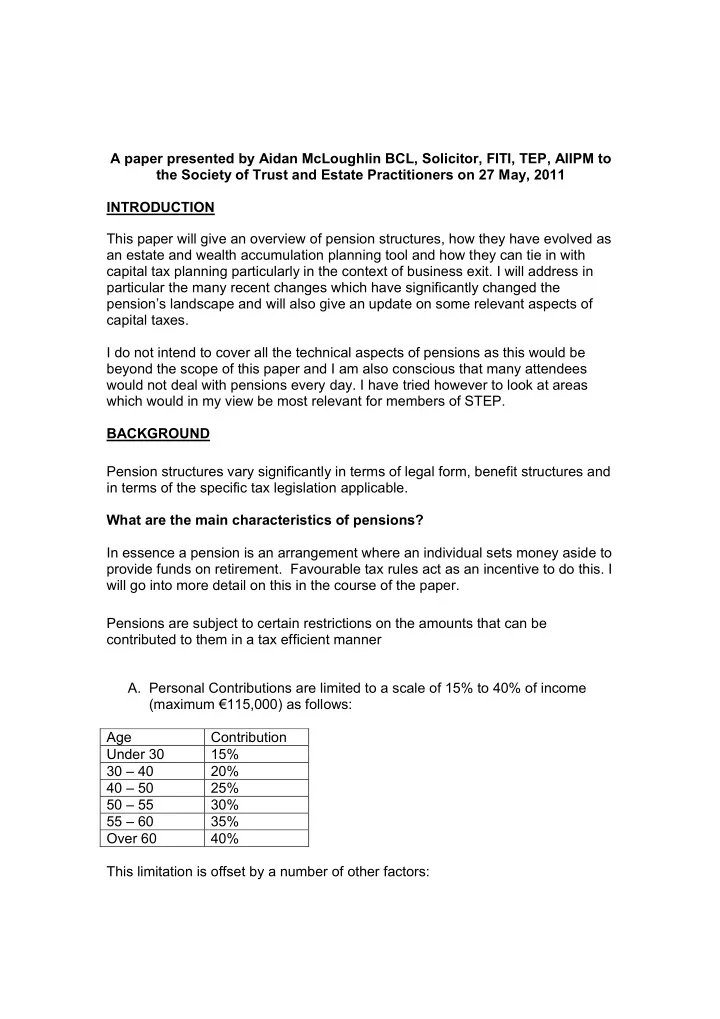

A paper presented by Aidan McLoughlin BCL, Solicitor, FITI, TEP, AIIPM to the Society of Trust and Estate Practitioners on 27 May, 2011 INTRODUCTION This paper will give an overview of pension structures, how they have evolved as an estate and wealth accumulation planning tool and how they can tie in with capital tax planning particularly in the context of business exit. I will address in particular the many recent changes which have significantly changed the pension’s landscape and will also give an update on some relevant aspects of capital taxes. I do not intend to cover all the technical aspects of pensions as this would be beyond the scope of this paper and I am also conscious that many attendees would not deal with pensions every day. I have tried however to look at areas which would in my view be most relevant for members of STEP. BACKGROUND Pension structures vary significantly in terms of legal form, benefit structures and in terms of the specific tax legislation applicable. What are the main characteristics of pensions? In essence a pension is an arrangement where an individual sets money aside to provide funds on retirement. Favourable tax rules act as an incentive to do this. I will go into more detail on this in the course of the paper. Pensions are subject to certain restrictions on the amounts that can be contributed to them in a tax efficient manner A. Personal Contributions are limited to a scale of 15% to 40% of income (maximum €115,000) as follows: Age Contribution Under 30 15% 30 – 40 20% 40 – 50 25% 50 – 55 30% 55 – 60 35% Over 60 40% This limitation is offset by a number of other factors:

These contributions are tax deductible In relation to Occupational Pension Schemes these amounts can be supplemented by virtually unlimited funding by the employer (subject to the funding cap discussed below) B. A further limitation exists in relation to the nature of the benefits. Some structures, particularly defined benefit occupational pension schemes for employees, have retirement benefits emerge primarily in income form. This means that when someone accesses their retirement benefits, they only have access to a source of income (i.e. an annuity) and do not have access to a capital asset. C. A third limitation is that in in most cases benefits cannot be accessed until age 50 /60. All of these negatives need to be considered in the light of the positives. In addition to tax relief on contributions pensions are entitled to: 1. Tax free cash on retirement 2. All or a substantial portion of the fund free from income tax on death before retirement 3. Potential, on death after retirement, for assets to transfer to children free from Capital Acquisitions Tax. 4. Exemption from Income Tax in respect of income derived from investments or deposits. 5. Exemption from Capital Gains tax on investments by the scheme. 6. Automatic tax relief on contributions paid by an employer. 7. Tax relief on personal contributions up to 15- 40% of allowable remuneration. 8. No benefit in kind on employee in respect of employer contributions to occupational pension schemes.. 9. Tax relief at source through the “net pay” arrangement. It is very important to note that there have been a lot of changes in this area recently, particularly in this year’s Finance Act and I will expand on these further. What are the main types of pension arrangements? For completeness it is worth noting that pensions are broadly defined as either state funded or private. The former would include social welfare pension benefits and public sector/local authority pensions. However these generally do not have a capital value and are therefore not amenable to transmission on death. I will deal therefore with private pensions in more detail. In general terms, funded pension schemes can be characterised either as:-

(i) Occupational Pension Schemes which are established by an employer for the benefit of employees. A key subset of these comprises Self Administered Schemes (SAPS) which includes Small Self Administered Pension Schemes (SSAPs); A key feature of almost all Occupational Pension Schemes is that they are established under trust. This has an important bearing on the security of the relevant assets as we will see later on. In addition the existence of a trust structure means that the benefits to be derived from such a scheme may not necessarily form part of the estate of a deceased but are capable of passing directly on foot of the benefit clauses of the trust. It should be noted that in many cases the estate is included as a possible beneficiary so executors should still make enquiries in relation to such schemes. (ii) Personal Pensions which are effected by individuals (either self employed or employees not covered by the first category of funded schemes) for their own benefit. A key element in this area of the market is the type of Personalised Pensions that have been developed in the last few years; Most Personal Pensions are established as policies of insurance. The one exception to this is in relation to group schemes established for particular occupations (the Law Society Scheme is a good example) which are typically established under trust. The comments above in relation to Occupational Pension Schemes therefore can also apply to such benefits. (iii) Personal Retirement Savings Accounts (PRSAs) which are a contract similar to the Personal Pension but with easier access for employees and additional controls in relation to costs etc. Such assets are part of the deceased’s estate. (iv) Approved Retirement Funds (ARFs) which are funded by monies transferred from one or both of the first three structures. Revenue Approval One of the key aspects is that formal approval must be obtained from the Revenue in relation to all types of schemes. Section 772(1) Taxes Consolidation Act provides a mandatory regime under which approval must be granted by the Revenue Commissioners to an occupational pension scheme. However, Sub-section (4) then goes on to provide: (a) The Revenue Commissioners may if they think fit having regard to the facts of a particular case and subject to such conditions, if any, as they

think proper to attach to the approval, approve a retirement benefit scheme for the purpose of this Chapter, notwithstanding that is does not satisfy one or more of the prescribed conditions. This discretionary power of the Revenue Commissioners has been utilised quite extensively and the rules which are applied by Revenue to govern schemes is set out in the Revenue Pensions Manual. Self Administered Pension Schemes It is worth setting out some specific details of self administered pension schemes as these would be most commonly found when dealing with directors of family owned businesses. Small self administered schemes are particularly suitable for owner-managed businesses. It is common that they are set up with one member who then has choice over the underlying assets in the fund (subject to restrictions). This is in contrast to most other types of pension arrangements where funds are pooled and are typically subject to prudent investment restrictions Similar to other defined contribution type schemes SSAPs can transfer to an Approved Retirement Fund (ARF) on retirement. One of the key aspects of the ARF regime is that it allows the pension holder to create a capital asset on retirement which is capable of being inherited on death. This contrasts with a situation where an annuity is acquired on retirement which then ceases on the death of the member. The definition of a small self administered scheme under Revenue rules involves two separate tests. Meeting either of these means the scheme is a small self administered scheme. 1. The scheme has less than 12 members (excluding certain staff with small benefits included to “make up the numbers”) 2. 65% or more of the fund is attributable to 20% Directors, their spouses or dependents. A number of restrictions apply to these kinds of schemes for example: Each scheme must have a Pensioneer Trustee Annual accounts and triennial funding reviews must be submitted to the Revenue Various Investment Restrictions apply.

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries