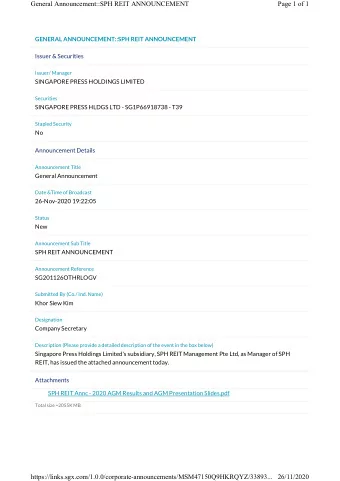

2018 Annual Results Announcement 22 February 2019 1

Disclaimer statements reflect the Company’s current expectations, beliefs, The information contained in this presentation is provided for informational purpose only, and should not be relied upon for the hopes, intentions or strategies regarding the future and assumptions purpose of making any investment or for any other purpose. in light of currently available information. Such forward-looking statements are not guarantees of future performance or events and Some of the information used in preparing this presentation was obtained from third parties or public sources. The information involve known or unknown risks and uncertainties. Accordingly, contained in this presentation has not been independently verified. actual results may differ materially from information contained in the No representation or warranty, expressed or implied, is made as to, forward-looking statements as a result of a number of factors. You and no reliance should be placed on, the fairness, reasonableness, should not place undue reliance on such forward-looking accuracy, completeness or correctness of such information or opinions contained herein. It is not the intention to provide, and you statements, and the Company does not undertake any obligation to may not rely on this presentation as providing, a complete or update publicly or revise any forward-looking statements. No comprehensive analysis of our financial or trading position or statement in this presentation is intended to be or may be construed prospects. The information and opinions contained in this as a profit forecast. presentation are provided as at the date of this presentation and are subject to change without notice and will not be updated to reflect We also do not undertake any obligation to provide you with access any developments which may occur after the date of this presentation. to any additional information or to update this presentation or any additional information or to correct any inaccuracies in this All statements, other than statements of historical facts included in presentation or any additional information which may become this presentation, are or may be forward-looking statements. Forward-looking statements include, but are not limited to, those apparent. using words such as “seek”, “expect”, “anticipate”, “estimate”, “believe”, “intend”, “project”, “plan”, “strategy”, “forecast” and similar This presentation does not constitute an offer or invitation to expressions or future or conditional verbs such as “will”, “would”, purchase or subscribe for any shares and no part of it shall form the “should”, “could”, “may” and “might” . These forward-looking basis of or be relied upon in connection with any contract, commitment or investment decision in relation thereto. 2

ASMPT Recognized as TOP 100 Global Tech Leaders ONLY Back-end Equipment Supplier Being Recognized “The Top 100 Global Technology Leaders are the organizations poised to propel the future of technology” , Brian Scanlon, Chief Strategy Officer Thomson Reuters, 2018 3

Corporate Overview 4

A World’s Technology & Market Leader 2018 Group Revenue (CAGR 2008-2018 14%) A leading Integrated Solutions Provider in the USD 2.49B semiconductor assembly and packaging industry as well as in the SMT solutions market A leading player for CIS, LED, and Automotive 47.4% Top 3 application markets accounted for 47% of group revenue in 2018 Back-end 41.1% Equipment SMT Solutions 11.5% Materials 5

ASMPT Global Presence Beuningen Weymouth Munich, Regensburg Boston Porto Chengdu Huizhou Taoyuan Shenzhen Hong Kong Sales Offices Johor Bahru Business Centre / R&D / Singapore Manufacturing Site >1,400 10 12 >2,000 Patents on key leading R&D centres Manufacturing Global R&D staff edge technologies worldwide facilities 6 6

ASMPT Major Facilities around the World Yishun Regensburg Boston Hong Kong Munich Longgang ( 龙岗 ) Fuyong ( 福永 ) Huizhou ( 惠州 ) Chengdu ( 成都 ) Porto Johor Bahru Expansion Taoyuan Beuningen Weymouth Johor Bahru (Ready 2019) 7

Three Business Segments With Leading Market Positions Worldwide Market Position & Share 1 Back-end Assembly & Packaging ~25% Equipment Equipment Market (2018) PAE #1 Die Bonders #2 Wire Bonders #1/2 Flip Chip Bonders #1 Thermal Compression Bonders (TCB) #1 LED Packaging Equipment #1 CMOS Imaging Sensors (CIS) Equipment #2 Encapsulation & Post Encapsulation Solutions #4 Turret Test Equipment (Test Handlers) #2 Laser Dicing and Grooving 1 SMT ~23% SMT Equipment Market SMT Solutions (2018) 3 ~9% Materials Leadframe Market Leadframe (2018) Sources: Market share for Back-end Equipment is based on information on packaging and assembly equipment market by VLSI, leadframe market by SEMI, and SMT market by ASMPT SIPLACE Market Intelligence 8

2018 Financial Highlights 9

Yearly Billings Group Billings BE EQT Billings YoY Growth: +11.6% (US$ m) (US$ m) YoY Growth: +7.3% 3,000 1,400 1,181 2,494 1,200 2,500 1,000 2,000 800 1,500 600 1,000 400 500 200 0 0 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018 Materials Billings SMT Billings YoY Growth: +19.1% YoY Growth: +5.2% (US$ m) (US$ m) 350 1,200 288 1,025 300 1,000 250 800 200 600 150 400 100 200 50 0 0 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018 10 10 10

Group Bookings Yearly Group Bookings (US$ m) Q4 Group Bookings: ▼ 4.5% YoY YoY Growth: +10.0% Q4 Backend: ▲ 4.0% YoY 3,500 Increased contribution from Advanced Packaging Q4 SMT Solutions: ▼ 2.5% YoY 3,000 2,575 Q4 Group Backlog: ▲ 21.6% YoY 2,500 2,000 Quarterly Group Bookings YoY Growth: -4.5% (US$ m) 1,500 800 600 1,000 474 400 500 200 0 0 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2014 2015 2016 2017 2018 14 14 14 14 15 15 15 15 16 16 16 16 17 17 17 17 18 18 18 18 11

Major Drivers for 2018 Bookings/Billings Back-end SMT Solutions IC / Discrete Automotive Discrete Automotive Semiconductors Consumer RF Filters IoT Power Management Industrial Advanced Packaging Smartphones (China + India) IoT 12

ASMPT Revenue Breakdown by Application Markets Mobility, Comm & IT, Optoelectronics and Automotive % of Group Revenue Automotive and Industrial advanced to #2 and #4 respectively 13

Sustainable and Gradually Increasing Dividends Dividend Per Share (HK cents) Dividend paid Share buyback Interim (HK cents) Final (HK cents) Payout Ratio 1,600 1,357 1,400 1,288 60.9% 59.0% 1,200 305 52.9% 52.6% 52.7% 349 51.5% 49.4% 926 1,000 HKD m 800 36.2% 270 521 250 600 487 240 210 1,052 190 939 80 140 400 140 130 260 130 110 40 91 85 200 160 30 130 50 120 100 80 80 61 35 - 2011 2012 2013 2014 2015 2016 2017 2018 2013 2014 2015 2016 2017 2018 Cumulative cash returned: HKD4.8bn 1H 2018 2H 2018 Full Year 2018 Share Buyback Program DPS 1.30 1.40 2.70 Amount exercised HKD654.1m, 1.49% of shares outstanding at 31 EPS 3.46 2.01 5.47 December 2018 Payout ratio 37.5% 69.9% 49.4% 14

We Are Ready to Ride the Next Wave of Growth 15

Future Is About Data and Only Just Beginning No single leading driver, but a fragmented growing market! 16 16

Market Expansion Led by Data Explosion Increased TAM for Back-End and SMT Advanced Packaging Heterogeneous 5G Integration MARKET GROWTH DRIVERS More Semiconductor No Latency Devices Higher Bandwidth Greater Storage High Performance Lower Power Computing TECHNOLOGY REQUIREMENTS Autonomous IoT Smart Data Centre Data Explosion Vehicle Factories By 2025... By 2030… By 2022… By 2021… ~8 million more AVs ~100 billion ~7 billion more 13.5 ZB more Data ~1.6 billion more Sensors more units M2M devices Transmission per year MEGA TRENDS 17

More than Moore: Heterogeneous Integration & Advanced Packaging Shifting the Value Chain Advantages of Heterogeneous Integration Key Enablers • Integrating multi-mode technologies to enable “More than Moore” • Faster time to market • Less IP issues Shrinkage of Die Heterogeneous Integration • Flexibility Geometry Advanced Packaging • Cost savings Source: Intel Artificial Intelligence requires “High Bandwidth & Low Power Data Pipes ONLY Available On Heterogeneous Integration on Advanced Packages” High Performance Computing Source: Intel 18

Advanced Packaging Contributed >10% Back-end Revenue in 2018 FIREBIRD Series (TCB) HBM / Memory 3D Memory / IC Stacking HI TCB Bonding X-PU Extra Large Die TCB Bonding Logic IC NUCLEUS Series 2.5D Silicon (Pick & Place) Interposer Extra Large Die Flip Chip Bonding Premium AP in Fan Out Technology Panel Level Active & Passive Embedding Embedded Component HDI Substrate NEXX (PVD | ECD) Integrated Passive Device, Bumping IPD integration TSV in Si Interposer RDL SIPLACE-CA (SMT Pick & Place) IPD Assembly AP will be a significant growth driver Board Level Assembly Module Level Decoupling Capacitor / Passive Component 19

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries