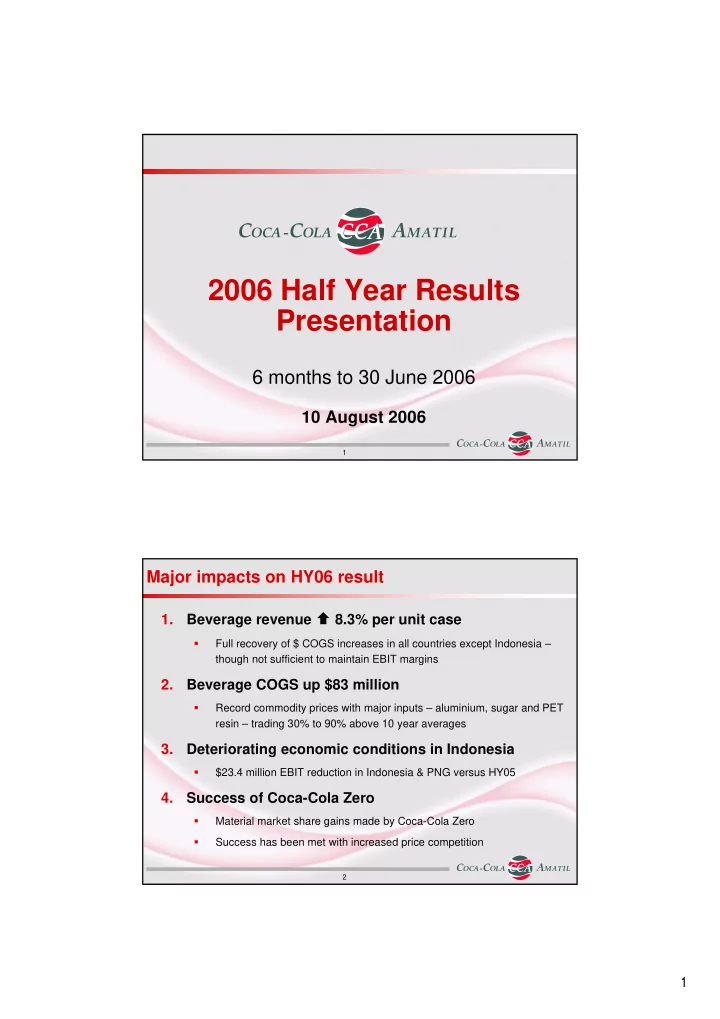

2006 Half Year Results Presentation 6 months to 30 June 2006 10 August 2006 1 Major impacts on HY06 result Beverage revenue � 8.3% per unit case 1. � Full recovery of $ COGS increases in all countries except Indonesia – though not sufficient to maintain EBIT margins 2. Beverage COGS up $83 million � Record commodity prices with major inputs – aluminium, sugar and PET resin – trading 30% to 90% above 10 year averages 3. Deteriorating economic conditions in Indonesia � $23.4 million EBIT reduction in Indonesia & PNG versus HY05 4. Success of Coca-Cola Zero � Material market share gains made by Coca-Cola Zero � Success has been met with increased price competition 2 1

Result Summary � 6.3% to $1.9bn Beverages revenue � 39.3% to $197.7m Food revenue 1 � 6.1% to $251.2m EBIT 1 � 0.1% to $145.4m NPAT 1 Earnings per share � 2.0% to 19.4c Dividends per share � 3.6% to 14.5c ROCE � 1.5 pts to 16.0% � $ 29.9m to $94.6m Free cash flow 3 1 . before significant items Australia HY06 HY05 % Chg A$m 1,105.8 1,039.3 6.4% Trading revenue Revenue per unit case $6.91 $6.71 3.0% Volume (million unit cases) 160.1 154.9 3.4% EBIT 218.2 217.8 0.2% EBIT margin 19.7% 21.0% (1.3 pts) Capital expenditure / revenue 3.3% 4.4% (1.1 pts) 4 2

Coca-Cola Zero KEY FACTS: � Outstanding consumer acceptance � Coca-Cola Zero has already taken 13% share of the Australian cola category � We have grown our total cola market share from 74% to 78% in the supermarket channel � Volume growth of 9% for Coca-Cola, diet Coke and Coca-Cola Zero in HY06 � Coca-Cola Zero already at > 60% of diet Coke volumes 5 Powerade Isotonic � New formulation Powerade Isotonic launched in May06 – more effective at hydrating and delivering energy to the body � Key opportunity for the sports drink category is to increase per capita consumption which is <30% of US and Japanese per caps � Powerade grew volumes >25% in HY06 Per Capita Sports Drink Consumption Per 8oz Serve 57 51 29 16 Japan USA Taiwan Australia 6 3

Australia – Current Trading & Full Year 2006 Outlook � Mount Franklin and Pump continue to grow volumes around 15% � Market share gains made by Coke met with strong price competition � Brand Coke average retail price gap to major competitor has widened from 33% to 36% over the last 3 months � Revenue per case increases of approx 7% since May � Outlook: � Solid rebound in July volume and price after slower May and June � Key issue for H2 will be competitive response and impact of higher prices on volumes 7 New Zealand & Fiji HY06 HY05 % Chg A$m 201.2 219.8 (8.5%) Trading revenue Revenue per unit case $6.39 $6.66 (4.1%) Volume (million unit cases) 31.5 33.0 (4.5%) EBIT 30.7 37.5 (18.1%) EBIT margin 15.3% 17.1% (1.8 pts) Capital expenditure / revenue 11.3% 4.4% 6.9 pts 8 4

New Zealand – Review & Full Year 2006 Outlook � NARTD category declined in HY06 in response to weakening consumer spending � Highlight for the first six months was the successful launch of Coca-Cola Zero with full year forecast volumes achieved by early June � Market characterised by higher levels of price competition � Outlook – Expecting a continuation of the trading conditions we experienced in HY06 9 South Korea HY06 HY05 % Chg A$m 366.7 310.5 18.1% Trading revenue Revenue per unit case $5.92 $4.93 20.1% Volume (million unit cases) 61.9 63.0 (1.7%) EBIT 1 8.5 0.9 844.4% EBIT margin 1 2.3% 0.3% 2.0 pts Capital expenditure / revenue 1.7% 5.4% (3.7 pts) 1. before significant items 10 5

South Korea – Review & Full Year 2006 Outlook � Delivered significant improvements in EBIT with local currency revenue per case up 10% � Continued expansion of the product portfolio with the launch of Coca-Cola Zero, Haru green tea and Minute Maid flavour extensions � Stabilisation of trademark Coca-Cola volumes in an NARTD market that declined by 7% � Outlook: � Great progress in HY06 with the business well on track to materially increase profits for the full year � Product recall in July after an extortion threat means H2 2005 outlook less certain 11 Indonesia & PNG HY06 HY05 % Chg A$m 184.4 178.1 3.5% Trading revenue Revenue per unit case $4.15 $3.39 22.4% Volume (million unit cases) 44.4 52.5 (15.4%) (12.1) 11.3 n/a EBIT EBIT margin (6.6%) 6.3% n/a Capital expenditure / revenue 11.2% 9.6% 1.6 pts 12 6

Indonesia – Economic landscape IDR per Litre Fuel Prices Inflation 4500 20% 16% 3500 Fuel prices have increased by Inflation 12% > 160% since climbed as high 2500 Jan05… as 18%... 8% 1500 4% Jan05 Apr05 Jul05 Oct05 Jan06 Apr06 Jan-05 Apr-05 Jul-05 Oct-05 Jan-06 Apr-06 Jul-06 Retail Sales Index Interest Rates 14% 180 Retail sales 170 declined by 18% 12% 160 And interest 10% 150 rates have increased to 140 8% 12.5%... 130 6% 120 Jan-05 Apr-05 Jul-05 Oct-05 Jan-06 Apr-06 Jan-05 Apr-05 Jul-05 Oct-05 Jan-06 Apr-06 13 Indonesia – Review & Full Year 2006 Outlook � CCA volume declines in line with overall retail sales decline � EBIT impacted by significant increases in cost base driven by: � Higher COGS � 2005 investment in sales force and coolers � Higher fuel costs � Flow on effect of high inflation � Outlook – expect Indonesia to return to profitability in the second half as high inflation and interest rates begin to moderate 14 7

6 months 4 months HY06 HY05 A$m % Chg Trading revenue 197.7 141.9 n/a EBIT 20.2 17.2 n/a EBIT margin 10.2% 12.1% n/a Capital expenditure / revenue 6.4% 2.8% 3.6 pts 15 SPCA – Review & Full Year 2006 Outlook � Fruit snacks category benefited from new convenience packaging of Goulburn Valley Fruit Snacks into the convenience and petroleum channel � International business driven by good volume and earnings growth Spain and Thailand manufacturing operations � Cheap imported product in Australia putting pressure on domestic volumes and margins � Good progress in improving the manufacturing and distribution efficiencies � Outlook – positive momentum in the business to continue for H2 16 8

2006 Half Year Results Presentation John Wartig, CFO 10 August 2006 17 Profit & loss A$m HY06 FY05 % chg EBIT (before significant items) 251.2 267.4 (6.1%) Net interest expense (66.2) (62.3) 6.3% Profit before tax 185.0 205.1 (9.8%) Income tax expense (39.6) (59.9) (33.9%) NPAT (before significant items) 145.4 145.2 0.1% Significant items after tax (31.1) - n/a NPAT 114.3 145.2 (21.3%) 18 9

Profit & loss Effective tax rate of 21.4% � Profits made in South Korea are not tax effected due to brought forward losses � Withholding tax benefit of $7 million due to losses in Indonesia and Korea on a post significant items basis � No tax payable on the $13.4 million gain on sale of the property at Eastern Creek due to Australian business utilising capital losses � Reversal of over provisions from prior years of $5 million Significant Items of $31.1m in South Korea � $27.9 million ERP with ~18 month payback � $3.2 million VAT audit penalty � Significant items are pre and post tax 19 Capital employed A$m HY06 FY05 $ chg Working capital 781.8 728.6 53.2 Property, plant & equipment 1,477.0 1,512.5 (35.5) IBAs & intangible assets 1,999.6 1,998.4 1.2 Deferred income tax liability (344.8) (341.9) (2.9) Other net assets / (liabilities) (328.3) (340.1) 11.8 Capital Employed 3,585.3 3,557.5 27.8 20 10

Working capital � Beverage working capital to Working capital revenue – small increase primarily due to impact of Group working capital currency translation on $782m $738m $729m South Korea and Indonesian balances partially offset by improvements in Australia � Food working capital to revenue – further reductions HY05 FY05 HY06 expected from introduction Beverages Food Other of automated inventory Working capital / revenue control system HY05 FY05 HY06 Beverages 11.1% 12.2% 11.4% Food 82.4% 67.0% 78.4% 21 Balance sheet remains strong � Net debt increase by Net Debt & Interest Cover $25.9 million $2,500m 5.0x � Cash balances increased by $279 million due to $2,000m 4.0x pre-funding of debt maturities in Q3 $1,500m 3.0x � Interest cover strong at $1,000m 2.0x 3.8x within CCA’s target range of 3.0 – 4.0x $500m 1.0x $0m 0.0x 2001 2002 2003 2004 2005 HY06 Net Debt Interest Cover 22 11

ROCE � Group ROCE down 1.5 pts ROCE due to reduction in earnings from Indonesia and full six 21.6% months impact of SPCA Post IFRS � Short-term ROCE dilution 17.5% Pre IFRS 16.0% expected from lead times in generating returns from infrastructure capex 10.2% 8.8% 7.3% 2001 2002 2003 2004 2005 HY06 23 Capital expenditure � 4.7% capex / revenue broadly in Capital Expenditure line with last year � $120m Full year capex expected to be around 7% of revenue including 4.8% $100m 5.0% 2% for infrastructure 5.0% � $80m H2 2006 increases in capex to be driven by infrastructure $60m spending on Sydney and Auckland automated $40m warehouses $20m $0m HY04 HY05 HY06 PPE Other (vehicles, computers etc) Cold drink equipment 24 12

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries