1031 Exchanges & Qualified Opportunity Zones Drew Emmert Colleen R. Fausz Ryan M. Whitaker

Part 1: 1031 Exchanges

Roadmap • Overview of 1031 Exchanges • History of 1031 Exchanges • Benefits of 1031 Exchanges • 1031 Exchange Requirements • Types of Exchanges • Common Issues • Changes to 1031 Exchanges from Tax Cuts and Jobs Act of 2017

Overview of 1031 Exchanges An exception to the recognition of taxable gain on sale of real property, provided the seller reinvests in like kind property Any entity or individual that is subject to tax may exchange assets they own This taxable gain is: (a) deferred until the property exchanged into is later sold in a taxable transaction or (b) eliminated if the property exchanged, or a subsequent replacement property, owned until death. The assets pass to the heirs at the then fair market value on the date of death. The deferred gain is eliminated. Can be partial 1031 exchange if unable to fully reinvest within the exchange period

History of 1031 Exchanges 1918 – Income tax first imposed – general rule that all gain is taxable 1921 – Old Section 202(c) (predecessor to 1031) Simultaneous exchanges only Policy – (a) continuity of investment, and (b) administrative convenience “[I]f the taxpayer's money is still tied up in the same kind of property as that in which it was originally invested, he is not allowed to compute and deduct his theoretical loss on the exchange, nor is he charged with the tax upon his theoretical profit. The calculation of the profit or loss is deferred until it is realized in cash, marketable securities, or other property not of the same kind having a fair market value.” HR Rep No. 704, 73d Cong, 2d Session (1934). 1984 – “Deferred” exchanges allowed, time limits imposed 2017 – Tax Cuts and Jobs Act of 2017 – no more personal property exchanges

Benefits of 1031 Exchanges 1031 Exchanges allow taxpayers to: Not pay income taxes in the current year on the exchange Allows tax-deferred diversification – either in terms of geographic scope, or type of property (e.g. residential to commercial, etc.) Increase cash flow available to the taxpayer to reinvest in their business Reinvest in more productive property and to earn more revenue from the property

1031 Exchange Requirements “Exchange” Requirement – sale of one property followed by purchase of another “Real Property” Requirement Fee Interest Leasehold Interest (30 years or more remaining) Tenancy in Common Interest “Like-Kind” requirement Very broad – almost all Real Property is “like-kind” to other real property; this rule was primarily aimed at Personal Property exchanges which have been eliminated by the Tax Cuts and Jobs Act of 2017 Old Property exchanged for Newer Property Commercial Property exchanged for Residential Property Improved Real Estate for Unimproved Real Estate

1031 Exchange Requirements continued… Qualified Use Requirement Both Relinquished Property and Replacement property have to be either (a) held for investment; or (b) used in taxpayer’s trade or business NOT Personal Residence NOT Dealer Property/Inventory Same Taxpayer Requirement Individual sells Relinquished Property, same individual purchases Replacement Property (matching of social security numbers) Entity sells, entity purchases (matching of EINs) Special Rules for Disregarded Entities, “Grantor (Revocable) Trusts” Timing Identify Replacement Property within 45 days Purchase Replacement Property within 180 days

1031 Exchange Requirements continued… No constructive receipt of funds from sale Deposit funds with a “Qualified Intermediary” No cash out Proceeds held in Escrow Must purchase Replacement Property with equal or greater value Must roll 100 percent of equity into Replacement Property If either of the above cannot happen, taxpayer receives “taxable boot” – BUT can have partial-1031 exchanges. Documentation and Reporting Exchange Agreement and Escrow Agreement Addendum, Assignments, etc.

Mechanics of Standard “Forward” Exchange Prior to sale of Relinquished Property Taxpayer engages Qualified Intermediary and executes Escrow Agreement and Exchange Agreement, among other legal documents; and Taxpayer assigns Purchase and Sale Agreement to QI so that QI can receive funds from sale of Relinquished Property. Taxpayer sells Relinquished Property and funds are deposited in a segregated “Qualified Escrow Account” Within 45 days from sale, Taxpayer “identifies” (in writing) Replacement Property Within 180 days of sale, Taxpayer purchases Replacement Property After the exchange – QI or accountant reports 1031 exchange on IRS Form 8824

Types of Exchanges Simultaneous Exchanges Two parties swap their properties No longer common; more convenient for taxpayers to utilize “deferred exchanges” Deferred Exchanges Forward Exchanges – Taxpayer sells, then purchases within 180 days Reverse Exchanges – Taxpayer purchases Replacement Property First, Sells Relinquished Property within 180 days “Parking” Exchanges outside Regulatory Safe Harbor – risky, but if structured properly, could allow taxpayer to effectuate 1031 exchange outside 180 day time period

Types of Exchanges continued… Improvement/Construction Exchanges When the value of Replacement Property is less than vale of Relinquished Property, Taxpayer will generally owe tax on the difference (i.e. a “cash out”) “Improvement Exchange” solves this problem – Example: January 1 - Taxpayer sells Relinquished Property for $1MM February 1– Taxpayer purchases Replacement Property for $600,000 February 1 through June 30 – Taxpayer makes improvements to Replacement Property valued at $400,000 Value of Replacement Property after improvements is $1MM, which is equal to value of Relinquished Property – no tax owed! (assuming other 1031 requirements satisfied).

Common Issues Personal Property included in purchase price – separately allocate in Purchase Agreement and on Closing Statement Found replacement property before finding purchase of relinquished property – Reverse Exchange Issues with documentation and reporting – consult with Tax Attorney or CPA who is experienced in 1031 exchanges The value of my replacement property is not sufficient to fully defer gain – do “Improvement Exchange” “One of my partners does not wish to effectuate a 1031 exchange” – do equity restructuring in advance of exchange, or cash the partner out at closing with corresponding gain allocation

Changes to 1031 Exchanges from Tax Cuts and Jobs Act of 2017 No more personal property exchanges – only real property 100 percent expensing on certain Qualified Improvements – may mean less 1031 exchanges Alternative to 1031 Exchanges – Qualified Opportunity Zones Only required to rollover “gain” into QOZ, whereas 1031 required to (a) roll over equity position, and (b) purchase property with a value equal to or greater than Relinquished Property.

Part 2: Understanding Qualified Opportunity Zones

What is a Qualified Opportunity Zone? Provides significant tax incentives for taxpayers to reinvest unrecognized capital gains in certain property and businesses located or operating in QOZs. Enacted as part of the Tax Cuts and Jobs Act of 2017. Encourages economic development in low-income areas by providing various tax incentives for private investments in QOZs.

Where are the Opportunity Zones? Treasury has designated QOZs in all 50 states, the District of Columbia, and five U.S. possessions - Map is FINAL KY - 144 low-income census tracts in 84 counties 7 designated in Kenton (5), Campbell (1), and Boone (1) counties. Hamilton Co., OH – 30 QOZs, including CBD, OTR, Avondale, Queensgate and Camp Washington.

Qualified Opportunity Zones in Ohio https://development.ohio.gov/bs/bs_censustracts.htm

Qualified Opportunity Zones in Hamilton County https://development.ohio.gov/bs/bs_censustracts.htm

Qualified Opportunity Zones in Kentucky Source: http:/ /www.thinkkentucky.com/OZ/

Qualified Opportunity Zones in N. Kentucky Source: https://www.cims.cdfifund.gov/preparation/?config=config_nmtc.xml

Qualified Opportunity Zones in N. Kentucky Source: https://www.cims.cdfifund.gov/pre paration/?config=config_ n mtc.xm1

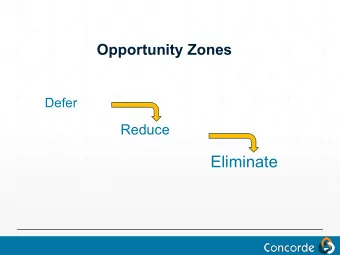

QOZ Tax Incentives 1. Temporary deferral of capital gain. 2. Step-up in basis. 3. Permanent exclusion of gain on appreciation.

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries