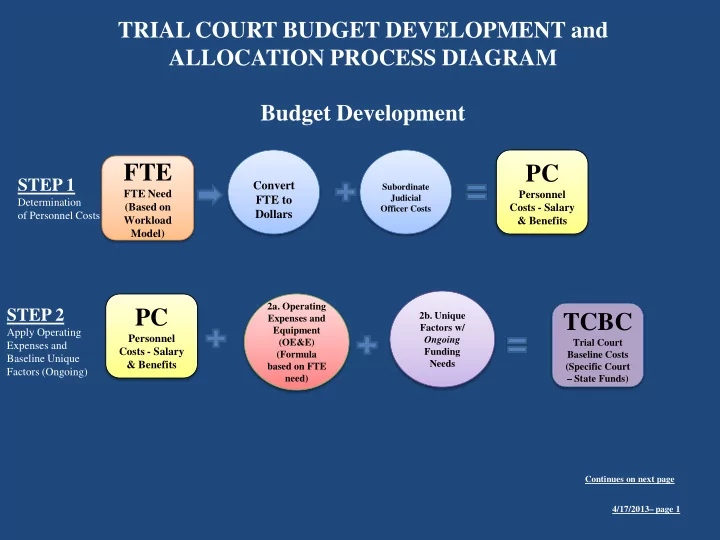

TRIAL COURT BUDGET DEVELOPMENT and ALLOCATION PROCESS DIAGRAM Budget Development FTE PC STEP 1 Convert Subordinate FTE Need Personnel Judicial FTE to Determination (Based on Costs - Salary Officer Costs Dollars of Personnel Costs Workload & Benefits Model) 2a. Operating PC STEP 2 2b. Unique TCBC Expenses and Factors w/ Equipment Apply Operating Personnel Ongoing (OE&E) Trial Court Expenses and Costs - Salary Funding (Formula Baseline Costs Baseline Unique Needs & Benefits based on FTE (Specific Court Factors (Ongoing) need) – State Funds) Continues on next page 4/17/2013– page 1

TRIAL COURT BUDGET DEVELOPMENT and ALLOCATION PROCESS DIAGRAM Budget Development (cont.) 3. Costs of STEP 3 programs w/ TTBC TCBC Additional dedicated state Expenditures funding sources/ TOTAL TRIAL Trial Court reimbursements from State COURT Baseline Costs (ex. Security, BASELINE Funding (Specific Court COSTS Dependency Sources – State Funds) (Specific Court – Counsel, Jury, State Funded) AB1058, AB 109) TTBA TTBC 4a. Costs STEP 4 associated w/ Total Trial TOTAL TRIAL programs or Court Baseline Additional COURT services Costs (Specific Expenditures BASELINE funded w/ Court – All Local Funding COSTS local revenue Funding (Specific Court – Sources Sources) State Funded) TTBA TTCB STEP 5 Total Trial 5a. Approved TOTAL TRIAL Court Baseline One-Time One-Time COURT BUDGET Costs (Specific Costs and Continues on next page Costs / NEED Court – All BCPs Budget (Specific Court – Funding Change All Sources) 4/17/2013– page 2 Sources) Proposals

TRIAL COURT BUDGET DEVELOPMENT and ALLOCATION PROCESS DIAGRAM Budget Development (cont.) STEP 6 The State “Ask” STCN TTBC 5a. Approved SUM: TOTAL TOTAL TRIAL SUM: One-Time STATEWIDE COURT Costs and TRIAL COURT BASELINE BCPs COSTS BUDGET NEED (Specific Court – (All Courts – State State Funded) Funds) 4/17/2013– page 3

Recommendation of the TCBWG 1. Approve the Workload-based Allocation and Funding Methodology (WAFM) for use in allocating the annual state trial court operations funds, consistent with the implementation schedule below, with the understanding that ongoing technical adjustments will continue to be evaluated by the TCBWG and that those adjustments will be submitted to the Judicial Council for approval.

Recommendation of the TCBWG 2. Direct the TCBWG to provide annual updates of the WAFM beginning with the April 2014 Judicial Council meeting.

Recommendation of the TCBWG 3. Adopt the five-year implementation schedule for the WAFM outlined below: a. In fiscal year (FY) 2013–2014 the currently estimated $261 million in unallocated reductions shall be allocated to each court on a pro rata basis (based upon each court’s current share of the statewide total of all applicable funds);

Recommendation of the TCBWG FY 2013–2014: • 10% allocated pursuant to the WAFM • 90% allocated pursuant to the FY 2013–2014 historically based funding methodology • The state’s smallest courts would be excluded from any change in their allocation based upon the WAFM in FY 2013–2014

Recommendation of the TCBWG FY 2014–2015: • 15% allocated pursuant to the WAFM • 85% allocated pursuant to the historical based funding methodology FY 2015–2016: • 30% allocated pursuant to the WAFM • 70% allocated pursuant to the FY 2013–2014 historical based funding methodology

Recommendation of the TCBWG FY 2016–2017: • 40% allocated pursuant to the WAFM • 60% allocated pursuant to the FY 2013–2014 historical based funding methodology FY 2017–2018: • 50% allocated pursuant to the WAFM • 50% allocated pursuant to the FY 2013–2014 historical based funding methodology

Recommendation of the TCBWG c. Allocate any new money appropriated for general trial court operations entirely pursuant to the WAFM; and d. Reallocate applicable base funding pursuant to the WAFM on a dollar-for-dollar basis for any new money appropriated for general trial court operations.

TRIAL COURT BUDGET DEVELOPMENT and ALLOCATION PROCESS DIAGRAM Allocation Process – Proposed FY 13/14 Budget Act Statewide Totals for: REVENUE for 3. Costs of programs w/ REVENUE for dedicated state STATE TRIAL 1e. funding sources/ STEP A Subordinate COURT TOTAL reimbursements Judicial ALLOCATION Determine (ex. Security, Officer Costs (Budget Act) Dependency Funding Counsel, Jury, Available for AB1058, AB 109) Court Operations Z STATE TRIAL COURT OPERATIONS ALLOCATION 4/17/2013– page 4

TRIAL COURT BUDGET DEVELOPMENT and ALLOCATION PROCESS DIAGRAM Allocation Process –Proposed FY 13/14 ( ) Z 90% H% STEP B STATE TRIAL COURT Historic Determine OPERATIONS Funding Local Court ALLOCATION Percentage Share of General ( Operations ) Funding TC% Z 10% Trial Court’s STATE TRIAL Percentage COURT Share of OPERATIONS Workload ALLOCATION Driven Need TCOF REVENUE for 1e. INDIVIDUAL Subordinate TRIAL COURT Judicial Officer Costs OPERATIONS FUNDING 4/17/2013– page 5

TRIAL COURT BUDGET DEVELOPMENT and ALLOCATION PROCESS DIAGRAM Allocation Process –Proposed FY 13/14 REVENUE for REVENUE 3. Costs of for programs w/ TCOF 4a. Costs dedicated state STEP C associated w/ funding sources/ INDIVIDUAL programs or Determine reimbursements TRIAL COURT services Individual Court’s (ex. Security, OPERATIONS funded w/ Dependency Total Budget FUNDING local revenue Counsel, Jury, AB1058, AB 109) ITCFB INDIVIDUAL TRIAL COURT FINAL BUDGET 4/17/2013– page 6

Parking Lot Items (to be addressed in Phase 2) Rev. A April 8, 8, 2013 2013

1. Reevaluation of the effect of future changes in the judicial branch budget • Consider how cuts should be handled beginning in FY 14- 15 if the cuts occur after: a. new money was received in the prior year b. no new money was received in the prior year • Consider what the recommendation should be if there is “new money” but it is only one-time new money (e.g., it is designated one-time in the budget bill or its source is one- time funding such as the IMF) 15

2. Improvement and validation of the data to determine workload • Validate the data used in the new model, including the accuracy of the data and consideration of factors other than filings, such as: Factor into workload determination “access to justice standards”/best practices Case complexity • Develop a “unique factors” protocol, including a process for requesting modification of revenue allocation • Develop a process for updating the WAFM as the filings, or any other factors used to develop “workload,” change in individual counties 16

3. Reevaluation of the role of salary and benefits • Evaluate impacts of new model in cluster #1 courts and make permanent adjustments as necessary • Evaluate manager to staff ratios currently in the new workload model • Evaluate Program 90 ratios currently in the new workload model • Evaluate how to include employee benefits in the new workload model (FY 13-14 model funds benefits at actual costs) • Consider BLS deflators for Program 90 salaries separate from those for Program 10 salaries 17

3. Reevaluation of the role of salary and benefits (cont’d) • Consider removing courtroom staff from new model (leave as is first year) and determine whether to make adjustments based on unmet judgeship needs • Reevaluate the salary component to consider the following: a. Employee salaries may be higher due to the distant location of outlying courts b. Compare salaries to other courts in the region rather than to all other government employees in the county 18

4. Evaluation of the impact of outside factors on funding or expenses related to operations • Evaluate self-help funding in the new workload model • Evaluate alternative ways of allocating technology funding • Evaluate impact of AOC provided services • Evaluate 1058 revenue as an offset • Extra staffing for multiple locations • Consider how any recommendations should be related to judgeship needs or otherwise make reference to judgeship needs • Evaluate whether and how Civil Assessments should affect funding allocations (and consider any relationship to MOE) 19

5. Evaluation of the impacts of outside factors on funding or expenses unrelated to court operations • Whether and how to treat unfunded costs not included in requests for the new model, e.g., payments for courthouse construction • Evaluate whether and how MOE should affect funding allocations (and consider relationship to civil assessments) 20

End of Presentation 21

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries