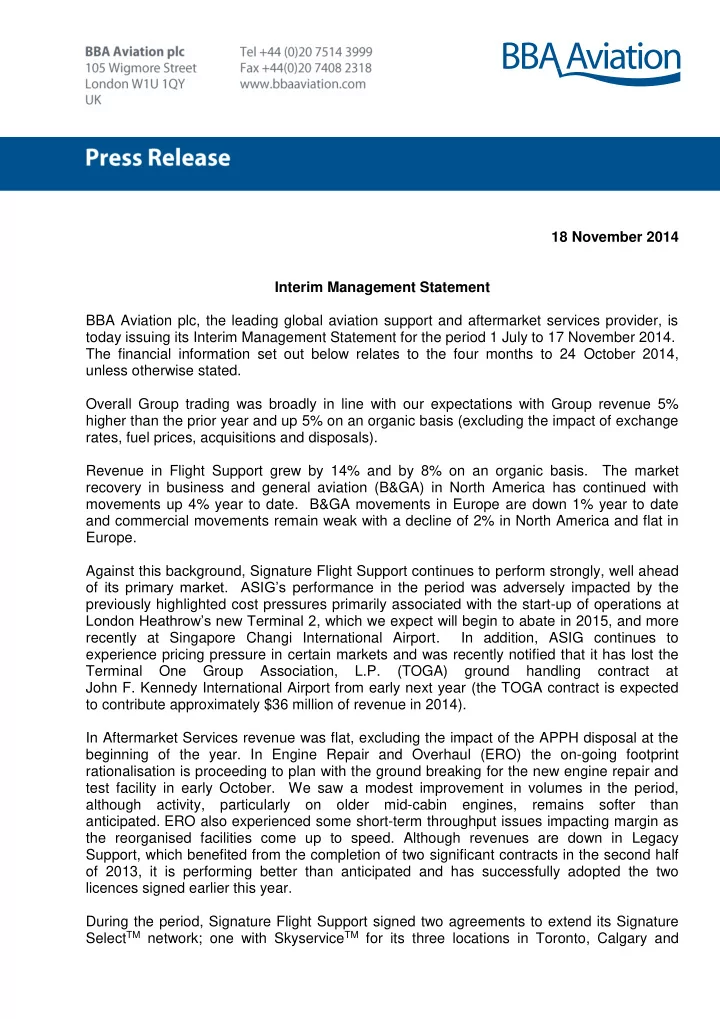

18 November 2014 Interim Management Statement BBA Aviation plc, the leading global aviation support and aftermarket services provider, is today issuing its Interim Management Statement for the period 1 July to 17 November 2014. The financial information set out below relates to the four months to 24 October 2014, unless otherwise stated. Overall Group trading was broadly in line with our expectations with Group revenue 5% higher than the prior year and up 5% on an organic basis (excluding the impact of exchange rates, fuel prices, acquisitions and disposals). Revenue in Flight Support grew by 14% and by 8% on an organic basis. The market recovery in business and general aviation (B&GA) in North America has continued with movements up 4% year to date. B&GA movements in Europe are down 1% year to date and commercial movements remain weak with a decline of 2% in North America and flat in Europe. Against this background, Signature Flight Support continues to perform strongly, well ahead of its primary market. ASIG’s performance in the period was adversely impacted by the previously highlighted cost pressures primarily associated with the start-up of operations at London Heathrow’s new Terminal 2 , which we expect will begin to abate in 2015, and more recently at Singapore Changi International Airport. In addition, ASIG continues to experience pricing pressure in certain markets and was recently notified that it has lost the Terminal One Group Association, L.P. (TOGA) ground handling contract at John F. Kennedy International Airport from early next year (the TOGA contract is expected to contribute approximately $36 million of revenue in 2014). In Aftermarket Services revenue was flat, excluding the impact of the APPH disposal at the beginning of the year. In Engine Repair and Overhaul (ERO) the on-going footprint rationalisation is proceeding to plan with the ground breaking for the new engine repair and test facility in early October. We saw a modest improvement in volumes in the period, although activity, particularly on older mid-cabin engines, remains softer than anticipated. ERO also experienced some short-term throughput issues impacting margin as the reorganised facilities come up to speed. Although revenues are down in Legacy Support, which benefited from the completion of two significant contracts in the second half of 2013, it is performing better than anticipated and has successfully adopted the two licences signed earlier this year. During the period, Signature Flight Support signed two agreements to extend its Signature Select TM network; one with Skyservice TM for its three locations in Toronto, Calgary and

Montreal, and one with Menzies Aviation in Barcelona, marking Signature’s first Signature Select TM in Europe and Signature’s first foothold in Spain . This extension of the Signature network is in addition to the previously announced acquisition of Wiggins Airways FBO at Manchester-Boston Regional Airport in October. In September, Legacy Support signed two new licences with Curtiss-Wright for electro-mechanical, hydraulic and pneumatic valves and actuators. Legacy Support has now signed 8 new licences over the last 12 months. Total capital expenditure for the year is expected to be around 2x depreciation and amortisation, including Signature’s large development projects at London Luton, which is due to become operational in early 2017, and at San Jose, which is due to be completed by the end of 2015. Trading cash flows have followed the usual seasonal pattern and the Group’s balance sheet remains strong. The $125 million share re-purchase programme is ongoing and to date approximately $63.5 million of shares have been repurchased. ERO’s Dallas Airmotive business is cooperating with the U.S. Department of Justice (DOJ) in an investigation relating to payments in South America by agents and employees of the business from 2008-2012. Dallas Airmotive is engaged in settlement discussions with the DOJ. The Company expects to take an exceptional charge of approximately $15 million in the fourth quarter of 2014 related to this matter. During the period, the Group also agreed a settlement with the IRS in relation to the 2006 to 2010 tax years resulting in a cash inflow and exceptional gain of $20.6 million. Commenting on the Interim Management Statement, Simon Pryce, BBA Aviation Group Chief Executive said: “BBA Aviation’s Flight Support division is now realising the benefits of the significant investments made in Signature in recent years as B&GA movements in North America continue to recover, although this has been partly offset by ASIG ’s growth costs which will abate in 2015. The recovery in B&GA movements is taking longer than anticipated to have a meaningful impact on engine repair and overhaul volumes in our Aftermarket Services division, which is also experiencing some short-term throughput inefficiency associated with the footprint rationalisation programme. This is being partly offset by a stronger than expected performance in Legacy. Ethical and legal compliance are core values of this Group and any breach of our high standards of conduct are taken extremely seriously. We continually look for ways to strengthen our compliance and control programmes to ensure we uphold these standards, which are fundamental to the way we operate. Despite the softness of ERO’s market and performance, we expect 2014 to be another year of absolute progress. Having already committed significant growth investment this year and with a good further pipeline for opportunities, we have good momentum going in to 2015.” Notes: BBA Aviation will announce its final results for the year ending 31 December 2014 on 4 March 2015.

Enquiries: BBA Aviation plc Mike Powell, Group Finance Director / Jemma Spalton, Head of Investor Relations 020 7514 3999 Tulchan David Allchurch / Christian Cowley 020 7353 4200 Notes to Editors BBA Aviation plc is a leading global aviation support and aftermarket services provider with market leading businesses and attractive growth opportunities. BBA Aviation’s Flight Support businesses (Signature Flight Support and ASIG) are focused on refueling and ground handling of business and commercial aviation aircraft. Its Aftermarket Services businesses (Dallas Airmotive, H+S Aviation, International Turbine Service, Barrett Turbine Engine Company, Ontic and APPH) are focused on the repair and overhaul of jet engines and the manufacture and service of aerospace sub-systems and components. For more information, please visit www.bbaaviation.com. This interim management statement contains forward-looking statements which are based on current expectations and assumptions. Such statements are subject to a number of risks and uncertainties that could cause actual results to differ materially from any expected future events or results referred to in these forward-looking statements. Unless otherwise required by applicable law, regulation or accounting standard, we do not undertake any obligation to update or revise any forward-looking statement, whether as a result of new information, future developments or otherwise.

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries