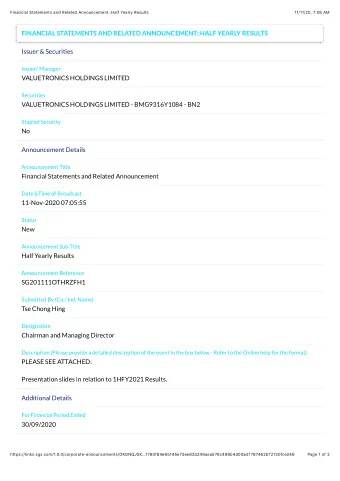

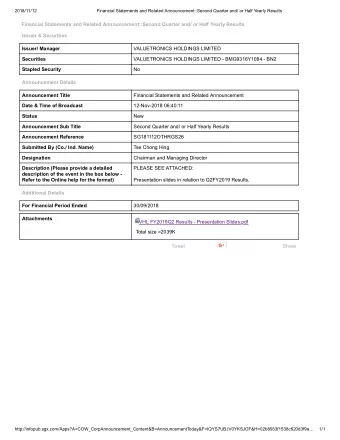

2015 Half-Yearly Results 20 August 2015

Forward looking statements This presentation may contain forward-looking statements and information that both represents management's current expectations or beliefs concerning future events and are subject to known and unknown risks and uncertainties. A number of factors could cause actual results, performance or events to differ materially from those expressed or implied by these forward-looking statements. August 2015 | P1

Agenda Introduction Tony Durrant UK Stuart Wheaton Sea Lion Neil Hawkings Exploration Robin Allan / Dean Griffin Finance Richard Rose Outlook Tony Durrant August 2015 | P2

2015 1H performance Operating cash flow of Increased cash flows: strong production, lower costs and $513 million hedging benefits (which continue into 2H and 2016) Production of Above budget and guidance year-to-date driven by 94% 60.4 kboepd operating efficiency Opex per barrel Many initiatives on-going; <$14/boe opex reduction Reduction in net debt to $2,093 million, despite investments Net debt stable in Solan and Catcher Renegotiated terms; vote of confidence by banks and Covenant flexibility bondholders Solan and Catcher On track for Q4 first oil from Solan and 2017 from Catcher milestones achieved Discoveries at Zebedee and Isobel Deep; Resource additions resource additions at Anoa Refocusing the Low cost acreage additions in Brazil and Mexico exploration portfolio August 2015 | P3

UK Stuart Wheaton UK Business Unit Manager

UK – underlying growth Solan Balmoral Area 89% operating 2015 1H efficiency • Averaged 16.9 kboepd • Improved operating efficiency • Opex $29/bbl, down 17% (1H 2014: $35/bbl) – Sale of high cost Scott area – Active cost management and Kyle Huntington G&A cuts • Sanctioned projects will see Premier’s UK production rise to c. 50 kboepd • $3.3 bn of UK tax losses and allowances Key projects Equity First Operator Reserves Wytch Farm interest oil/gas YE14 (gross) Catcher Balmoral Area c. 80% Various Premier 7 mmboe Catcher 50% 2017 Premier 96 mmboe Huntington 40% 2013 E.On 16 mmboe Kyle 40% 2001 CNR 5 mmboe 44 mmboe Solan 100% 2015 Premier Wytch Farm 30% 1979 Perenco 47 mmboe August 2015 | P5

Solan – long term vision • Reserves upside potential • Infill drilling opportunities; near field exploration • Nearby accumulations; potential 3rd party business over Solan hub facility • Consider farm down of equity post first oil Solan oil production rate (stb/d) 25,000 20,000 Cash 15,000 generative Potential ullage? 10,000 $26/bbl opex 5,000 (LOF) 0 2020 No tax August 2015 | P6

Solan – 2015 1H highlights On track for Q4 first oil • P1/ W1 tied in; P2 drilling • Improved offshore productivity • Removed partner funding concerns • Reduced balance sheet exposure • Cash spend to end July $1.65 billion August 2015 | P7

Solan – facilities update Bibby DSV Ocean Valiant Complete commissioning W2 to spud of subsea infrastructure o Bibby DSV First oil Tanker SOST & Ocean Valiant Offloading trials P1/W1 tied in P2 spudded 56,000 direct hrs to first oil 2015 1H Jul - Aug Sep - Oct Nov - Dec Habitation 20 men; 100-120 hrs/day Commissioning of production systems Victory Siem Spearfish Regalia flotel Superior flotel 250 men; 800-1,000 hrs/day 60 men; 180-280 hrs/day 135-150 men; 600-800 hrs/day 200-220 men; 1,000 hrs/day Completion of over-side Complete construction Commissioning of Commissioning of work & commissioning of works; commissioning of safety, accommodation, production systems emergency power systems accommodation & production systems, power generation & utilities August 2015 | P8

Solan – drilling and subsea P1 and W1 W1 • Completed and tied-in • P1 encountered 1,855 feet of sands • 10-15 kbopd P1 • First oil Q4 2015 P2 P2 and W2 W2 • P2 nearing completion Top Solan sand depth map • 3,000 feet of sands targeted 500m Pressure • W2 to spud in September data suggests good connectivity Field P2 cross-section • Ramp up to 25 kbopd once both Solan seal producer/injector pairs on-stream Subsea • Tank tied in • Commissioning to complete in September Solan pay sands Current bit position 250m P2 on prognosis August 2015 | P9

Catcher area Reservoir upside Near field tie-backs Exploration upside No tax Varadero 4P, 3I Catcher 5P, 2I Burgman 5P, 3I August 2015| P10

Catcher execution phase progressing • 96 mmboe (50 per cent, operator) • $1.6 bn (gross budget to first oil) • Post ramp up, peak production of c. 50 kbopd FPSO and SURF FPSO and SURF Acquired acreage Carnaby fabrication HUC as part of Oilexco discovery commenced Burgman and Development Formal concept Varadero select drilling discoveries 2009-2011 2012 2013 2014 2015 2016 2017 2018 SURF Catcher discovery installation Increased interest First Near field to 50% following DECC approval exploration oil EnCore acquisition August 2015 | P11

Catcher – FPSO 1H Highlights • Turret and mooring system progressing – Mating cone module fabricated and delivered • Hull fabrication on-going in Japan and Korea • Topsides fabrication underway in ProFab, Dynamac and Asia Offshore yards August 2015 | P12

Catcher – subsea • 2 templates installed (Catcher 1 & Burgman 1) • PLEM installed • 60 km gas export pipeline lay completed • Fabrication of remaining templates completed • Fabrication of towheads well-advanced • First steel cut on mid- water arches • Fabrication of bundles to start in H2 • Fabrication of risers and jumpers to commence in 2016 August 2015 | P13

Catcher – drilling 1H Highlights • Ensco 100 rig on hire since July • Pilot hole completed 22 wells (14P, 8WI) • Batch drilling of 30” & 20” Six 4-slot templates sections of first 4 wells completed 2 phases of drilling • Operations on schedule and on each field within budget CTI1 – Drilling ahead at CTI1 CCP3 CTP1 CCI2 Template 1 September 2014 | P14 August 2015 | P14

Catcher – CTI1 progress Catcher Discovery wells CTI1 Tay reservoir Cromarty reservoir 1.5km to nearest offset well Reservoir encountered on depth • Operations on schedule and budget • Reservoir on prognosis; ‘ injectite wing’ and main reservoir found within 7 feet of pre- drill forecast • Setting production casing and will drill ahead reservoir section seeking ~250 feet net pay in ~600 feet gross interval August 2015 | P15

Sea Lion Neil Hawkings SE Asia & Falkland Islands Director

De-risking the Sea Lion development • Phase 1a reservoir is fully appraised, subsurface plan is robust • FPSO and SURF is well understood, conceptual design is now mature • Key project execution contractors are to be selected ahead of FEED • Financing plans progressing well • Upside in the area has increased and become better defined • Stakeholder discussions continuing August 2015 | P17

Exploration Robin Allan – N. Sea and Expl’n Director Dean Griffin – Head of Exploration

Exploration – re-shaping the portfolio • Focusing on under-explored, emerging 2012 2015 plays in proven hydrocarbon provinces – Entry into Brazil and follow-on farm in to Block 661, Ceará Basin Rationalisation 51 17 in – Successful entry into Mexico North Sea and SE Asia mature areas with award of Blocks 2 & 7 • Minimising up-front capex commitments Growth in • Current industry conditions favour low emerging basins 0 11 Falklands, Brazil and Mexico cost acreage acquisition with material opportunities • Exiting acreage in traditional, more mature areas (save for near-field exploration) Balance of wells targeting Mature verses Emerging plays – Significant disposal proceeds and reduced well commitments 2012 well campaign – Improved materiality of 2015 well discoveries campaign • Net unrisked prospective resource of >1 bn boe 100% 100% Mature Emerging August 2015 | P19

2015 North Falklands Basin campaign Aim • Demonstrate exploitation potential of F2 Two • Explore upside potential of F3 PL032 discoveries prospects from two 2015 1H highlights wells • Zebedee oil & gas discovery (36% op interest) Chatham Pmean – adds c. 50 mmbbls to Phase 2 47 mmbbls Jayne • Isobel Deep oil discovery (36% op interest) East Pmean – de-risks the Isobel/Elaine fan complex (un- 39 mmbbls Zebedee risked Pmean resource of 400 mmbbls) 50 – opens up potential Phase 3 development mmbls 2015 2H look ahead Phase 2 prospects • Jayne East (36% op interest) – would add resource to Phase 2 • Chatham (40% op interest) – would add resource to Phase 1b Southern exploration leads Isobel / Elaine Beyond 2015 Pmean 400 mmbbls • Additional exploration/appraisal prospects identified for drilling in 2017/2018 August 2015 | P20

Jayne East and Isobel Deep • Jayne East targets northern end of F3 fan sequence and Full stack amplitude at F3G horizon shallower F2 horizons • Further drilling at Isobel / Elaine complex to confirm significant resource potential of southern F3 fan system (unrisked Pmean 400 mmbbls) Jayne East Zebedee Jayne East North Falkland Isobel Deep Graben Isobel / Elaine Isobel Deep Re-drill Isobel / Elaine 10Km August 2015 | P21

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries

![Draft IRIS Assessment of Benzo[a]pyrene Presentation for the Benzo[a]pyrene Augmented Chemical](https://c.sambuz.com/196768/draft-iris-assessment-of-s.webp)