CLS Holdings plc Half-Yearly Financial Report

CONTENTS > Business Review 2 How We Operate 3 Financial Highlights 4 Chairman’s Statement 6 Business Review Accounts > 10 Responsibility Statement 11 Independent Review Report to CLS Holdings plc 12 Condensed Group Statement of Comprehensive Income 13 Condensed Group Balance Sheet 14 Condensed Group Statement of Changes in Equity 15 Condensed Group Statement of Cash Flows 16 Notes to the Condensed Group Financial Statements 32 Glossary of Terms 33 Directors, Officers and Advisers

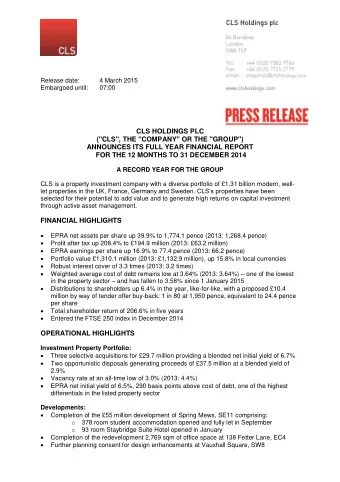

CLS Holdings plc Half-Yearly Financial Report INVESTORS IN EUROPEAN COMMERCIAL PROPERTY LISTED SINCE 1994 > Shareholders’ funds of £438 million > EPRA net assets of £523 million > £1 billion of office properties across London, France, Germany and Sweden > Top UK property company total shareholder return performance in the last 5 years > Strong alignment of interest with shareholders: management owns 54% > Substantial cash and liquid resources available for new investment > Cautiously entrepreneurial approach to future opportunities PROPERTY INVESTMENTS BY VALUE France Germany 24% 21% Sweden (Direct) 6% London 46% Sweden (Indirect) 3% GENERATING CASH THROUGH HIGH NET INITIAL YIELD AGAINST LOW COST OF DEBT 01

HOW WE OPERATE OUR GOAL IS TO CREATE LONG-TERM SHAREHOLDER VALUE WE AIM TO ACHIEVE OUR GOAL BY: > PURSUING AN OPPORTUNISTIC INVESTMENT STRATEGY > FOCUSING ON CASH RETURNS > OPERATING IN DIVERSE LOCATIONS > UTILISING DIVERSIFIED SOURCES OF FINANCE > MAINTAINING A BROAD CUSTOMER BASE > MINIMISING VACANT SPACE > IMPOSING STRICT COST CONTROL > RETAINING A HIGH LEVEL OF LIQUID RESOURCES 02

CLS Holdings plc Half-Yearly Financial Report FINANCIAL HIGHLIGHTS EPRA net assets per share: up 6.0% to 1,223.7 pence (31 December 2012: 1,154.4 pence) > EPRA net assets: up 3.9% to £522.8 million (31 December 2012: £503.4 million) > EPRA earnings per share: up 7.5% to 33.0 pence (2012: 30.7 pence) > EPRA profit before tax: up 8.9% to £19.5 million (2012: £17.9 million) > Cash flow from operating activities: up 4.9% to £15.0 million (2012: £14.3 million) > Net assets per share: up 6.4% to 1,024.8 pence (31 December 2012: 963.1 pence) > Net assets: up 5.0% to £437.8 million (31 December 2012: £417.1 million) > Earnings per share: up 10.3% to 52.7 pence (2012: 47.8 pence) > Profit after tax: up 6.6% to £22.7 million (2012: £21.3 million) > Proposed distribution to shareholders: £5.0 million (September 2012: £4.6 million) by way of tender offer > buy-back: 1 in 113 at 1,320 pence, equivalent to 11.7 pence per share Low weighted average cost of debt: 3.55% (31 December 2012: 3.67%) > Interest cover: 3.8 times (year ended 31 December 2012: 3.9 times) > Adjusted solidity: 42.9% (31 December 2012: 41.1%) > Balance sheet loan to value: 51.4% (31 December 2012: 52.5%) > OTHER KEY DATA > Top performer in UK listed property sector total shareholder return since July 2008: 190.9% Portfolio value: £1,001.8 million – down 0.4% in local currencies > Proportion of rental income from Government tenants: 39% > > Occupancy rate: 94.5% > Indexation applies to 64% of contracted rent Liquid resources: £158.6 million > 03

CHAIRMAN’S STATEMENT A GOOD TIME TO BE BUYING PROPERTY OVERVIEW The Group has had a very active first six months Availability of debt is improving, with more lenders in the of 2013, with a number of successes for shareholders. Five market and better terms being offered. This is likely to lead acquisitions in London and Germany have helped the core to improved values for high yielding property in due course. investment portfolio to grow to over £1 billion in value and Net debt was unchanged at £592.3 million (31 December 2012: further acquisitions are being made in the second half. In £592.6 million) as acquisitions and additional development London, construction is well under way at Spring Mews, expenditure were financed in part from the proceeds of the Vauxhall and at Clifford’s Inn, Fetter Lane, and solid progress sale of corporate bonds. Our liquid resources, consisting of is being made in advancing our Vauxhall Square project. All cash and corporate bonds, nevertheless remained at a very this activity has led to EPRA net asset value growing by 6.0% healthy level of £158.6 million, reinforcing the strength of to 1,223.7 pence per share (31 December 2012: 1,154.4 pence). the balance sheet and our capacity to invest in the future. The economic development in our markets across Europe We have reduced the corporate bond portfolio in the period continues to be mixed: the unemployment level in France is from £127.3 million to £88.9 million, taking profits ahead almost double that of Germany; and sovereign debt levels of deteriorating market conditions in the second quarter. continue to grow. The corporate bonds generated a total return of £7.9 million, or 6.2%, in the six months. In August 2013, we sold a further Meanwhile, the core fundamentals of the Group’s business £68.4 million of corporate bonds over five days, and without strategy remain sound. The investment property portfolio affecting their individual prices, evidencing their very contains a diverse base of 450 occupiers across four markets liquid nature. generating rental income well in excess of the Group’s cost of debt, with 39% of rents paid by governments, 29% from major PROPERTY PORTFOLIO The value of the investment property corporations; 64% of rents are subject to indexation. The balance portfolio has grown to £1.0 billion, with the five acquisitions sheet continues to grow ever stronger with significant levels in the period, in London and Germany, totalling £34.2 million of cash and liquid resources and a widespread funding base with an annualised rental income of £3.36 million for a blended including 22 banks and other capital market funding sources. net initial yield of 10.01%. The Group has produced a Total Shareholder Return in six Rental income has grown in the period to £35.9 million, a like months of 30.1% with the share price reaching record highs for like increase of 6.1%, due in part to rental indexation, from in recent months. which 64% of the portfolio benefits. RESULTS AND FINANCING Profit before tax was £27.9 million The investment property portfolio’s underlying value rose by for the six months to 30 June 2013 (2012: £27.1 million), with 2.3% in the six months, including a foreign exchange gain from earnings per share of 52.7 pence (2012: 47.8 pence). EPRA sterling’s relative weakness against the euro and Swedish earnings per share were 33.0 pence (2012: 30.7 pence) and krona. In local currencies the underlying portfolio fell by 0.4%. EPRA profit before tax was £19.5 million (2012: £17.9 million). The London portfolio grew by 0.2%; developments added 3.2% after capital expenditure, acquisitions fell by 2.4% due to Shareholders’ funds have grown by 5.0% in the six months incidental transaction costs, and the remaining properties ended 30 June 2013 to £437.8 million after distributions to fell by 0.4%. The French portfolio reduced in value in local shareholders of £8.6 million. currency by 1.7%, reflecting the anticipated increase in the Interest cover remains a very healthy 3.8 times (2012: 3.9 times) vacancy rate due to exceptionally high lease expiries and the and the weighted average cost of debt has reduced further soft economic conditions which we highlighted earlier in to 3.55% (31 December 2012: 3.67%), which is one of the the year. The German portfolio increased in value by 0.8% lowest in the real estate sector of the London Stock Exchange. in local currency (excluding the acquisition), and its vacancy We continue to believe that interest rates will stay low, and, rate has been successfully reduced since the year end. therefore, in our hedging strategy we favour the use of interest Sweden’s property remained broadly level, down 1.1% in local rate caps. At 30 June 2013, net debt as a proportion of gross currency. Overall the vacancy rate at 30 June 2013 was 5.5% assets (less cash) was 51.4%. (31 December 2012: 3.8%). 04

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries